A Roth individual retirement account (Roth IRA) gives you a chance to grow your money over time by investing already-taxed dollars in a range of different securities. In retirement, your qualified withdrawals are tax-free—provided you satisfy a few basic rules. 1 Although Roth IRAs can offer a powerful and flexible way to save and invest for retirement, not everyone can contribute to one. Heres what you need to know about contribution requirements for this type of retirement account.

The Basics of Roth IRA Eligibility in 2025

Have you ever wondered if you qualify for a Roth IRA? Maybe you’ve heard about the amazing tax benefits these retirement accounts offer but aren’t sure if you can take advantage of them. Well, I’ve got good news – Roth IRAs are more accessible than many people think!

As someone who’s navigated the confusing world of retirement planning for years, I can tell you that understanding who can contribute to a Roth IRA is actually pretty straightforward once you break it down. Let’s dive into everything you need to know about Roth IRA eligibility in 2025.

What Exactly Is a Roth IRA?

Before we get into who can contribute, let’s make sure we’re on the same page about what a Roth IRA actually is

A Roth IRA is a special type of Individual Retirement Account that offers unique tax advantages. According to the IRS, a Roth IRA follows many of the same rules as traditional IRAs, but with some important differences:

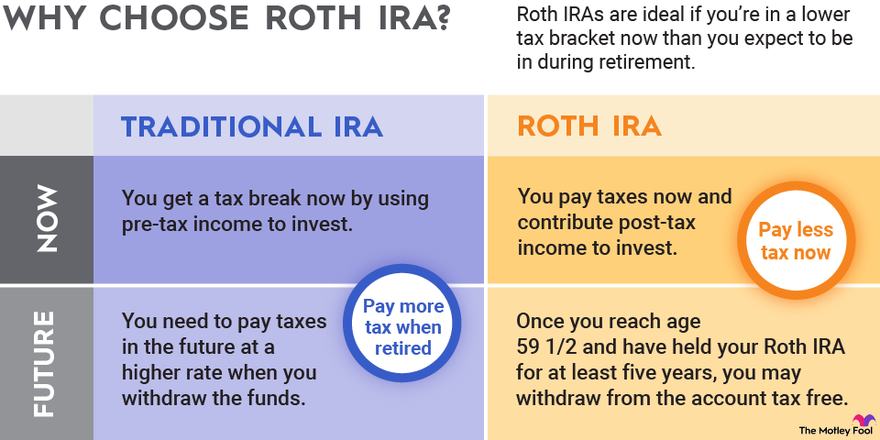

- Tax treatment: You can’t deduct contributions to a Roth IRA (unlike traditional IRAs), but qualified distributions are completely tax-free

- Age flexibility: You can make contributions after age 70½ (no age limits!)

- Lifetime access: You can leave amounts in your Roth IRA as long as you live (no required minimum distributions)

Who Can Contribute to a Roth IRA in 2025?

The simple answer: Anyone with earned income that falls within certain income limits can contribute to a Roth IRA.

But what does that actually mean? Let’s break it down.

1. You Must Have Earned Income

Before you can put money into a Roth IRA, you need to be making money. According to Fidelity, earned income includes:

- Wages, salaries, and tips (typically reported on a W-2)

- Commissions and self-employment income

- Certain military income streams (like nontaxable combat pay)

- Disability benefits received before retirement age

What doesn’t count as earned income? Things like:

- Investment earnings (interest, dividends, capital gains)

- Rental income

- Pension or annuity income

- Social Security benefits

- Unemployment compensation

One important rule: You cannot contribute more to a Roth IRA than you’ve earned in that year. So if you only earned $5,000 in 2025, that’s your maximum contribution limit (even though the standard limit is higher).

2. Your Income Must Fall Within IRS Limits

This is where things get a bit more complicated. Based on your Modified Adjusted Gross Income (MAGI) and how you file your taxes, the IRS decides how much you can put into a Roth IRA.

For 2025, here are the Roth IRA income limits:

| Filing Status | MAGI | Contribution Limit |

|---|---|---|

| Single | < $150,000 | Full contribution ($7,000; $8,000 if 50+) |

| Single | ≥ $150,000 but < $165,000 | Partial contribution |

| Single | ≥ $165,000 | Not eligible |

| Married filing jointly | < $236,000 | Full contribution ($7,000; $8,000 if 50+) |

| Married filing jointly | ≥ $236,000 but < $246,000 | Partial contribution |

| Married filing jointly | ≥ $246,000 | Not eligible |

| Married filing separately | < $10,000 | Partial contribution |

| Married filing separately | ≥ $10,000 | Not eligible |

Let me explain what “partial contribution” means. If your income is in this range, you’ll need to figure out how much less you can contribute. You can’t give as much as you would like because you are getting closer to the upper limit.

Common Questions About Roth IRA Eligibility

Is There an Age Limit for Roth IRAs?

Nope! Unlike traditional IRAs, there’s absolutely no age limit for contributing to a Roth IRA. In fact, as Fidelity points out, even children under 18 can have Roth IRAs as long as they have earned income (think: babysitting, lawn mowing, or part-time jobs).

This is actually a super smart strategy for parents or grandparents who want to give kids a head start on retirement savings. The power of compound interest over 50+ years is absolutely mind-blowing!

