It’s possible to have many IRAs, but the most money you can put into all of them at once is limited.

Many, or all, of the products featured on this page are from our advertising partners who compensate us when you take certain actions on our website or click to take an action on their website. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not provide advisory or brokerage services, and it does not tell investors whether to buy or sell certain stocks, bonds, or other investments.

The answer to how many IRAs you can have is straightforward: Theres no limit. But whats more important to understand is that annual contribution limits still apply across all your IRA accounts combined. That limit for IRA contributions into any IRA you have is $7,000 in 2025 ($8,000 if age 50 and older).

There are exceptions: contribution limits don’t apply to rollovers from employer-sponsored retirement plans, such as a 401(k) into an IRA, or rollovers from one IRA account to another.

Its also worth noting that if youre hoping to invest in a Roth IRA, your income may make you ineligible to contribute the maximum amount. (You can learn more about Roth IRA income limits here. ).

Yes, You Can Have Multiple Roth IRAs – Here’s What You Need to Know

Having more than one Roth IRA is completely legal and sometimes even beneficial for your retirement strategy. I’ve seen many clients confused about this topic, so let’s clear things up right away yes, you absolutely can have two or more Roth IRAs at the same time. There’s no limit on the number of IRA accounts you can open.

But—and this is a big but—having more than one account doesn’t make it possible for you to contribute more. The IRS limits are for the total amount of money you can put into all of your IRAs, not just one.

Let me walk you through everything you need to know about having multiple Roth IRAs including the benefits limitations, and strategies for making the most of your retirement savings.

The Real Rules About Multiple Roth IRAs

The misconception that you can only have one IRA account is super common. Truth is you can have as many Roth IRAs as you want. You can even have multiple traditional IRAs alongside your Roth IRAs.

Here’s what matters:

- No limit on number of accounts: You can open IRAs at different financial institutions

- Combined contribution limit: For 2025, the total amount you can contribute across all your traditional and Roth IRAs combined is $7,000 if you’re under 50, or $8,000 if you’re 50 or older

- Same eligibility requirements: Having multiple accounts doesn’t change income limits or eligibility rules

If you’re 45 years old and have two Roth IRAs, you could put $3,500 into each one, or any other amount that adds up to $7,000 for the year. Just can’t go over that total limit.

Why You Might Want Multiple Roth IRAs

There are actually several good reasons why someone might open more than one Roth IRA:

1. Investment Diversification

Having accounts at different financial institutions gives you access to different investment options. Maybe one brokerage has great mutual funds while another offers excellent ETF choices or robo-advisor services.

One of my clients told me, “I keep one Roth at Fidelity for their sector funds and another at a different firm for their international options that weren’t available at Fidelity.” “.

2. Insurance Coverage Protection

Each financial institution provides SIPC insurance coverage (up to $500,000, including $250,000 for cash). Having accounts at different places can increase your total coverage.

3. Testing Different Providers

You might want to try out different brokerages to compare their:

- Customer service

- Investment options

- User interfaces

- Fee structures

4. Organizational Purposes

Some people find it helpful to have separate IRAs for different goals or investment strategies. One account might be more aggressive growth-oriented while another focuses on income-generating investments.

5. Estate Planning

Having separate IRAs with different beneficiaries can simplify estate planning. You don’t have to split up a single account to give each one to a different heir.

The Contribution Limits You Need to Know

This is where things get strict. The IRS sets contribution limits that apply across all your IRA accounts combined:

For 2025:

- $7,000 maximum contribution if you’re under 50

- $8,000 maximum contribution if you’re 50 or older (includes $1,000 catch-up contribution)

These limits apply to the total of all your traditional and Roth IRA contributions in a single tax year. So if you contribute $3,000 to a traditional IRA, you’d only have $4,000 left that you could contribute to your Roth IRA(s) if you’re under 50.

Remember that Roth IRA contributions may be limited or eliminated based on your income. For 2025:

- Single filers: Full contributions allowed with MAGI under $150,000, phase-out between $150,001-$165,000

- Married filing jointly: Full contributions allowed with MAGI under $236,000, phase-out between $236,001-$246,000

Can You Have Both a Roth IRA and Traditional IRA?

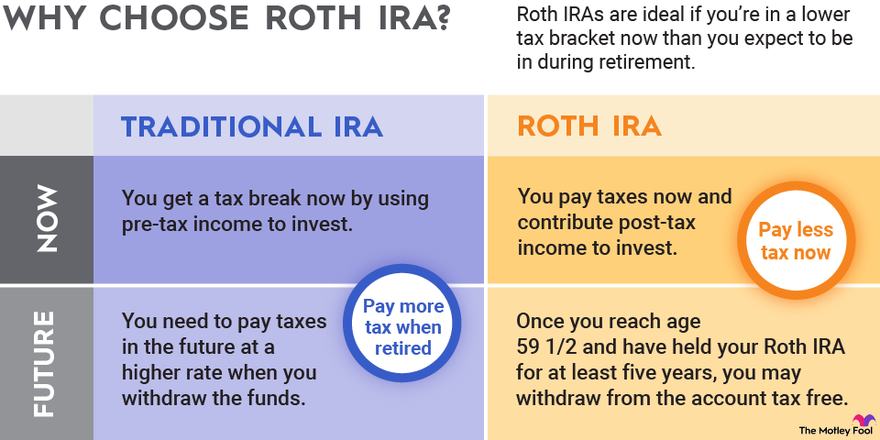

Absolutely! In fact, having both types can be a smart tax-diversification strategy. With a traditional IRA, you might get a tax deduction now but pay taxes when you withdraw in retirement. With a Roth, you pay taxes now but get tax-free withdrawals in retirement.

