The world of trusts is not one-size-fits-all. What kind of trust you pick should depend on how you want your assets to be managed now and in the future.

Terry Ruhe, senior vice president and regional trust manager for U.S. Trust, says, “A trust can help you deal with specific tax issues or protect you from creditors. It can also help you make sure your wealth supports your family or leave a legacy for a charity you believe in.” S. Bank Wealth Management. “Whatever your wishes, there’s a trust for you. ”.

The two basic trust structures are revocable and irrevocable. The biggest difference is that revocable trusts can be changed after they are created, while irrevocable trusts typically cannot.

As stated above, a revocable trust – also referred to as a living trust – is one that can be changed after it’s created. “A revocable trust can accomplish many of the same things as a will. However, there’s one key difference,” says Ruhe. “You can avoid the probate process that’s needed for a will by setting up a revocable trust and moving your assets to it.” ” Probate can be both lengthy and public, and a revocable trust usually is not public.

Because you can make changes to your revocable trust at any time, for certain purposes you are still viewed as the owner of the assets – even though you have a trustee who manages the trust for you. For example, you’ll be responsible for making tax payments and reporting on the trust’s investment returns, and revocable trust assets are includable in your estate and are available to creditors.

You can set up your revocable trust to play out in several different ways, too. You can have your revocable trust end upon your death, and have all assets distributed to your beneficiaries at that time. You can also set it up so that when you pass away, that revocable trust automatically creates irrevocable trusts that continue for different people or institutions.

You typically cannot change or amend an irrevocable trust after it’s created. The assets move out of your estate, and the trust pays its own income tax and files a separate return. This can give you greater protection from creditors and estate taxes.

As stated above, you can set up your will or revocable trust to automatically create irrevocable trusts at the time of your death. When you use your will to create irrevocable trusts, it’s called a testamentary trust. But you can also set up irrevocable trusts during your lifetime.

There are a variety of irrevocable trust types to choose from, depending on your unique circumstances. “Your reason for setting up an irrevocable trust is critical in helping you select one that fits your needs,” says Ruhe. Are you setting up a trust to:

The following are scenarios where these concerns can be addressed through a type of irrevocable trust.

You worked hard for what you have, let’s face it. After you die, the last thing you want is for your hard-earned assets to be taken by creditors, lawsuits, or high taxes. There are trusts that can help with this, but not all of them are the same when it comes to protecting assets.

I have spent a lot of time researching the different kinds of trusts that can help protect your money. Now I’m going to explain it all to you in simple terms. There’s a trust that can help you if you’re worried about estate taxes, future debts, or just making sure your loved ones are taken care of.

Understanding Trusts: The Basics

Before diving into specific types let’s get clear on what a trust actually is. A trust is basically a legal arrangement where you (the grantor) transfer assets to a trustee who manages those assets for your beneficiaries. Think of it as a secure container for your stuff that follows your specific instructions.

Trusts are great because they are flexible; you can change them to fit your needs and goals. Whether you want to keep your assets safe from creditors, lower your taxes, or take care of your family, there’s probably a trust idea that will work for you.

Which Types of Trusts Actually Protect Your Assets?

Not all trusts provide asset protection. Here are the ones that do:

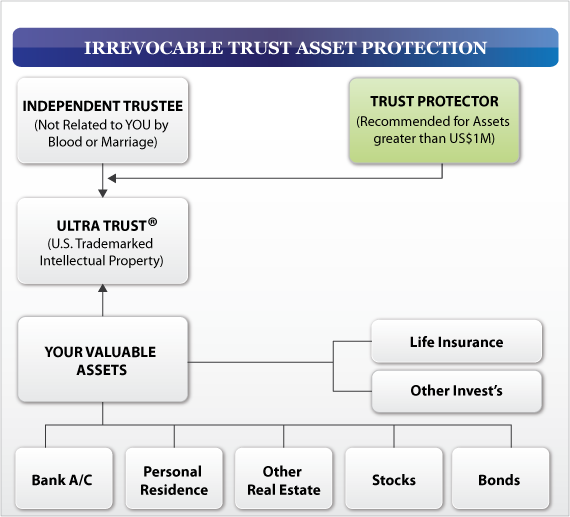

1. Irrevocable Trusts

When it comes to protecting your assets, an irrevocable trust is the best. Unlike its revocable cousin, once you put assets in an irrevocable trust, you give up ownership and control of them.

