No matter what stage of life youre in, one thing will always remain the same: Its never too late — or too early — to save money.

Are you approaching your late 30s and wondering if your financial house is in order? Maybe you’re looking at your bank account retirement savings and overall financial picture and thinking, “Am I where I should be at this point in my life?”

You’re not alone. At 38, many of us are juggling career advancement, possibly raising children, perhaps paying a mortgage, and hopefully building wealth for the future. But with so many competing priorities, it can be hard to know if you’re on track.

This article will break down the important financial goals you should have by age 38, give you tips on how to get caught up if you’re behind, and give you a realistic way to look at your own financial situation.

The Financial Benchmarks for Your Late 30s

Retirement Savings: The 3X Rule

Most financial experts say that by age 38, you should have saved three times your annual salary for retirement. This benchmark comes up consistently across multiple financial resources.

Take the example of someone who makes $60,000 a year: they should have around $180,000 saved in 401(k), IRAs, and other retirement-specific accounts.

But don’t panic if you’re not there yet! According to Federal Reserve data, the median retirement account balance for Americans in the 35-44 age group is about $60,000-$67,000, with some sources citing averages as high as $131,950. This shows there’s a wide range of “normal” when it comes to retirement savings.

Emergency Fund: Your Financial Safety Net

By age 38, you should have enough money saved in an emergency fund to cover three to six months of living costs. If you lose your job, have a medical emergency, or need to make major repairs to your home, this safety net will protect you.

If your income is stable or you’re in a dual-income household, three months might be sufficient. If your income fluctuates or you’re the sole earner, aim for six months of expenses.

Debt Management

At 38, you should be focused on eliminating what financial planners call “bad debt” – high-interest obligations like credit card balances and personal loans with interest rates above 7%.

“Good debt” with interest rates below 7% (like mortgages and some student loans) is acceptable to maintain as long as the payments fit comfortably within your budget while still allowing you to save.

Net Worth Goals

Your net worth (assets minus liabilities) at 38 should ideally be around five times your annual income. Some financial experts suggest a more conservative target of two times your annual salary by age 40, which would mean you should be approaching that benchmark at 38.

According to various sources, the average net worth for Americans aged 35-44 ranges from $52,000 to $67,270, though this varies widely based on income level and geographic location.

Beyond the Basic Numbers: A Holistic Financial Picture

Insurance Coverage

By 38, you should have comprehensive insurance coverage, including:

- Health insurance

- Disability insurance (often overlooked but crucial)

- Property and casualty insurance

- Life insurance (especially if you have dependents)

Disability insurance deserves special attention. As a certified financial planner from SoFi notes, “Your ability to earn income for the next several decades is your most valuable asset. Protect it accordingly.”

Estate Planning Basics

If you have children or significant assets, by 38 you should have at least basic estate planning documents in place:

- A will (especially important for naming guardians for minor children)

- Power of attorney

- Healthcare directives

Investment Diversification

Your investment portfolio should be increasingly diversified by age 38. Beyond your retirement accounts, consider investing in:

- Index funds

- Real estate

- Other asset classes that match your risk tolerance and goals

What If You’re Behind? Catching Up Strategies

If the benchmarks above seem daunting, don’t worry! Here are some effective strategies for catching up:

1. Increase Your Savings Rate

The single most effective way to accelerate your financial progress is to increase how much you save. Try to save at least 15-20% of your income toward retirement and other financial goals.

2. Maximize Retirement Account Contributions

Take full advantage of tax-advantaged accounts:

- Contribute at least enough to your 401(k) to get your employer match

- Consider maxing out your IRA contributions

- If you’re eligible, explore catch-up contributions

3. Prioritize High-Interest Debt

Focus on eliminating high-interest debt first to free up more money for savings and investments.

4. Consider Side Hustles

A temporary side hustle can give your savings a significant boost. Even an extra $500 per month can add up to $6,000 per year toward your financial goals.

5. Reassess Your Housing Costs

Housing typically consumes the largest portion of most budgets. Ensure your rent or mortgage payment doesn’t prevent you from meeting your financial goals. Financial experts recommend spending no more than 28-30% of your gross income on housing.

The Reality Check: Everyone’s Path Is Different

Here’s an important truth: these benchmarks are general guidelines, not absolute rules. Your financial journey is uniquely yours, influenced by:

- Your career path and income trajectory

- Whether you had student loans

- Your geographical location and cost of living

- Family situations (children, elder care responsibilities)

- Health considerations

- Personal financial priorities

As Brian Walsh, a certified financial planner, wisely notes: “Everyone starts with different levels of debt, works in different industries, and lives in different locations… I am much more concerned about their finances now and over the next 30 years than what they did in their 20s.”

Is 38 Too Late to Get Started?

Absolutely not! While starting early gives you more time to benefit from compound interest, 38 is still young in the grand scheme of things.

If you’re just beginning your serious financial journey at 38, you still have potentially 25-30 years until traditional retirement age. That’s plenty of time to build significant wealth with disciplined saving and investing.

The key is to start NOW. Every day you delay means missing out on the power of compound growth.

Creating Your Personal Financial Roadmap at 38

Rather than comparing yourself to arbitrary benchmarks, use your current age as motivation to create a personalized financial plan:

-

Take stock of where you are right now – Calculate your net worth, review your retirement savings, and assess your debt situation.

