When you’re dealing with the loss of a loved one, the last thing you want to worry about is taxes. But if you’ve received a lump sum death benefit, understanding the tax implications is crucial for your financial planning. I’ve helped many clients navigate this confusing terrain, and I’m here to break it down in simple terms

Understanding Lump Sum Death Benefits

When someone dies, a lump sum death benefit is a payment made to a beneficiary. These payments usually come from

- Life insurance policies

- Employer-provided plans

- Retirement accounts (like 401(k)s or IRAs)

- Pension plans

The big question is: do you have to pay taxes on this money? Well, it depends on the source of the benefit and several other factors.

Are Life Insurance Death Benefits Taxable?

Good news! You don’t have to pay taxes on most life insurance death benefits. Section 101(a) of the Internal Revenue Code says that when you get a lump sum payment from a life insurance policy, it usually goes to the beneficiaries tax-free.

However, there are some exceptions:

- If you receive the death benefit in installments that include interest, the interest portion is taxable

- If the policy was transferred for value (sold or assigned to someone else), the proceeds might be partially taxable

- If the death benefit goes to the deceased’s estate, it could be subject to estate taxes if the estate exceeds exemption limits

Employer-Provided Death Benefits

As part of their benefits package, many companies offer death benefits. In the case of the Illinois Municipal Retirement Fund (IMRF), the death benefit is equal to one year’s salary plus member contributions and interest for active members and $3,000 for retired members.

Unlike life insurance, employer-paid death benefits like those from IMRF are usually taxable. Why? Because the employer pays for the benefit, not the employee with after-tax dollars.

If you’re a spouse beneficiary receiving an employer death benefit, you have two options:

- Receive the payment directly (20% federal tax withholding required)

- Roll over the benefit into a traditional IRA or qualified retirement plan (tax-deferred until withdrawal)

Non-spouse beneficiaries can roll the payment into an inherited IRA, which has different distribution rules than regular IRAs.

Retirement Plan Death Benefits

Death benefits from retirement plans like 401(k)s and IRAs have different tax rules:

- These distributions are generally included in the beneficiary’s income

- They’re taxed at ordinary income tax rates

- Under the SECURE Act, most beneficiaries must withdraw the entire balance within 10 years

- Eligible designated beneficiaries (like surviving spouses and minor children) have exceptions

Tax-free withdrawals may be possible if certain conditions are met if the retirement account was a Roth IRA.

How to Report a Death Benefit on Your Tax Return

If you’ve received a taxable death benefit, you’ll need to report it on your tax return. Here’s how:

- For employer death benefits: Report on the pension line of IRS Form 1040 or 1040A

- For retirement account distributions: You’ll receive Form 1099-R showing the distribution amount

Let’s look at some examples from IMRF:

Example 1: $15,000 Death Benefit – Entire amount paid to you

- Box 1 (gross distribution) on Form 1099-R shows $15,000

- Box 2a (taxable amount) shows $15,000

- Include $15,000 in Box a on Form 1040/1040A and $15,000 in Box b

Example 2: $15,000 Death Benefit – $8,000 paid to you, $7,000 rolled over

- You’ll receive two Forms 1099-R

- Show the total death benefit of $15,000 in Box a on Form 1040/1040A

- Show $8,000 (the amount not rolled over) in Box b

State Income Tax Considerations

Don’t forget about state taxes! Each state has different rules regarding death benefits:

- Some states fully exempt these benefits from taxation

- Others impose taxes based on the benefit type

- Some consider the relationship between the deceased and beneficiary

For instance, Pennsylvania has an inheritance tax that could affect your net benefit. It’s definitely worth checking your specific state’s regulations.

Strategies to Minimize Tax Impact

If you’re facing taxes on a death benefit, consider these strategies:

- Rollovers: If you’re a spouse, rolling over the benefit to an IRA can defer taxes

- Charitable contributions: Donating part of the benefit to charity may provide a tax deduction

- Installment payments: In some cases, taking the benefit over time rather than as a lump sum might lower your overall tax burden

- Estimated tax payments: If the distribution increases your annual income significantly, making estimated tax payments can help avoid penalties

Steps for Claiming Death Benefits

To claim a death benefit, follow these steps:

- Identify which company holds the policy or benefit

- Complete a death claim form with the required information (policy number, name, SSN, date of death)

- Submit the form along with a certified death certificate

- Choose your preferred payment method (lump sum or installments)

If multiple beneficiaries are listed, each person must complete a claim form.

Real-World Example

My client Sarah received a $50,000 death benefit from her husband’s employer-provided plan. Since she was worried about taxes, we decided to roll $35,000 into her IRA and take $15,000 as a direct payment for immediate expenses. This strategy helped her manage her cash flow needs while minimizing the immediate tax impact.

Understanding whether a lump sum death benefit is taxable can save you from unexpected tax bills during an already difficult time. While life insurance proceeds are generally tax-free, benefits from employers and retirement plans often have tax implications.

I always recommend consulting with a tax professional who can provide guidance specific to your situation. Everyone’s circumstances are different, and tax laws can change over time.

Have you received a death benefit or are you planning for one? What questions do you still have about the tax implications? Feel free to reach out – we’re here to help make these difficult financial decisions a bit easier.

Do you have an Intuit account?