Key benefits

- Assets are removed from your taxable estate

- Protection from creditors and lawsuits

- Shields assets from nursing home and Medicaid costs

The catch? You can’t easily change or dissolve the trust once it’s established. This permanence is exactly what provides the protection – since the assets are no longer yours, creditors can’t touch them.

As one attorney told me, “Think of an irrevocable trust like giving someone a gift. Once you’ve handed it over, you can’t ask for it back just because you changed your mind.”

2. Asset Protection Trusts (APTs)

These specialized irrevocable trusts are specifically designed to shield your assets from creditors and legal claims. They come in two flavors:

Domestic Asset Protection Trusts (DAPTs)

- Available in only some states (like Nevada, Delaware, and South Dakota)

- Allows you to be a beneficiary while still protecting assets

- Less expensive than offshore options

Foreign Asset Protection Trusts

- Set up in jurisdictions with strong asset protection laws (Cook Islands, Nevis)

- Provides stronger protection than domestic trusts

- More complex and expensive to establish

APTs are particularly useful for individuals in high-risk professions like doctors, lawyers, and business owners who might face lawsuits. But remember – these must be set up before any legal claims arise, or they could be considered fraudulent transfers!

3. Spendthrift Trusts

If you’re worried about a beneficiary who’s not great with money (we all know someone!), a spendthrift trust might be perfect. This trust includes provisions that prevent beneficiaries from:

- Selling or transferring their interest in the trust

- Having trust assets seized by creditors

Imagine your nephew who can’t seem to hold onto money for more than a week. With a spendthrift trust, he’d receive structured payments instead of a lump sum, and his creditors couldn’t touch the principal.

4. Special Needs Trusts

These trusts are designed specifically for beneficiaries with disabilities who rely on government benefits like Medicaid or Supplemental Security Income (SSI).

How they protect assets:

- Assets in the trust don’t count toward eligibility limits for government benefits

- Provides supplemental support without disqualifying the beneficiary from crucial programs

- Ensures funds are used appropriately

For families with special needs members, this trust is absolutely essential to protect both the assets and the beneficiary’s access to necessary support services.

Comparison: Asset Protection Power of Different Trusts

Let me break it down with this handy comparison table:

| Type of Trust | Asset Protection Level | Control Retained | Tax Benefits | Complexity |

|---|---|---|---|---|

| Revocable Living Trust | Low | High | Minimal | Moderate |

| Irrevocable Trust | High | Low | Significant | High |

| Asset Protection Trust | Very High | Moderate | Significant | Very High |

| Spendthrift Trust | Moderate-High | Low | Moderate | Moderate |

| Special Needs Trust | High (for beneficiary) | Low | Moderate | High |

| QTIP Trust | Moderate | Low | Significant | High |

When Revocable Trusts DON’T Protect Your Assets

Here’s a common misconception I gotta clear up: revocable living trusts DO NOT protect your assets from creditors during your lifetime.

While they’re awesome for avoiding probate and maintaining privacy, the fact that you can change or dissolve them means the assets are still considered yours. This makes them vulnerable to creditors, lawsuits, and bankruptcy claims.

As one estate planning attorney put it to me, “A revocable trust is like putting your assets in a glass display case – everyone can still see them, and you can take them out whenever you want. That’s not protection.”

Creating a Trust That Actually Protects Your Assets

If asset protection is your primary goal, here are some key steps:

-

Start early – Most asset protection trusts must be established well before any legal claims arise (typically 2-4 years)

-

Work with a specialist – This isn’t DIY territory, folks. Asset protection planning requires specialized knowledge of both state and federal laws

-

Be honest about your goals – Hiding assets from existing creditors is fraud. Be upfront with your attorney about your situation

-

Consider your level of control – The more protection you want, the less control you’ll likely need to give up

-

Evaluate the costs – Some trusts are expensive to establish and maintain, so make sure the protection is worth the investment

Who Should Consider Asset Protection Trusts?

You might benefit from an asset protection trust if:

- You work in a profession with high liability risk (doctors, lawyers, etc.)

