A lot of people think that when they get married, their spouse will automatically get everything if they die. But is this really the case? The answer might surprise you and could save you a lot of trouble in the future.

The Quick Answer: No, Not Always

Contrary to popular belief, a spouse is not always an automatic beneficiary. Whether your spouse automatically inherits your assets depends on several key factors:

- The type of asset in question

- The state you live in

- Any existing legal agreements (like prenups)

- Whether you have a will or not

- Specific beneficiary designations you’ve made

Let’s break down what this means for you and your family.

Assets With Beneficiary Designations: Your Will Doesn’t Matter Here

There are things called “beneficiary designation forms” that can get many of your assets past your will. These are clear instructions about who gets what, and they take precedence over what your will says. Here’s what you need to know:

Non-Probate Assets (They Skip Court)

These assets go directly to the named person without going through probate court:

- Life insurance policies

- Annuities

- Accounts labeled “Payable on Death” (POD)

- Accounts labeled “Transfer on Death” (TOD)

Whoever is named on these forms gets the asset – period. If you named your college roommate as your life insurance beneficiary before you got married and never updated it guess what? Your spouse gets nothing from that policy, regardless of what your will says.

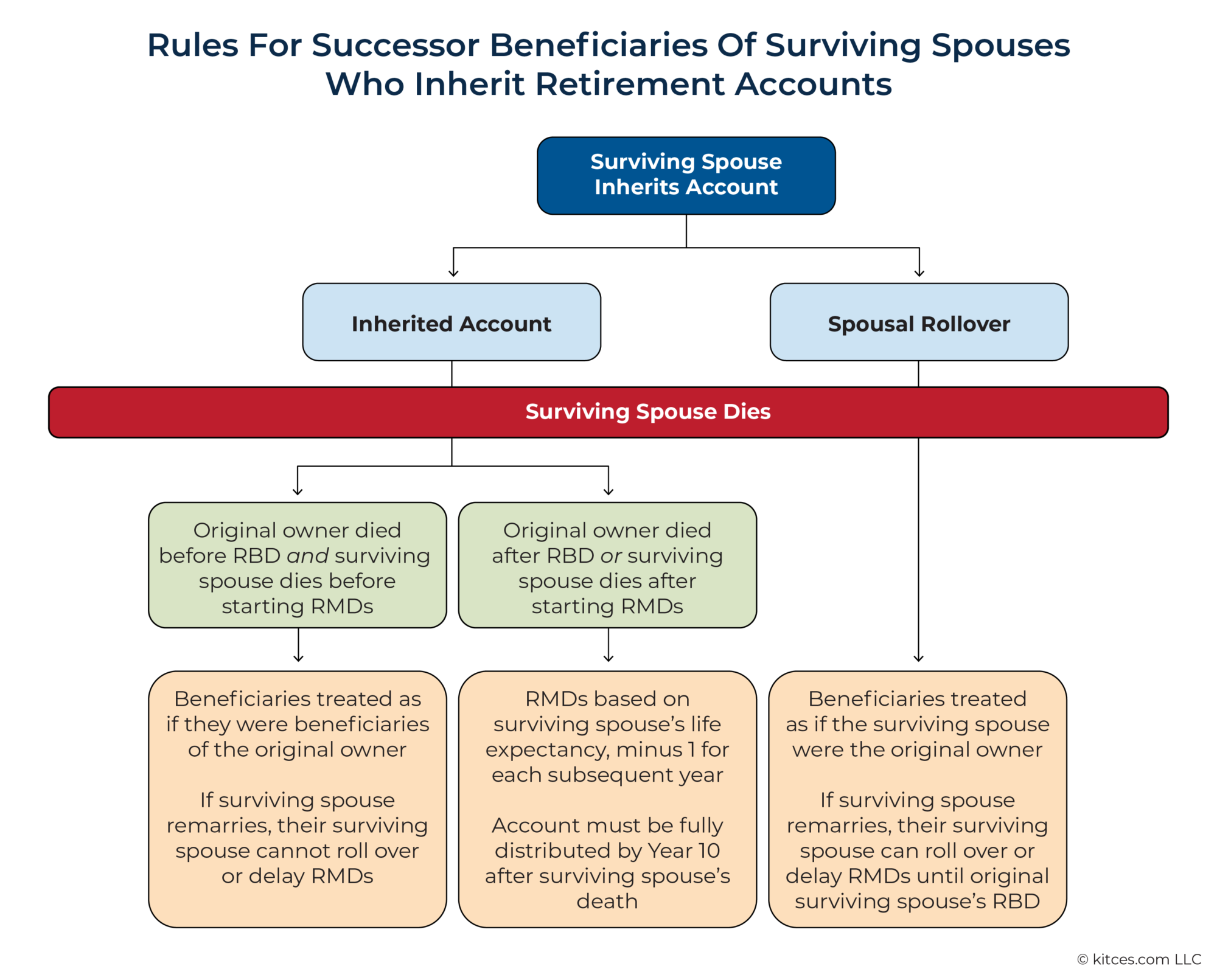

Retirement Accounts: A Special Case

This is where things get tricky – and where many people get blindsided.