What if I Don’t Have Income But My Spouse Does?

Great question! If you’re married filing jointly, you might qualify for what’s called a “spousal IRA.”

Here’s how it works: If one spouse has earned income and the other doesn’t, the earning spouse can contribute to an IRA for the non-working spouse, as long as:

- You file a joint tax return

- The working spouse earns enough to cover both contributions

- You stay within the income limits for married filing jointly

This is super helpful for stay-at-home parents or anyone temporarily out of the workforce.

Can I Contribute to a Roth IRA if I Have a 401(k)?

Absolutely! Having a workplace retirement plan like a 401(k) doesn’t affect your eligibility for a Roth IRA at all. Many financial advisors actually recommend contributing to both if you can afford it.

The only thing that matters is whether your income falls within the IRS limits. So feel free to max out both your 401(k) and your Roth IRA if possible!

What if I Make Too Much Money for a Roth IRA?

If your income exceeds the Roth IRA limits, don’t worry – you’ve still got options:

Option 1: Backdoor Roth IRA

This is a popular workaround for high-income earners. It involves:

- Contributing to a traditional IRA (which has no income limits for contributions, though deductibility may be limited)

- Converting those funds to a Roth IRA

There’s some paperwork involved, and you’ll need to be careful about the “pro-rata rule” if you have existing traditional IRA balances, but it’s a legitimate strategy many people use.

Option 2: Roth 401(k)

If your employer offers a Roth 401(k) option, there are no income limits for these accounts! You can contribute regardless of how much you earn.

Option 3: Traditional IRA

While not the same as a Roth, a traditional IRA is still a tax-advantaged retirement account. Just be aware that the tax benefits work differently (tax deduction now, taxed withdrawals later), and income limits may affect whether your contributions are deductible.

How Much Can I Contribute to a Roth IRA?

Assuming your income qualifies, here are the contribution limits for 2025:

- Under age 50: $7,000 per year

- Age 50 and older: $8,000 per year (includes $1,000 “catch-up” contribution)

Don’t forget that these limits apply to ALL of your IRA contributions, whether they are traditional or Roth. If you put $3,500 into a traditional IRA, you can only put the same amount into a Roth IRA if you are younger than 50.

When’s the Deadline for Making Roth IRA Contributions?

You have until the tax filing deadline to make Roth IRA contributions for the previous year. For most people, that’s April 15th of the following year.

So for 2025 contributions, you have until April 15, 2026, to contribute. This gives you some flexibility in timing your contributions.

Why Should I Consider a Roth IRA?

I’m a huge fan of Roth IRAs for several reasons:

- Tax-free growth: Your money grows completely tax-free

- Tax-free withdrawals: As long as you follow the rules, you won’t pay taxes on qualified distributions

- No RMDs: Unlike traditional IRAs, Roth IRAs don’t have required minimum distributions during your lifetime

- Flexibility: You can withdraw your contributions (not earnings) at any time without penalties

- Estate planning benefits: Roth IRAs can be great wealth transfer vehicles for your heirs

My Personal Take on Roth IRAs

I’ve been contributing to my Roth IRA for over a decade now, and it’s honestly one of the best financial decisions I’ve ever made. The peace of mind knowing I’ll have tax-free income in retirement is invaluable.

For young professionals especially, I think Roth IRAs are a no-brainer if you qualify. You’re likely in a lower tax bracket now than you will be later in your career, so paying taxes now makes a lot of sense.

How to Open a Roth IRA

If you’ve determined you’re eligible to contribute to a Roth IRA, opening one is super easy! Most major brokerages and financial institutions offer them. You’ll need:

- Your Social Security number

- Bank account info for transfers

- Basic personal information

- An initial contribution (though some places will let you open with $0)

The whole process usually takes less than 15 minutes online.

Final Thoughts

Understanding who can contribute to a Roth IRA doesn’t have to be complicated. The key factors are:

- Having earned income

- Being within the income limits

- Staying under the annual contribution caps

If you check those boxes, congratulations – you can take advantage of one of the most powerful retirement savings tools available!

Remember that eligibility can change from year to year as your income changes or the IRS adjusts its limits. It’s worth checking each year to see if you qualify.

Have you started contributing to a Roth IRA yet? If not, and you’re eligible, what are you waiting for? Your future self will thank you!

This article has been updated with the latest information for 2025 from the IRS and Fidelity.

Is there an age limit to contribute to a Roth IRA?

Provided you have earned income, theres no age limit to contribute to a Roth IRA. This means that even those under 18 can contribute to Roth IRAs. In fact, parents can open a Roth IRA for kids to help their children invest for the future. Contributions are subject to the earned income requirement even for those that are 18 or younger.

When do you have to contribute to a Roth IRA by?

The latest you can contribute to a Roth IRA if youre eligible is your unextended tax filing deadline, which for most people is Tax Day in April. This can help because you might not really know your MAGI until you start filing your taxes.

If you become ineligible after youve already made Roth IRA contributions for the year, you have until the extended filing deadline (normally October 15 the year your taxes are due) to correct the mistake. Depending on the investment income youve earned, you may owe taxes or a penalty. Find out your options if you contributed too much to your IRA.