-

Define your financial goals – When do you want to retire? What lifestyle do you envision? Do you have other major financial goals?

-

Create a realistic plan – Based on your current situation and goals, determine how much you need to save and invest.

-

Implement and monitor – Put your plan into action and check in regularly to track progress and make adjustments.

-

Seek professional guidance – Consider working with a financial advisor to create a tailored strategy.

Regular Financial Checkups

At 38, establish the habit of regular financial reviews. Schedule time every 3-6 months to:

- Review your budget and spending

- Check progress toward savings goals

- Rebalance investments as needed

- Reassess insurance needs

- Update financial documents

The Bottom Line: Focus on Progress, Not Perfection

I believe the most important financial milestone at 38 isn’t reaching a specific dollar amount—it’s establishing positive financial habits and momentum toward your personal goals.

Rather than getting discouraged by comparing yourself to arbitrary benchmarks, focus on continuously improving your financial situation. Small, consistent actions over time lead to significant results.

Remember that financial success isn’t a competition or a race—it’s about creating security and opportunities for yourself and your loved ones. Wherever you are in your financial journey at 38, the best time to take the next step forward is today.

What’s your take?

Where are you on your financial journey at 38 (or whatever age you are now)? Have you found certain strategies particularly helpful for building wealth? I’d love to hear your thoughts and experiences in the comments below!

Disclaimer: This article provides general financial information and is not intended as personalized financial advice. Everyone’s situation is unique, and you should consult with a qualified financial professional before making significant financial decisions.

Average savings by age

The average American has $62,410 in savings, according to the Federal Reserve Board’s 2022 Survey of Consumer Finances, the latest available data. When you break that down by age group, it looks like this:

|

Age group |

Average savings |

|---|---|

|

Under 35 |

$20,540 |

|

35-44 |

$41,540 |

|

45-54 |

$71,130 |

|

55-64 |

$72,520 |

|

65-74 |

$100,250 |

|

75+ |

$82,800 |

Calculate how long it will take to hit your savings goals with Ally Bank’s savings calculator:

Compounded savings by age 65 based on the age you started:

|

Starting age |

5% annual retirement savings rate |

10% annual retirement savings rate |

15% annual retirement savings rate |

|---|---|---|---|

|

25 |

$575,714 |

$1,153,286 |

$1,730,857 |

|

35 |

$294,096 |

$589,141 |

$884,187 |

|

45 |

$136,842 |

$274,126 |

$411,410 |

Dedicating 5% to 15% of your pre-tax income to retirement isnt always possible. You may be starting a new career, paying back student loans, or have other financial obligations and arent able to save that much of your salary all at once. Start with a percentage youre comfortable with and increase your savings rate gradually by 1% each year until you reach the 15% mark.

If youre currently paying back loans or other debts, aim to save for retirement while paying off debt simultaneously, putting away what you can while sticking to your loan repayment schedule.

40 Years Old and Nothing Saved For Retirement – Top 10 Recommendations

FAQ

How much money should a 38 year old have in savings?

How much should you save for retirement? By the time you’re 30, you should have saved enough to cover your yearly salary. For example, if you’re earning $50,000, you should have $50,000 banked for retirement. By age 40, you should have three times your annual salary saved.

How much super should I have at 38?

| Age | Male | Female |

|---|---|---|

| 25–29 | $25,407 | $23,273 |

| 30–34 | $53,154 | $44,053 |

| 35–39 | $90,822 | $71,686 |

| 40–44 | $131,792 | $102,227 |

At what age should you have $100,000 saved?

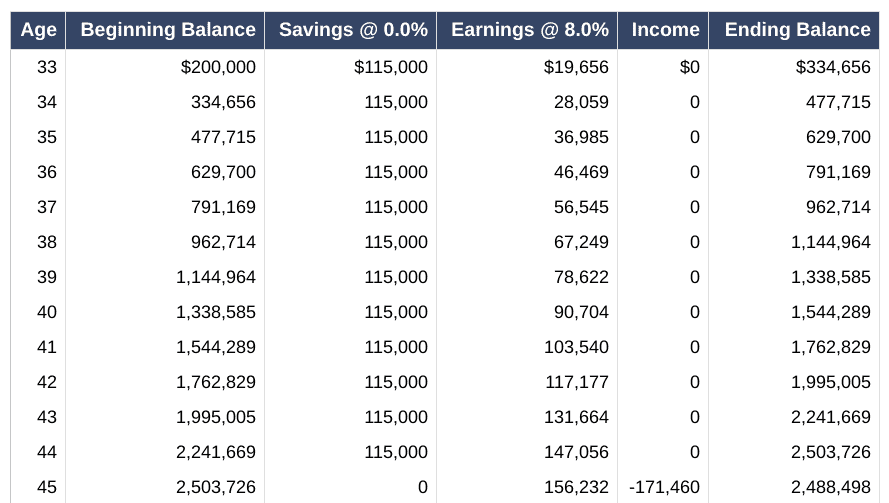

Kevin O’Leary says that by age 33, you should have saved $100,000 “somewhere.” He says, “That’s the Age When It’s Really Time to Start Getting Focused.”

What is the $1000 a month rule for retirement?

Key Takeaways. The $1,000-a-month rule says you’ll need $240,000 in savings for every $1,000 monthly retirement income you want. This rule uses a 5% annual withdrawal rate and assumes your savings stay invested to grow with inflation.