Whether it helps you qualify for a new credit card or secure the best interest rate on your mortgage, your credit score has a big impact on your finances.

While there are a few different types of credit scores, the one youâre most likely familiar with (and the one thatâs most widely used) is the FICO Score, which ranges from 300 to 850. Anything less than 580 is considered âpoor,â and âgoodâ scores start around 670.

But what are the five factors that affect your credit score? Hereâs what to know about each of them, and how heavily they are weighted into your score.

Your credit score plays a huge role in your financial life. It impacts everything from whether you can qualify for a loan or credit card to how much interest you’ll pay. So it’s important to understand what goes into calculating this all-important three-digit number.

There are a few different credit scoring models, but the most commonly used one is the FICO score, which ranges from 300 to 850 The higher the score, the better Anything above 700 is generally considered good credit.

FICO scores are calculated based on information in your credit reports from the three major credit bureaus – Equifax, Experian and TransUnion. Each bureau may have slightly different information about your credit history, which is why you can have multiple credit scores.

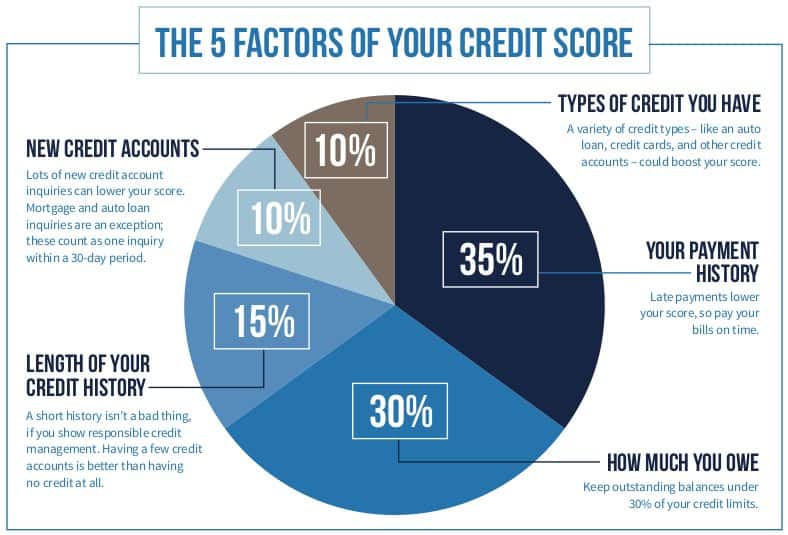

When calculating your FICO score, five main factors are considered:

1. Payment History

How you’ve paid your bills in the past is the most important factor, accounting for 35% of your FICO score.

Your payment history shows lenders whether or not you’ve paid debts on time. When you make payments as agreed, it gets reported to the credit bureaus and you build up a positive track record over time.

Missing payments, especially if they are 30 days or more late will damage your credit score the most. A history of late payments signals risk to lenders. An account sent to collections also devastates your score.

To improve your payment history

- Set up automatic payments on loans and credit cards to avoid late payments.

- Check credit reports for errors and dispute any inaccurate late payments.

- Bring past due accounts current and continue paying on time going forward.

2. Credit Utilization

The second biggest factor is your credit utilization ratio – how much of your total available credit you’re using. This makes up 30% of your FICO score.

Lenders want to see you’re able to manage credit responsibly, without “maxing out” your cards or having an excessive reliance on credit.

To calculate your utilization, add up your balances and divide it by your total credit limits. For example, if you have $2,000 in balances across credit cards with a total $10,000 limit, your utilization is 20%.

Experts recommend keeping this ratio below 30%, but lower is better. High utilization signals risk, while low utilization shows you’re not over-reliant on credit.

To improve your utilization ratio:

- Pay down balances, especially on cards close to their limits.

- Ask for credit limit increases on existing accounts.

- Balance transfers to a new card with an intro 0% APR.

3. Credit History Length

The third factor considered is the length of your credit history, accounting for 15% of your FICO score. This reflects how long you’ve been managing credit accounts.

Lenders want to see you have experience with credit over time – not just a short history with a few new accounts. Your history length factors in:

- How long your accounts have been open

- The age of your oldest account

- How long it’s been since you used certain accounts

To build up your history length:

- Avoid closing your oldest credit card accounts if possible.

- Be cautious about opening a lot of new accounts close together.

- Let your accounts age and build history over time.

4. Credit Mix

The fourth factor, making up 10% of your score, is your mix of credit types – e.g. credit cards, retail accounts, installment loans, mortgage.

Having a diverse mix shows you can handle responsibly managing different types of credit accounts. However, it’s not required to have one of each.

