As a financial planner, I’ve noticed many clients are confused about whether they can put their Roth IRA in a trust. The short answer is you can name a trust as the beneficiary of your Roth IRA but a trust cannot directly own a Roth IRA during your lifetime. This distinction is crucial for proper estate planning and getting it wrong could cost your heirs thousands in unnecessary taxes.

I’ll walk you through everything you need to know about Roth IRAs and trusts – from the legal requirements to the common mistakes people make that can derail their estate plans.

Understanding the Relationship Between Trusts and Roth IRAs

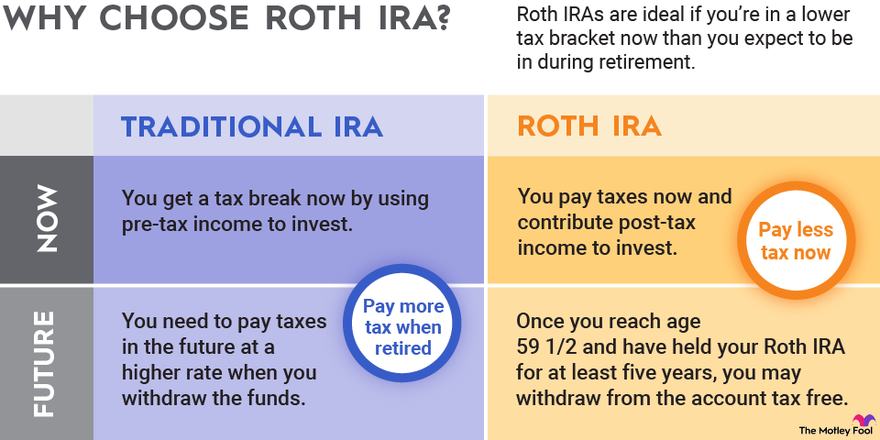

Roth IRAs are incredibly valuable retirement vehicles that offer tax-free growth and withdrawals. Unlike traditional IRAs, Roth contributions are made with after-tax dollars, and distributions are tax-free as long as you’re at least 59½ years old and have had the account for at least five years.

When it comes to trusts, though, things get complicated. Here’s what you need to understand:

- During your lifetime: You cannot transfer ownership of your Roth IRA to a trust. The IRA must remain in your name.

- After your death: You can designate a trust as the beneficiary of your Roth IRA.

This difference is very important because a lot of people think they can just move their Roth IRA into their living trust, but that’s not how it works!

Legal Requirements for a Trust as Roth IRA Beneficiary

If you want your Roth IRA to pass to a trust when you die you need to make sure the trust meets specific IRS requirements to receive favorable tax treatment. The trust must

- Be a valid legal entity under state law

- Meet the IRS’s “see-through” requirements

- Become irrevocable upon your death

- Have clearly identifiable beneficiaries

- Provide proper documentation by October 31 of the year following your death

The “see-through” trust requirement is particularly important. This means the IRS can “see through” the trust to identify the actual human beneficiaries. Without this qualification, your beneficiaries might lose valuable tax advantages.

Types of Trusts for Roth IRA Beneficiaries

When it comes to inheriting Roth IRAs, not all trusts are the same. The two main types to consider are:

Conduit Trusts

With a conduit trust, all distributions from the Roth IRA must pass directly to the trust beneficiaries. This preserves the tax advantages of the Roth IRA because the money doesn’t accumulate inside the trust where it could face higher tax rates.

Accumulation Trusts

With an accumulation trust, the trustee can keep distributions inside the trust instead of giving them to beneficiaries right away. This gives you more control, but it also has a big downside: any income held in the trust that is more than $15,200 (as of 202024) is taxed at the highest federal rate of 33%. Ouch!.

How the SECURE Act Changed the Game

The SECURE Act of 2019 made big changes to how inherited retirement accounts work. This includes Roth IRAs that are held in trusts. Before this law, beneficiaries who were not married could spread out their payments over their whole lives. Most beneficiaries must now take all assets within 10 years of the death of the original owner.

There are exceptions for certain “eligible designated beneficiaries” including:

- Disabled or chronically ill individuals

- Minor children of the original account owner (until they reach adulthood)

- Beneficiaries less than 10 years younger than the deceased

These changes make trust planning for Roth IRAs even more complex and underscore the importance of working with a qualified professional.

Transfer Mechanics When a Trust Inherits a Roth IRA

When you die and your trust becomes the beneficiary of your Roth IRA, several steps must occur:

- The financial institution managing the IRA must be notified of your death

- The account is transferred into an inherited Roth IRA

- The new account is titled according to IRS guidelines, typically as “[Your Name] Roth IRA (Deceased) FBO [Trust Name]”

Not all financial institutions handle trust-owned IRAs the same way. Some require additional documentation like a copy of the trust agreement or a certification of trust. Others may not allow inherited Roth IRAs to be held in trust at all, necessitating a transfer to a different custodian.

4 Common Mistakes People Make With Roth IRAs and Trusts

In my years of practice, I’ve seen clients make the same mistakes over and over. Here are the big ones to avoid:

1. Failing to Name a Beneficiary

This is probably the most obvious error Roth IRA owners make. If you don’t explicitly list a beneficiary, the account transfer may be determined by your will, which can be complicated, costly, and time-consuming. Always name your beneficiaries as soon as you open the account and update them whenever your circumstances change.

2. Choosing the Wrong Beneficiary

Married couples usually list each other as primary beneficiaries of their Roth accounts. When one spouse dies, the other inherits the money, which is then passed on again upon the death of the second spouse.