- You own a business or real estate investments

- You’re concerned about future long-term care costs

- You have significant wealth that could attract lawsuits

- You want to protect an inheritance for your children from divorce or other claims

Beyond Trusts: Other Asset Protection Strategies

While trusts are powerful tools, they’re not the only way to protect your assets. Consider these complementary strategies:

- Insurance – Liability insurance is your first line of defense

- Business entities – LLCs and corporations can shield personal assets from business liabilities

- Retirement accounts – Many have built-in creditor protection under federal law

- Homestead exemptions – Some states offer significant protection for your primary residence

Common Mistakes to Avoid

I’ve seen people make these mistakes way too often:

- Waiting until there’s a problem – Asset protection must be done proactively, not reactively

- Commingling personal and business assets – This can pierce the liability shield

- Creating a DIY trust – Asset protection is complex and requires professional guidance

- Not funding the trust – A trust without assets is just an empty shell

- Choosing the wrong trustee – This person has significant power, so choose wisely

The Bottom Line on Asset Protection Trusts

Let’s keep it real – if you want serious asset protection, you’ll need an irrevocable trust structure of some kind. The specific type depends on your unique situation, goals, and the level of control you’re willing to sacrifice.

Remember that asset protection planning isn’t about hiding assets or avoiding legitimate obligations. It’s about proactively structuring your affairs to protect against unforeseen future risks while ensuring your wealth can benefit those you care about most.

I always tell my clients: “The best time to set up asset protection was yesterday. The second-best time is today.” Don’t wait until you need protection to start planning – by then, it’s usually too late.

Have questions about which trust might be right for your situation? Reach out to a qualified estate planning attorney who specializes in asset protection. They can help create a customized plan that balances protection with your other financial and personal goals.

Trust me (pun totally intended), your future self will thank you for taking steps today to protect what you’ve worked so hard to build.

Grantor retained annuity trust (GRAT) and qualified personal residence trust (QPRT)

There are certain irrevocable trusts that are intended to last for only a specific term of years. Two examples are grantor retained annuity trusts (GRATs) and qualified personal residence trusts (QPRTs).

“GRATs are a common way for people to minimize taxes on financial gifts to their beneficiaries,” says Ruhe. With this type of trust, you contribute assets to the trust and receive an annuity payment on a regular basis, usually a set percentage of the original amount of assets. The assets in the trust will inevitably rise and fall in value.

When the trust ends, any money left over, including any growth in value, goes to your chosen recipients tax-free as a gift. These things will be part of your estate and subject to estate tax if you are not alive when the terms end.

QPRTs are another way to transfer assets to beneficiaries – more specifically, real estate. “Let’s say you want to give your home to your child but have no plans to move out,” Ruhe says. “You could set up a QPRT for 10 years. If you are still alive when the trust ends, the property goes to your child instead of your estate. ”.

These are strategies to leverage both time and appreciation to get assets out of your estate with the goal of saving money on estate taxes.

Estás ingresando al sitio de U.S. Bank en español Algunos materiales y servicios podrían estar disponibles solamente en inglés. Los enlaces incluidos en esta comunicación podrían dirigirte a sitios web en inglés.

Financial guidance and support, tailored for you.

Explore the benefits of personalized wealth services.

Share:

- The two basic trust structures are revocable and irrevocable.

- You can change a revocable trust after you set it up. Moving your assets to a revocable trust can help you avoid probate.

- Once an irrevocable trust is set up, it usually can’t be changed or amended. You can choose from different types of irrevocable trusts based on why you want to set one up.

The world of trusts is not one-size-fits-all. The type of trust you choose should reflect your unique wishes for how your assets are handled now and in the future.

“A trust can help you navigate specific tax concerns or creditor protection, ensure your wealth supports your family, or leave a legacy for a charitable cause you believe in,” says Terry Ruhe, senior vice president and regional trust manager for U.S. Bank Wealth Management. “Whatever your wishes, there’s a trust for you.”

The two basic trust structures are revocable and irrevocable. The biggest difference is that revocable trusts can be changed after they are created, while irrevocable trusts typically cannot.

(There are a few exceptions, though, as state laws can vary considerably.1)

“Both revocable and irrevocable trusts can provide specific benefits depending on your intent,” Ruhe continues.