Just remember that the contribution limit applies to all your IRAs combined. If the limit is $7,000 and you put $4,000 in a traditional IRA, you can only put $3,000 in your Roth IRA(s).

Can You Contribute to an IRA and a 401(k)?

Yes, you can contribute to both an employer-sponsored retirement plan (like a 401(k)) and an IRA in the same year. However, if you or your spouse are covered by a workplace retirement plan and your income is above certain levels, your ability to deduct traditional IRA contributions may be limited.

For Roth IRAs, 401(k) participation doesn’t affect your eligibility – only your income matters.

Managing Multiple Roth IRAs: Tips and Strategies

If you do decide to have multiple Roth IRAs, here are some tips to manage them effectively:

1. Track Your Total Contributions

Use a spreadsheet or financial app to ensure you don’t exceed the annual limit across all accounts. The IRS won’t be happy if you over-contribute, and penalties can apply.

2. Consider Consolidation If Needed

If managing multiple accounts becomes too complex, you can always consolidate them later through a direct transfer, which won’t count as a contribution or trigger taxes.

3. Choose Complementary Investment Strategies

Rather than duplicating the same investments, use different accounts for different asset classes or strategies.

4. Keep Beneficiary Designations Updated

One of the biggest mistakes I see is people forgetting to update beneficiaries on all their accounts. Make sure to review these regularly, especially after major life events.

5. Watch Out for Fees

Multiple accounts might mean multiple maintenance fees. Compare the cost against the benefits you’re getting from having separate accounts.

The Drawbacks of Multiple Roth IRAs

While having multiple Roth IRAs is allowed and can be beneficial, there are some potential downsides:

1. More Paperwork and Complexity

Each account generates its own statements, tax forms, and communications. This can make your financial life more complicated.

2. Risk of Exceeding Contribution Limits

With money going into multiple accounts, it’s easier to accidentally contribute too much, which can result in penalties.

3. Harder to Track Performance

Evaluating your overall retirement portfolio performance becomes more challenging when investments are spread across multiple platforms.

4. Potential for Higher Fees

You might end up paying more in account maintenance fees with multiple accounts.

When Should You Consider Consolidating IRAs?

Sometimes having multiple IRAs doesn’t make sense anymore. Consider consolidating if:

- You’re finding it difficult to keep track of multiple accounts

- You’re paying unnecessary fees for account maintenance

- You want to simplify your financial life

- You’ve accumulated small balances across several accounts

- You want a clearer picture of your overall retirement strategy

FAQs About Multiple Roth IRAs

Can I transfer money between my two Roth IRAs?

Yes, you can transfer funds between Roth IRAs without tax consequences through a direct trustee-to-trustee transfer. This doesn’t count toward your annual contribution limit.

Can I convert my traditional IRA to multiple Roth IRAs?

Yes, you can split a conversion among multiple Roth IRAs. Some people do this for tax planning or investment diversification reasons.

If I have a 401(k) and a Roth IRA, how much can I contribute to each?

These plans have separate contribution limits. For 2025, you can contribute up to $7,000 (or $8,000 if 50+) to your Roth IRA and up to $23,000 (or $30,500 if 50+) to your 401(k).

What happens if I accidentally contribute too much across my multiple IRAs?

You’ll need to withdraw the excess contributions (and any earnings on them) before your tax filing deadline (including extensions) to avoid a 6% excise tax penalty that applies each year the excess remains in your account.

Can my spouse and I have Roth IRAs at the same financial institution?

Yes, but they would be separate individual accounts since IRAs (Individual Retirement Accounts) are always individually owned.

Making the Right Choice for Your Retirement

Having multiple Roth IRAs is perfectly legal and might make sense for your situation. The key is understanding that the total contribution limits apply across all your IRA accounts combined and being strategic about how you use them.

For most people, the decision comes down to convenience versus specific benefits. If having accounts at different institutions gives you access to unique investment opportunities or services that help you reach your retirement goals, it could be worth the extra paperwork.

In my experience working with retirement savers, I’ve found that what matters most isn’t how many accounts you have, but rather:

- That you’re contributing regularly

- You’re investing appropriately for your time horizon

- You’re staying within contribution limits

- Your overall asset allocation makes sense

Whether you choose one Roth IRA or several, the most important thing is that you’re taking steps to secure your financial future. The fact that you’re researching this question suggests you’re already on the right track!

Remember, while having multiple Roth IRAs might seem complicated, the fundamental goal remains simple: building wealth for a comfortable retirement. Focus on maximizing your contributions (within limits), making smart investment choices, and regularly reviewing your retirement strategy as your life circumstances change.

More paperwork

Although it’s easier than ever to track and manage your money online, multiple accounts mean dealing with multiple tax forms, notices of service changes or updates, privacy policies and other disclosures.

5 benefits of multiple IRAs

Having multiple IRAs can help you fine-tune your tax-minimization strategy, as well as access more investment choices and increased account insurance. Here are the pros of having multiple IRAs: