One of the most important questions you’ll have to answer when planning for retirement is, “How long does a pension last?” The answer can have a big effect on your peace of mind and financial security in your golden years. Let’s talk about your options and everything you need to know about how long your pension will last.

The Basics: How Long Does a Traditional Pension Last?

A traditional pension typically provides guaranteed income for life. Unlike other retirement funds that can run out, pension payments keep coming in until the person dies. This gives you a steady source of income during your retirement years.

For most retirees, this means your pension could last 20+ years. With average life expectancies of 81 for males and 84 for females, your pension might need to sustain you for over two decades after retirement.

Understanding Your Pension Payment Options

When retiring with a pension, you’re typically offered several ways to receive your benefits:

1. Monthly Payments (Traditional Pension Annuity)

- Duration: Guaranteed for life

- Control: Managed by plan administrator

- Stability: Fixed monthly income

- Inflation: Typically no built-in protection

- Legacy: Limited or no inheritance options

2. Lump Sum Payout

- Duration: Depends on your management

- Control: Complete control over funds

- Flexibility: Freedom to spend or invest

- Risk: You bear investment and longevity risk

- Legacy: Potential to leave remaining funds to heirs

3. Annuity with Guaranteed Lifetime Withdrawal Benefit (GLWB)

- Duration: Guaranteed for life

- Control: More control than traditional pension

- Growth: Potential for payment increases

- Protection: Market downside protection

- Legacy: Possibility to leave funds for heirs

How Pension Benefits Are Calculated

Understanding how your pension is calculated helps explain how much you’ll receive throughout retirement

Pension Benefit = Years of Service × Multiplier × Final Average Salary- Years of Service: The qualifying years worked for your employer

- Final Average Salary: Typically the last 3-5 years of compensation

- Multiplier: Usually around 2% (determines percentage of salary received)

For example if you work 30 years with a 2% multiplier and a final average salary of $75000, your annual pension would be 30 × 2% × $75,000 = $45,000 per year

This becomes your guaranteed lifetime income, which means your “replacement rate” is 60% (30 years × 2%) of your final salary.

Monthly Pension vs. Lump Sum: Which Lasts Longer?

The longevity of your retirement funds depends largely on which option you choose:

Monthly Pension Payments

- Guaranteed for life regardless of how long you live

- No risk of outliving your money

- Managed by professionals, no investment decisions needed

- May not keep pace with inflation over time

- Payments typically end upon death (or spouse’s death)

Lump Sum Option

- Duration depends on your management and withdrawal rate

- Potentially depleted before death if poorly managed

- Subject to market fluctuations and investment risks

- Can be invested to potentially keep pace with inflation

- Remaining funds can be passed to heirs

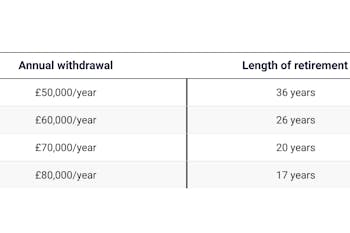

Many financial advisors reference the “4% rule” for lump sums, suggesting withdrawing 4% annually with inflation adjustments. However, market downturns could jeopardize this approach.

Factors Affecting How Long Your Pension Will Last

Several key factors influence the duration and sustainability of your pension

1. Life Expectancy

Your personal health history and family longevity play crucial roles. If you think you’ll live longer than most people, monthly payments may be worth more over time.

2. Inflation Considerations

Traditional pension payments rarely include inflation protection, meaning your buying power will likely decrease over time. A $45,000 pension today won’t buy the same goods and services in 20 years.

3. Financial Management Skills

If taking a lump sum, your investment knowledge and discipline directly impact how long your money lasts. Poor decisions could deplete funds prematurely.

4. Retirement Income Needs

Matching your guaranteed income (Social Security + pension) against essential expenses helps determine which option provides better security.

5. Estate Planning Goals

If giving money to your heirs is important to you, a lump sum is a better way to do it than regular pension payments.

Making the Right Choice for Your Situation

To determine which option might work best for you, consider these steps:

- Analyze your essential expenses vs. guaranteed income sources

- Consider your health and family history for longevity expectations

- Evaluate your investment experience and risk tolerance

- Review your wealth transfer plans and inheritance goals

- Consult with a financial advisor for personalized guidance

Beyond Traditional Options: The GLWB Alternative

An annuity with a Guaranteed Lifetime Withdrawal Benefit (GLWB) offers an interesting middle ground between monthly pension payments and lump sums.

With a GLWB, you can:

- Secure lifetime income (like a pension)

- Maintain some control over principal

- Potentially see income increases over time

- Leave remaining funds to heirs

- Protect against market downturns

Many retirees find this option provides more flexibility and security than either traditional pension payments or managing a lump sum independently.

Tax Implications and Your Pension’s Longevity

The tax treatment of your pension can significantly impact how long your money lasts:

- Monthly payments are taxed as ordinary income when received

- Lump sum payments face immediate taxation unless rolled into a qualified account

- Early withdrawals (before age 59½) may incur a 10% penalty

Proper tax planning is essential to maximize your pension’s longevity. Rolling a lump sum into an IRA can maintain tax-deferred status and preserve more of your retirement funds.

What Happens to Your Pension When You Die?

Understanding the legacy aspects of your pension is important:

- Traditional pension payments typically end upon death or continue to a surviving spouse at a reduced rate

- Lump sum options allow remaining funds to be passed to any beneficiaries

- GLWB annuities often include death benefits for heirs

Some pension plans offer “life and period certain” options that guarantee payments for a minimum period (like 15 or 20 years) even if you die before that period ends.

Real-World Considerations

Here’s what we’ve seen work for many retirees:

- If your guaranteed income just covers essential expenses, keeping monthly payments provides security

- If you have substantial other savings or income sources, a lump sum offers flexibility

- If you’re uncertain about managing investments, monthly payments reduce stress

- If inflation protection is important, consider either a lump sum or GLWB annuity

Next Steps: Securing Your Retirement Income

To make the most of your pension:

- Confirm your eligibility and benefit options with current or former employers

- Keep contact information updated with pension administrators

- Consider tax implications before making decisions

- Consult a financial advisor for personalized analysis

- Compare all options including traditional payments, lump sums, and GLWB annuities

The question of how long a pension lasts has different answers depending on your choices. Traditional pension payments are guaranteed for life, while lump sums last as long as you manage them to last. Your personal circumstances, health, financial goals, and risk tolerance should guide your decision.

Whichever option you choose, careful planning ensures your retirement income serves you well throughout your golden years. After all, pensions are designed to provide financial security when we’re no longer working – making the right decision about yours is one of the most important retirement choices you’ll make.

Remember, there’s no one-size-fits-all answer. What works for your friend, neighbor, or colleague might not be best for you. Take time to evaluate your options, consult professionals, and choose the path that offers the greatest security and satisfaction for your unique situation.

A Government Pension – What You Should Know

FAQ

How long does my pension have to last?

In this case, if you want to retire at age 68 and hope to live to be 90, your retirement would last about 22 years. In this case, it’s worth planning for your money to last for at least 25 years.

Do pension payments ever stop?

Yes, pensions can end if the fund’s assets aren’t enough to cover its debts. This can happen if investments don’t do well, people don’t put enough money into the fund, the economy goes down, or people don’t think they will live as long as they thought they would.

What is the average pension payout?

There is no such thing as an “average” pension payout because it depends so much on the person, the plan, and the industry. However, new data from 2025 shows that the median annual income for US households aged 65 is between $56,000 and $57,000, or about $4,700 per month, with a higher mean (average) of around $87,000.

What is the 10 year rule for pension?

If you retire under the Rules and have qualifying service of 10 years, your pension is calculated @ 50% of last pay or average emoluments (i.e. average of the basic pay drawn by you during the last 10 months of your service), whichever is more beneficial to you.

How long do pension payments last?

Depending upon the specific pension plan you choose, payments may continue up until your death or pass on to a designated survivor. When you reach retirement, you typically have the chance to choose between several different pension payment plans that determine how long you receive payments.

What is a pension & how does it work?

A pension is a retirement account that an employer maintains to give you a fixed payout when you retire. It’s a kind of defined benefit plan. Your payout typically depends on how long you worked for your employer and on your salary. When you retire, you can choose between a lump-sum payout or a monthly “annuity” payment.

How long does a private pension plan last?

Some plans may last for a fixed number of years, while others may continue until the retiree’s death. The length of time that a private pension plan lasts is often determined by factors such as the employee’s age, years of service, and the retirement age specified in the plan. One common type of private pension plan is a defined benefit plan.

How long should a pension plan be?

The duration of a pension plan can vary depending on factors such as the age at which the plan is started, the individual’s retirement goals, and the type of pension plan. It is important for individuals to assess their own financial situation and goals before determining the length of their pension plan.

Should I keep my monthly pension payments?

Pension plans typically provide for the payment of a set amount every month from your retirement date for the rest of your life (“an annuity”). You may also choose to receive lifetime payments that continue to your spouse after your death. 1 These monthly payments do have drawbacks, however:

How does the duration of a pension plan affect retirement age?

The duration of a pension plan can also affect an individual’s retirement age decision. If the pension plan has a long duration, individuals may choose to retire earlier, knowing that their financial needs will be met for a longer period.