Theres a lot to like about Roth IRAs, including tax-free withdrawals in retirement. But the accounts do have some cons, such as no upfront tax break, and income limits for contributing.

The products shown on this page are mostly or entirely from our advertising partners. They pay us when you click on one of their links and then do something on our site. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

In the world of retirement accounts, Roth IRAs are a favorite. These accounts allow for tax-free growth and tax-free withdrawals in retirement. They also don’t require you to take money out at a certain age.

That said, everything has a downside, and Roth IRAs have their fair share. Weighing the Roth IRAs benefits and drawbacks could help you decide if and how to incorporate one into your retirement planning.

Hello, fellow money-savvy friends! If you’ve been looking into retirement planning lately, you’ve probably heard a lot of people talking about Roth IRAs like they’re the coolest thing ever. But before you join the crowd, you may be wondering: is a Roth IRA safe? That’s a good question, and I’ll answer it in simple terms down below.

As someone who’s spent way too many hours researching retirement options (seriously my browser history is sad) I can tell you that Roth IRAs have some pretty sweet advantages—but they’re not perfect for everyone. Let’s dive into what makes them tick and whether they deserve a spot in your financial toolbox.

What Exactly Is a Roth IRA?

First things first a Roth IRA is an individual retirement account with a special tax structure. Unlike traditional IRAs, you fund a Roth with money that’s already been taxed (yep the cash you’ve already paid Uncle Sam on). The big selling point? Your money grows tax-free and when you withdraw it in retirement, you don’t pay taxes on it either. Pretty sweet deal, right?

Here’s the basic rundown straight from the IRS:

- You cannot deduct contributions to a Roth IRA (unlike traditional IRAs)

- If you satisfy requirements, qualified distributions are completely tax-free

- You can make contributions after age 70½ (no age restrictions!)

- You can leave amounts in your Roth IRA as long as you live (no required minimum distributions)

- The account must be designated as a Roth IRA when set up

Is a Roth IRA Actually Safe?

We need to be clear about what we mean when we say “safety.” There are different kinds of safety to consider:

1. The Safety of the Account Structure

Federal law sets up Roth IRAs, which have been around since 1997. They are legal ways to invest money, and both the IRS and banks recognize them. When it comes to being a safe way to invest, yes, they are.

2. The Safety of Your Investments

Here’s where things get nuanced. There is no investment in a Roth IRA; it is just a type of account that gives you tax breaks. The things you put your money in within the Roth IRA will determine how safe it really is. You could invest in:

- Super conservative options like CDs or Treasury bonds

- Moderate-risk investments like mutual funds or ETFs

- Higher-risk investments like individual stocks

So when someone asks “is a Roth IRA safe?”, I always wanna say: “Well, that depends on what you put in it!” It’s like asking if a refrigerator keeps food fresh—depends what food you store and how you use it!

3. The Safety from Tax Changes

This is probably the biggest unknown. While current laws make Roth IRAs incredibly attractive with their tax-free growth and withdrawals, tax laws can change. There’s always a possibility (though unlikely) that future legislation could alter how Roth IRA withdrawals are taxed.

The Major Pros of Roth IRAs (Why People Love ‘Em)

Let’s talk about why these accounts have such a fan club:

Tax-Free Growth and Withdrawals

This is the biggie! Once your money’s in a Roth, it grows without you owing taxes on the earnings. And when you take it out in retirement (following the rules), you don’t pay a penny in taxes. This can be HUGE over decades of growth.

No Required Minimum Distributions (RMDs)

Unlike traditional IRAs that force you to take money out starting at age 73, Roth IRAs let you keep your money invested for as long as you want. You’re not forced to cash out investments at potentially bad times just to satisfy government requirements.

Flexibility with Withdrawals

You can withdraw your contributions (but not earnings) at any time without penalties or taxes. This gives you more flexibility than many other retirement accounts, which can be nice if you’re in a pinch.

Tax Diversification in Retirement

If you have a 401(k) or traditional IRA, you’ll pay taxes when you withdraw that money. Having some funds in a Roth gives you the flexibility to manage your tax situation in retirement by choosing which accounts to draw from.