Youll need to sign in or create an account to connect with an expert. 4 Replies

I am going to be receiving a lump sum from a death benefit. Is this taxable and if so is there some way I can avoid that by putting it into another account?

Its not clear what you mean by a “death benefit. ” If its just a cash inheritance from the deceased persons ordinary assets, its not taxable. You dont even report it on your tax return. If its from an IRA, pension, or other tax-sheltered plan, or from a trust, provide more details, including your relationship to the deceased.

Is The Lump Sum Death Benefit Taxable? – Wealth and Estate Planners

FAQ

Are death benefits paid to the beneficiaries tax free?

Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren’t includable in gross income and you don’t have to report them. However, any interest you receive is taxable and you should report it as interest received.

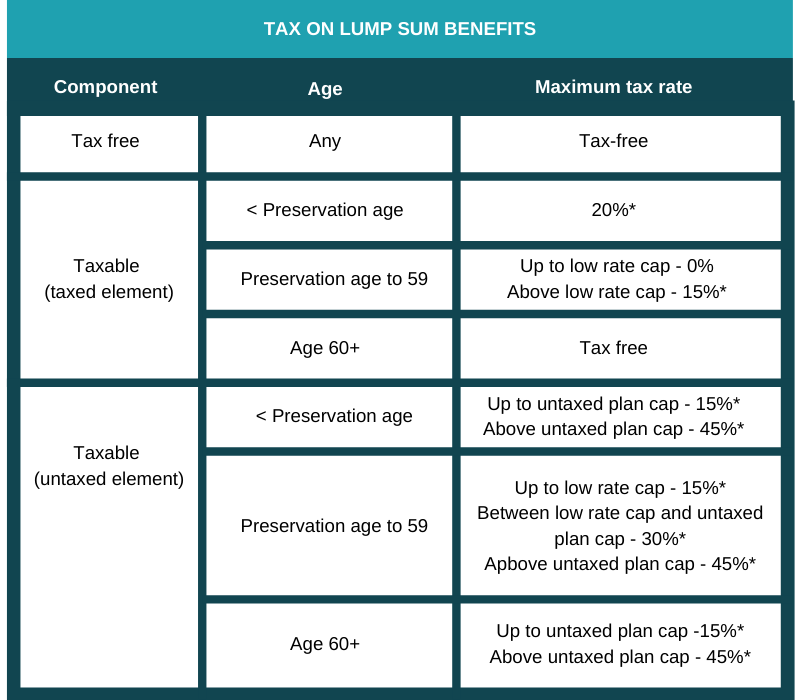

How much of lump sum payout is tax free?

Retirement fund lump sum benefits or severance benefitsTaxable%20income%20(R)%E2%80%8BRate%of%20tax1%20%E2%80%93%20550%2000%%20of%20taxable%20income550%20001%20%E2%80%93%20770%2000018%%20of%20taxable%20income%20above%20550%20000770%20001%20%E2%80%93%201%20155%2000039%20600%20 %2027%%20of%20taxable%20income%20above%20770%200001%20155%20001%20and%20above143%20550%20 %2036%%20of%20taxable%20income%20above%201%20155%20000

Are death benefits considered earned income?

In many cases, the money your beneficiaries receive from a life insurance payout is not taxed as income. However, there are a few exceptions that we’ll go over below.

Do you have to pay tax on money received as a beneficiary?

People who inherit money or property usually don’t have to pay income tax on it. However, there are some exceptions, like retirement accounts, life insurance proceeds, and savings bond interest. If the money you inherit from a 401(k), 403(b), or IRA was tax-deductible when it was put in, you have to pay taxes on it.

Are lump sum death benefits taxable?

Maintaining detailed records, including receipts and acknowledgments from charitable organizations, is essential for claiming these deductions. Accurate reporting of lump sum death benefits on tax returns is critical. Beneficiaries must determine the taxable portion of the benefit, which depends on the source and type of benefit.

Is a lump sum death benefit paid under FERS taxable?

The amount of lump sum death benefit payment under FERS is not subject to Federal income tax because the original contributions were previously taxed. However, any interest paid on these contributions is taxable in the year the refunded contributions are paid. “Trans” FERS Employees – What Should They Do?

Can a beneficiary receive a lump sum distribution if he dies?

Share the benefits of a lump sum distribution. Upon your death, a beneficiary can decide how they want to receive the death benefit. The beneficiary can choose either a lump sum payment, interest payments, or another option. Choosing a lump sum payment will help the beneficiary avoid taxation on interest.

What is a lump sum death benefit?

A lump sum death benefit is a payment made to a beneficiary upon the death of the insured individual. This benefit is typically associated with life insurance policies, but it can also arise from other sources such as pensions or annuities. Taxability of Lump Sum Death Benefits:

Is a $3,000 death benefit taxable?

The $3,000 death benefit is a taxable distribution for the surviving spouse. However, the surviving spouse can consider two options: having the $3,000 made payable to them or rolling it over into a traditional (not a Roth) IRA, Roth IRA, qualified plan, 457 or 403(b) plan. If the $3,000 is rolled over, IMRF will report a taxable amount of $0.

Are death benefits taxable?

However, interest earned on the benefit amount after death may be taxable. Split-dollar arrangements, where the employer and employee share ownership, may have different tax implications. Beneficiaries should also review state-specific tax codes, as states can have varying rules regarding death benefit taxation.