As stated above, a revocable trust – also referred to as a living trust – is one that can be changed after it’s created. “A revocable trust can accomplish many of the same things as a will. However, there’s one key difference,” says Ruhe. “By creating and transferring your assets to a revocable trust, you can avoid the probate process that’s required for a will.” Probate can be both lengthy and public, and a revocable trust usually is not public.

Because you can make changes to your revocable trust at any time, for certain purposes you are still viewed as the owner of the assets – even though you have a trustee who manages the trust for you. For example, you’ll be responsible for making tax payments and reporting on the trust’s investment returns, and revocable trust assets are includable in your estate and are available to creditors.

You can set up your revocable trust to play out in several different ways, too. You can have your revocable trust end upon your death, and have all assets distributed to your beneficiaries at that time. You can also set it up so that when you pass away, that revocable trust automatically creates irrevocable trusts that continue for different people or institutions.

You typically cannot change or amend an irrevocable trust after it’s created. The assets move out of your estate, and the trust pays its own income tax and files a separate return. This can give you greater protection from creditors and estate taxes.

As stated above, you can set up your will or revocable trust to automatically create irrevocable trusts at the time of your death. When you use your will to create irrevocable trusts, it’s called a testamentary trust. But you can also set up irrevocable trusts during your lifetime.

There are a variety of irrevocable trust types to choose from, depending on your unique circumstances. “Your reason for setting up an irrevocable trust is critical in helping you select one that fits your needs,” says Ruhe. Are you setting up a trust to:

- Transfer wealth to the next generation?

- Keep a family business in the family?

- Leave a legacy with a charity you support?

- Minimize estate taxes for you or your beneficiaries?

- Shield your assets from creditors?

The following are scenarios where these concerns can be addressed through a type of irrevocable trust.

Living Trusts Explained In Under 3 Minutes

FAQ

What trust is best for asset protection?

Irrevocable trust Most trusts can be irrevocable. An irrevocable trust offers your assets the most protection from creditors and lawsuits.

What is the downside of an irrevocable trust?

The main downsides of an irrevocable trust are loss of control over assets, inflexibility and inability to change terms or access assets, higher taxes on trust income, and the complexity and cost of setup and ongoing administration. These problems could cause issues if the grantor’s needs or goals change or if problems with the trustee come up out of the blue.

How to make your assets untouchable?

Want to make your assets virtually untouchable by creditors and lawsuits? Equity stripping may be the answer. This advanced technique involves encumbering your assets with liens or mortgages held by friendly creditors, such as an LLC or trust you control.

What type of trust avoids all taxes?

A Living Trust can help avoid or reduce estate taxes, gift taxes and income taxes, too.

Can an irrevocable trust protect your assets from creditors?

One type of trust that can protect your assets from your creditors is called an irrevocable trust. Once you establish an irrevocable trust, you no longer legally own the assets you used to fund it. With careful planning by your estate planning attorney, you may still be able to indirectly benefit from the assets in the irrevocable trust.

What is the best type of trust?

The best kind of trust depends on your goals. Someone who is focused on avoiding estate tax or making sure their assets are outside of the reach of creditors may want to choose an irrevocable trust—even though that means they can’t change the trust, so they are limited with what they can do with their assets.

What is an asset protection trust?

Asset protection trusts are generally created to protect assets from creditors or for other singular purposes like meeting Medicaid’s asset limit if you have too many assets. There are broadly two types of asset protection trusts that can be created based on your needs—domestic asset protection trusts and foreign asset protection trusts.

What are the different types of asset protection trusts?

There are broadly two types of asset protection trusts that can be created based on your needs—domestic asset protection trusts and foreign asset protection trusts. The National Firearms Act (NFA) limits who can own and transfer firearms. To get around the NFA’s strict rules on paperwork and high taxes, gun trusts are set up.

What is a trust & how does it work?

A trust is a legal arrangement that allows you to separate who owns a given asset from who controls it and who uses it. You can create a trust and transfer assets into it so the trust becomes the new legal owner. You can name a trustee to manage the assets, and the trustee could be yourself or someone else.

Are there different types of trusts for financial security?

There are different trust types for financial security, each offering specific advantages depending on your goals. Whether you’re looking to protect your assets, reduce taxes, or ensure that your estate is distributed according to your wishes, trusts can provide a solid solution.