But leaving a Roth to a younger beneficiary may trigger estate or generation-skipping transfer taxes in some cases. This is where expert advice becomes invaluable.

3. Establishing a Trust Incorrectly

If you’ve decided to use a trust, it’s essential to set it up correctly. The trust documents must clearly spell out all details about distributions and beneficiaries. Otherwise, the IRS may require that the trust disperse all income in the account within five years rather than the typical 10 years.

Common mistakes include:

- Not making the trust irrevocable upon death

- Failing to identify all beneficiaries

- Using incorrect language regarding RMDs

- Not including provisions to prevent disqualifying modifications

4. Neglecting Required Minimum Distributions (RMDs)

This is primarily a mistake that beneficiaries make. While you as the original Roth IRA owner don’t need to take RMDs during your lifetime, your beneficiaries (including trusts) generally will have to follow distribution rules.

Under the SECURE Act, most non-spouse beneficiaries have up to 10 years to fully distribute all funds in an inherited Roth IRA. The account must be completely emptied by December 31 of the 10th year following your death.

For those who qualify as eligible designated beneficiaries, RMDs must begin as early as December 31 of the year following your death.

Trustee Responsibilities for Inherited Roth IRAs

If you’re named as a trustee of a trust that inherits a Roth IRA, you have significant responsibilities:

- Managing investments within the inherited Roth IRA

- Ensuring compliance with trust provisions and IRS regulations

- Maintaining accurate records of all transactions

- Balancing risk and return in investment selections

- Communicating transparently with beneficiaries

Trustees must understand the unique nature of Roth IRAs and the tax implications of their decisions. Poor management could significantly reduce the benefits of the Roth structure and impact the financial security of beneficiaries.

Tax Considerations for Trust-Owned Roth IRAs

While Roth IRA distributions are generally tax-free, how the trust handles these distributions affects overall tax efficiency:

- Conduit trusts pass Roth IRA distributions directly to beneficiaries, preserving their tax-free status

- Accumulation trusts that retain distributions may face high trust tax rates on any earnings from reinvested distributions

- The full value of a Roth IRA is included in the account holder’s taxable estate, potentially triggering estate taxes for larger estates (over $13.61 million in 2024)

Is Using a Trust for Your Roth IRA Right for You?

Using a trust as a Roth IRA beneficiary makes sense in certain situations:

- You want to control how and when beneficiaries receive funds

- You have beneficiaries with special needs or who require protection

- You’re concerned about creditor issues for your heirs

- You have minor children who can’t directly inherit the IRA

- You want to protect the assets from a beneficiary’s spouse in case of divorce

However, the added complexity and potential for mistakes means this strategy isn’t right for everyone. Smaller Roth IRAs may not justify the expense and complexity of trust planning.

Final Thoughts: Proceed With Expert Guidance

If you’re considering naming a trust as your Roth IRA beneficiary, don’t try to DIY this complex area of estate planning. The rules are intricate, and the penalties for getting it wrong can be severe. Work with both a financial advisor experienced in retirement accounts and an estate attorney familiar with the latest IRS regulations.

Remember, while a trust cannot own your Roth IRA during your lifetime, properly designating a trust as your beneficiary can provide valuable protection and control for your heirs – if done correctly.

Have you considered using a trust for your Roth IRA? What questions do you still have about this complex topic? I’d love to hear your thoughts in the comments!

Should I Put My Brokerage, 401(K) or IRA in My Trust? | Bethel Law

FAQ

Can an irrevocable trust be the owner of an IRA?

You can’t put an IRA directly into an irrevocable trust while you’re still alive, because the IRA must still belong to the person who put it in. You can instead name a qualifying trust as the beneficiary of your IRA, which will decide how and when the money is given out after you die.

Why don’t you put an IRA into a trust?

When you move money from a retirement account to a trust, the taxes on the money haven’t been paid yet because the account is tax-deferred.

Can a trust be a Roth IRA beneficiary?

There are specific legal requirements, tax implications, and administrative complexities involved. A trust can be named as a Roth IRA beneficiary, but it must comply with IRS regulations. To qualify for favorable tax treatment, the trust must be a valid legal entity under state law and meet the IRS’s “see-through” requirements.

Can an IRA be owned by a trust?

The IRS states that an IRA can only be owned by an individual. Property can be held and managed by a trust, which is a legal entity that is frequently used to distribute assets to beneficiaries. Ownership of assets is transferred to the trust by the person who creates it, known as the grantor.

Can I transfer my Roth IRA to a trust?

Trusts are not considered individuals, so transferring ownership of your Roth IRA to a trust would violate IRS regulations. Tax Consequences: If you were to transfer ownership of your Roth IRA to a trust, it would be treated as a distribution, triggering immediate income taxes on the entire balance.

Can a Roth IRA be passed through a living trust?

Build your living trust online, with step-by-step tools and optional attorney support for peace of mind. When you pass your Roth IRA through a living trust, your beneficiaries will receive the Roth assets tax-free. Doing this also allows you to “stretch your IRA.”

Can inherited Roth IRAs be held in trust?

Not all custodians allow inherited Roth IRAs to be held in trust, so transferring the account to a custodian that permits trust ownership may be necessary. Improper transfers can trigger unintended distributions or administrative complications.

What happens if you pass a Roth IRA through a trust?

Once you do this, the Roth will automatically be payable to the trust upon your death. When you pass your Roth IRA through a living trust, your beneficiaries will receive the Roth assets tax-free. Do IRA owners need a trust?