The Downsides of Roth IRAs (Yep, There Are Some)

Every silver lining has a cloud, and Roth IRAs are no exception:

Income Limits Can Be a Pain

Not everyone can contribute directly to a Roth IRA. For 2024, if you’re single with a modified adjusted gross income (MAGI) of $161,000 or more, you can’t contribute at all. For married couples filing jointly, that limit is $240,000.

Here’s a quick breakdown of the 2024 limits:

| Filing Status | Full Contribution Below | Partial Contribution | No Contribution |

|---|---|---|---|

| Single/Head of Household | Less than $146,000 | $146,000 – $160,999.99 | $161,000+ |

| Married Filing Jointly | Less than $230,000 | $230,000 – $239,999.99 | $240,000+ |

| Married Filing Separately (lived with spouse) | N/A | Less than $10,000 | $10,000+ |

No Upfront Tax Break

Unlike traditional IRAs, you don’t get a tax deduction when you contribute. This means higher earners might be better off with traditional IRAs if they expect to be in a lower tax bracket in retirement.

Limited Contribution Amounts

For 2024, you can only contribute up to $7,000 per year ($8,000 if you’re 50 or older). That’s significantly lower than the 401(k) contribution limit of $23,000 ($30,500 for those 50+), which means you’ll probably need additional accounts to save enough for retirement.

Early Withdrawal Restrictions on Earnings

While you can take out your contributions anytime, the earnings part is more complicated. To withdraw earnings tax-free, you generally need to be 59½ or older and have had the Roth IRA for at least 5 years.

Who Should Open a Roth IRA?

I think Roth IRAs make the most sense for:

- Young people just starting their careers (you’ll likely be in a higher tax bracket later)

- People expecting to be in a higher tax bracket in retirement than they are now

- Those who value flexibility and want access to contributions if needed

- Folks who already have tax-deferred accounts like 401(k)s and want tax diversification

- People who want to leave tax-free money to heirs (Roth IRAs are great for this)

Who Might Want to Look Elsewhere?

Roth IRAs might not be the best fit if you’re:

- High earners in peak earning years who expect to be in a lower tax bracket in retirement

- Near retirement age with little time for tax-free growth to compound

- Unable to contribute due to income limits (though the “backdoor Roth” strategy might work for you)

Alternatives to Consider

If a Roth IRA isn’t right for you, don’t worry! There are plenty of other great options:

- Traditional IRAs – Get a tax deduction now, pay taxes later

- 401(k) plans – Higher contribution limits and possible employer matching

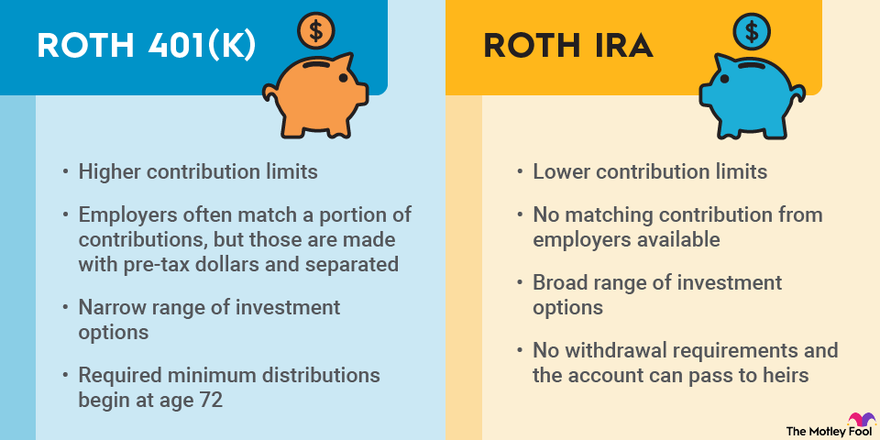

- Roth 401(k)s – Combine the tax-free withdrawals of a Roth with higher contribution limits

- Backdoor Roth IRA – A strategy for high earners to still get Roth benefits

My Personal Take

I’ve gotta be honest – I LOVE Roth IRAs as part of a diversified retirement strategy. The tax-free growth is pretty amazing, especially if you start young. But I don’t think they should be your only retirement vehicle.