To improve your credit mix:

- No need to open accounts you don’t need just for mix purposes.

- Getting an installment loan or mortgage may add to your mix over time.

5. New Credit

The final factor considered (10%) looks at new credit – accounts you’ve opened recently. Applying for several new accounts in a short period can indicate higher risk, especially if you don’t have a long established credit history already.

Opening new accounts also causes hard inquiries on your credit reports when lenders check your credit. Too many hard inquiries in a short timeframe can negatively impact your score.

To minimize score damage from new credit:

- Avoid applying for too many new accounts close together.

- Shop for a mortgage, auto loan or student loan within a focused timeframe.

While these five factors form the foundation of FICO credit scores, their importance may vary based on your individual credit profile. The key is to maintain a long history of responsible credit use over time. Monitor your credit reports and FICO scores so you understand how potential changes impact your credit health.

The better you understand what goes into your score, the easier it is to build and maintain excellent credit.

Your payment history (35 percent)

You probably already know that paying your bill on time each month is a good credit card habit to build. But did you know that if you miss a bill payment it could lead to a drop in your score?

If you miss your due date by only a day or two, the damage will likely be minimal, although you may be charged a late fee (many companies wonât report a late payment to a credit bureau until itâs 30 days late). Plus, when deciding how missed payments will affect your score, FICO considers other factors such as how late you were, how much was owed, how recently you missed the deadline and how many times youâve been late in the past.

If youâre so late with a payment that it goes to collections, expect an even bigger ding to your score. Because youâre not always notified when this happens, its a good idea to regularly check your credit report, which you can do by requesting a free copy from each of the three major credit bureaus (Equifax, Experian and TransUnion).

Length of your credit history (15 percent)

Your credit history factors in the length of your oldest credit account, your newest credit account and the average age of all your accounts combined so lenders know how long youâve been responsibly managing your credit. In most cases, the longer your credit history, the higher your score. So if youâre thinking of canceling a card youâve had for a long time, you may want to think twice.

What Five Factors Determine My FICO® Score? | Experian Credit 101 Express

FAQ

What are the 5 factors that determine your credit score?

The five key factors that determine a credit score are payment history, amounts owed, length of credit history, new credit, and credit mix.

What are the 5 components of the FICO Score?

- Payment History. Weight: 35% …

- Amounts You Owe. Weight: 30% …

- Length of Your Credit History. Weight: 15% …

- New Credit You Apply For. Weight: 10% …

- Types of Credit You Use. Weight: 10%

What are the 5 C’s of credit score?

Character, capacity, capital, collateral and conditions are the 5 C’s of credit. When applying for credit, lenders may look at them to determine your creditworthiness. And understanding them can help you boost your creditworthiness before applying.

What are the factors in determining a FICO Score?

The main categories considered are a person’s payment history (35%), amounts owed (30%), length of credit history (15%), new credit accounts (10%), and types of credit used (10%). FICO scores are available from each of the three major credit bureaus, based on information contained in consumers’ credit reports.

How are FICO scores calculated?

FICO Scores are calculated using many different pieces of credit data in your credit report. This data is grouped into five categories: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and credit mix (10%). Your FICO Scores consider both positive and negative information in your credit report.

What factors affect a credit score?

Though there are multiple credit scoring models, FICO Scores are used by 90% of lenders. FICO Scores are calculated based on five factors: payment history, credit utilization, length of credit history, credit mix and new credit. What affects your credit scores? Credit scoring companies calculate your credit score based on multiple factors.

Do lenders rely on a FICO score?

While there are other credit scores out there, most lenders rely on FICO, and even if they don’t, the scoring models will use similar factors. Keeping tabs on your FICO score should give you a good gauge on your credit worthiness in general. Keep in mind that your FICO score is calculated only from the information in your credit report.

How many different FICO scores are there?

According to myFICO.com, the consumer division of FICO, there are at least 10 different FICO scores used for varying purposes. The VantageScore, which was created by the three credit bureaus, is another common credit score. Many free credit score services offer the VantageScore 3.0.

Does your credit mix affect your FICO score?

The credit mix usually won’t be a key factor in determining your FICO scores—but it will be more important if your credit report does not have a lot of other information on which to base a score. While there are other credit scores out there, most lenders rely on FICO, and even if they don’t, the scoring models will use similar factors.

What is a credit score based on?

Your credit score is based on the information lenders and other financial institutions report to credit bureaus. Though there are multiple credit scoring models, FICO Scores are used by 90% of lenders. FICO Scores are calculated based on five factors: payment history, credit utilization, length of credit history, credit mix and new credit.