For 401(k)s and Similar Employer Plans:

- These are governed by federal law (ERISA)

- Your current spouse IS automatically the primary beneficiary

- To name someone else, your spouse must sign a formal waiver giving up their rights

For Individual Retirement Accounts (IRAs):

- These are governed by state law, not federal

- Your spouse is NOT automatically protected

- You can name anyone as beneficiary without your spouse’s consent or knowledge

This is risky because someone could move money from their 401(k), which protected their spouse, to an IRA, which doesn’t, and their spouse could lose the right to inherit without even knowing it!

What Happens If You Die Without a Will?

If you don’t have a valid will when you die (called dying “intestate”), state laws determine who gets what. Your spouse usually gets priority, but exactly how much they receive varies dramatically based on where you live.

Community Property States vs. Common Law States

In community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin):

- Most property acquired during marriage is jointly owned

- Your spouse automatically inherits your half of community property

- Separate property (gifts, inheritances) might be distributed differently

In common law states (everywhere else):

- Property ownership depends on whose name is on the title

- Your spouse’s inheritance share depends on whether you have children

- Without children, spouse often gets everything

- With children, spouse might get first $50,000 plus half the remainder

People have been shocked to find out that their spouse only got a small part of their estate when someone died in a common law state with children from a previous marriage and no will.

Can Your Spouse Be Completely Cut Out of Your Will?

Most states don’t let you completely disinherit your spouse, even if you try. This protection is called the “elective share.”

The elective share allows a surviving spouse to reject what they were left in the will and instead claim a legally defined percentage of the estate (usually between 1/3 and 1/2). But this isn’t automatic – your spouse has to formally file a claim with the court.

Some states have a sliding scale based on how long you’ve been married – longer marriages result in a higher percentage. This protects spouses in newer marriages from being completely disinherited.

Prenups and Postnups Can Change Everything

Through prenuptial agreements (signed before marriage) or postnuptial agreements (signed after), spouses can waive their inheritance rights. This includes giving up:

- The right to an elective share

- Rights under intestate succession laws

- Claims to specific assets

For these waivers to be enforceable, the agreement must be:

- In writing

- Signed voluntarily

- Made after full financial disclosure by both parties

We often see these agreements used to protect assets for children from previous relationships or to keep family businesses within the bloodline.

Real-World Examples That Might Surprise You

Case #1: The Forgotten Beneficiary Form

John and Mary were married for 20 years. In his will, John left everything to Mary. However, he never updated the beneficiary form on his life insurance policy, which still named his sister from before his marriage. When John died, the $500,000 policy went to his sister, not Mary – despite what his will stated.

Case #2: The IRA Rollover Mishap

When Sarah changed jobs, she rolled her 401(k) into an IRA but forgot to name her husband Michael as beneficiary. Her previous 401(k) had automatically protected him, but the IRA didn’t. When Sarah unexpectedly passed away, the entire IRA went to her adult children from a previous marriage instead of Michael.

Case #3: The Intestate Surprise

Tom died without a will, assuming his wife Jennifer would get everything. But because they lived in a common law state and had children, Jennifer only received $100,000 plus half the remaining estate. The rest was divided among their children, creating tax complications and limiting Jennifer’s access to funds she needed for retirement.

Practical Steps to Protect Your Spouse (If That’s What You Want)

If you want to ensure your spouse inherits your assets, here’s what you should do:

- Create a will that clearly states your wishes

- Review beneficiary designations on all accounts regularly, especially after major life events

- Understand your state’s inheritance laws and how they apply to your situation

- Consider estate planning tools like trusts that can provide more control

- Update everything after major life events like marriage, divorce, births, or deaths

- Consult with an estate planning attorney familiar with your state’s laws

When You Might NOT Want Your Spouse to Inherit Everything

There are legitimate reasons why you might not want your spouse to automatically inherit everything:

- You have children from a previous relationship you want to provide for

- You own a family business that should stay within your bloodline

- Your spouse may not have the financial knowledge to manage certain assets

- Tax planning considerations make other arrangements more beneficial

- Your spouse has agreed to alternative arrangements

In these cases, proper estate planning is even more crucial to ensure your wishes are carried out legally.

Common Questions People Ask Us

Does a spouse automatically inherit a house?

Not necessarily. If the house is jointly owned with rights of survivorship, then yes. But if it’s solely in your name, it depends on your will or state intestacy laws. In some states, your spouse might only receive a portion of the house’s value, forcing a sale or creating co-ownership with your children or other heirs.

Can my spouse contest my will if I leave everything to someone else?

In most states, yes. Your spouse can typically claim their elective share regardless of what your will says. The percentage varies by state, but it’s usually between one-third and one-half of your estate.

If I die without a will, does my spouse get everything?

It depends on your state and whether you have children or other living relatives. In some states, if you have children, your spouse might only get a portion of your estate, with the remainder going to your children. If you don’t have children but have living parents, they might be entitled to a portion in some states.

The Bottom Line: Take Control of Your Estate Plan

The assumption that spouses automatically inherit everything is one of the most common and potentially costly misconceptions in estate planning. The truth is much more complicated – and if you don’t take control of the process, state laws and old paperwork might determine your spouse’s financial future in ways you never intended.

Don’t leave these important decisions to chance or outdated forms. Take the time to create a comprehensive estate plan that reflects your wishes and protects those you love.

I’ve seen too many families thrown into financial and emotional turmoil because someone assumed their spouse would automatically inherit their assets. Don’t let your family be one of them.

Have you updated your beneficiary designations recently? Is your will current? These might be the most important financial documents you ever sign.