The best approach is usually a mix of different account types. Maybe max out your 401(k) match first (hello, free money!), then fund a Roth IRA, then go back to your 401(k) if you can save more. This gives you options in retirement.

Final Thoughts: So, Is a Roth IRA Safe?

The bottom line: Yes, Roth IRAs are generally safe as an account structure, but the actual safety of your investments depends on what you choose to put in the account.

Like any investment vehicle, there are pros and cons to consider. The tax advantages are fantastic, but the income limits, contribution caps, and lack of an immediate tax break might be drawbacks for some people.

If you’re still unsure, talking to a financial advisor who understands your specific situation could help. They can look at your current tax bracket, expected retirement income, and other factors to help you decide if a Roth IRA makes sense for you.

What about you? Have you already started a Roth IRA, or are you still weighing your options? Drop a comment below – I’d love to hear about your retirement planning journey!

Disclaimer: I’m not a financial advisor (just someone who’s obsessed with retirement planning), so please consult with a professional before making any major financial decisions. Tax laws and contribution limits can change, so always check the latest information from the IRS.

Penalty-free withdrawals

Ideally, the money you put away for retirement remains squirreled away and untapped until retirement. But if you need the money quickly, the Roth IRA makes it easier to take money out than the traditional IRA.

You will probably have to pay income taxes and a 2010 early withdrawal penalty if you take money out of a traditional IRA before you turn 59% of the time. (There are some exceptions; read more about traditional IRA withdrawals. ).

With a Roth, you can avoid both taxes and penalties as long as the money you take out is only from the contributions you made. This makes it a cheaper choice when your emergency fund needs access to its own emergency fund. But remember that you can’t put money back into your account and that you might miss out on investment growth.

Roth IRA benefits

The most obvious difference between a traditional IRA and a Roth is how each account deals with taxes. A traditional IRA offers an upfront tax break: Contributions may be deductible in the year they are made to the account. The money grows tax-deferred, but when you pull money out of a traditional IRA in retirement, you owe income taxes.

With the Roth, once youre 59 ½ and have held your Roth IRA for at least five years, you wont have to pay taxes on qualified withdrawals. That can give your savings a powerful boost, especially if you expect your tax rate to be higher in retirement.

» Learn more about the 5-year rule

Roth IRA Explained Simply for Beginners

FAQ

What are the risks of a Roth IRA?

Risks associated with a Roth IRA are not inherent to the account type but often stem from the investments within it or the rules for withdrawals, which include a five-year waiting period to access earnings tax-free and possible penalties for early distributions.

Is it common to lose money in a Roth IRA?

Yes, a Roth IRA can lose money. This isn’t because of how the Roth IRA is set up, but because the money in it is invested in things that can lose value, like stocks or bonds.

What is one negative to a Roth IRA?

No Tax Deduction – Roth IRAs don’t offer a tax deduction for the contributions you make. Instead, you have to wait until retirement to reap the tax benefits. Tax-free withdrawals in your golden years could be an advantage, however, if you anticipate being in a higher tax bracket in retirement.

Does a Roth IRA double every 7 years?

No, a Roth IRA does not necessarily double every 7 years; it depends on the investment’s rate of return, which varies depending on the chosen investments. The “Rule of 72” can help estimate how quickly money doubles; .

Is a Roth IRA good or bad?

Roth IRAs might seem ideal, but they have disadvantages, including the lack of an immediate tax break and a low maximum contribution. Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page.

Are Roth IRA worth it?

Roth IRAs typically yield 7-10% annual returns on average. For instance, if you’re under 50 and just opened a Roth IRA, putting away $6,000 a year for ten years at 7% interest would add up to $83,095. If you wait another 30 years, the account will be worth over $500,000.

Are Roth IRA risky?

Traditional IRAs have immediate tax savings. Roth IRAs, on which taxes are prepaid, may have a future benefit that is less than the prepaid tax. Specifically, there are three risk factors for Roth IRAs. The first risk is the possibility that the IRS or federal income taxes may not exist in the future.