Finally, after years of diligently putting money into your 401(k), the big day has arrived: retirement! But now comes the tricky part: figuring out how to turn all that saved money into real income without running out too soon or paying too much in taxes.

I’ve helped many clients navigate this transition, and let me tell you, it’s not as simple as just cashing out your account. There are withdrawal strategies that can make your retirement savings last longer and minimize your tax burden.

Understanding Your 401(k) Withdrawal Options

When you retire, you’ve got several choices for what to do with your 401(k) money:

- Leave it where it is – Keep your money in your employer’s 401(k) plan

- Set up periodic withdrawals – Create a regular payment schedule

- Take a lump sum distribution – Cash out the entire balance at once

- Roll it over to an IRA – Transfer to a potentially more flexible account

- Convert to a Roth IRA – Pay taxes now for tax-free withdrawals later

- Purchase an annuity – Exchange your balance for guaranteed income

Each option has its own advantages and potential pitfalls, which we’ll explore below.

Key Rules You Need to Know First

Before diving into strategies, you should understand some important 401(k) rules that affect your withdrawals

Age-Related Withdrawal Rules

- Before 59½: Withdrawals typically incur a 10% early withdrawal penalty plus income taxes

- Rule of 55: If you retire or are laid off in the year you turn 55 or later, you can withdraw from your 401(k) without the 10% penalty (but still pay income taxes)

- 59½ to 73: You can withdraw without penalties, but aren’t required to yet

- Age 73+: Required Minimum Distributions (RMDs) begin for traditional 401(k)s

Tax Considerations

- Traditional 401(k): Withdrawals are taxed as ordinary income

- Roth 401(k): Qualified withdrawals are tax-free (starting in 2024, no RMDs required)

Top Withdrawal Strategies for Your 401(k)

Now, let’s look at the most effective strategies for withdrawing money from your 401(k) after retirement:

1. The 4% Rule Approach

This tried-and-true retirement withdrawal strategy calls for taking out 4% of your retirement savings in your first year of retirement and then adjusting that amount annually for inflation (usually by adding about 2% each year).

Example: If you have $1 million saved, you’d withdraw $40,000 in your first retirement year. In year two, you’d take $40,800 (original amount plus 2%), and so on.

Pros:

- Simple to follow

- Provides predictable annual income

- Designed to make your money last approximately 30 years

Cons:

- Doesn’t account well for market volatility

- May not work as well in low-return environments

- Could deplete savings early if you retire during a market downturn

2. Fixed-Dollar Withdrawals

With this method, you regularly take out a set amount of money, like $3,000 a month or $36,000 a year.

Pros:

- Predictable income makes budgeting easier

- Automatic withdrawals can include tax withholding

- Simple to implement and understand

Cons:

- Doesn’t adjust for inflation automatically

- May require selling more investments during market downturns

- Could deplete your principal faster than anticipated

3. Fixed-Percentage Withdrawals

Instead of a fixed dollar amount, you withdraw a set percentage of your portfolio annually. The dollar amount fluctuates based on your portfolio’s current value.

Example: With a $1 million portfolio and a 4% withdrawal rate, you’d take $40,000 the first year. If your portfolio then grows to $1.1 million, your next withdrawal would be $44,000.

Pros:

- Automatically adjusts to market conditions

- Can potentially increase withdrawals over time

- Reduces risk of depleting savings too quickly

Cons:

- Unpredictable income makes budgeting harder

- May lead to significant income fluctuations

- Could result in too little income during market downturns

4. Systematic Withdrawal Plan

With this strategy, you only withdraw the income generated by your investments (dividends, interest) while preserving your principal.

Pros:

- Preserves your principal

- Offers potential for continued growth

- Theoretically allows your savings to last indefinitely

Cons:

- Income varies based on market performance

- May not provide enough income to meet needs

- Might not keep pace with inflation

5. The “Buckets” Strategy

This approach divides your retirement savings into three separate accounts or “buckets”:

- Bucket 1: Cash for immediate expenses (3-5 years of living expenses)

- Bucket 2: Fixed income securities for medium-term needs

- Bucket 3: Equities for long-term growth

As you deplete Bucket 1, you replenish it with earnings from Buckets 2 and 3.

Pros:

- Provides psychological comfort during market volatility

- Allows longer-term investments time to grow

- Helps manage sequence-of-returns risk

Cons:

- More complex to manage

- Requires regular rebalancing

- May keep too much in cash, limiting growth potential

6. RMD-Based Withdrawals

Once you reach age 73, you’re required to take minimum distributions from traditional 401(k)s. Some retirees simply use these RMDs as their withdrawal strategy.

How it works: The IRS has tables that tell you how much you need to take out based on your account balance and how long you expect to live.

Pros:

- Ensures compliance with tax laws

- Generally conservative in early retirement years

- Adjusts automatically as you age

Cons:

- May not provide enough income in early retirement

- Could force larger withdrawals than needed in later years

- Doesn’t account for your actual income needs

Tax-Smart Withdrawal Strategies

One of the biggest mistakes I see retirees make is not considering the tax implications of their withdrawals. Here are some tax-efficient approaches:

Withdraw in Low-Income Years

Between ages 59½ and 73, you can strategically withdraw only enough to keep yourself in a lower tax bracket.

Example: In 2023, a married couple filing jointly could withdraw enough to stay within the 12% tax bracket (below $89,450 in taxable income).

Incorporate Charitable Giving

If you’re charitably inclined and age 70½ or older, you can make qualified charitable distributions (QCDs) directly from your IRA to eligible charities – up to $100,000 annually ($200,000 for couples).

This satisfies your RMD requirement without increasing your taxable income!

Strategic Roth Conversions

During years when your income is lower (especially early in retirement), consider converting portions of your traditional 401(k) to a Roth IRA. You’ll pay taxes now but enjoy tax-free withdrawals later.

What About Your 401(k) Plan Fees?

Don’t forget about fees! If your 401(k) plan charges high fees, it might make sense to roll your money into an IRA, which often has:

- Lower administrative fees

- More investment options

- Greater withdrawal flexibility

However, if you need to access your money between ages 55-59½, keeping it in your 401(k) allows you to use the Rule of 55 for penalty-free withdrawals.

A Sample Withdrawal Strategy

Here’s what a comprehensive withdrawal strategy might look like for someone retiring at 65 with $1 million in retirement accounts:

- Ages 65-70: Withdraw living expenses from taxable accounts first, staying within lower tax brackets

- Age 70½+: Implement QCDs for charitable intentions

- Ages 65-73: Perform strategic Roth conversions in low-income years

- Age 73+: Take RMDs as required, withdrawing from traditional accounts first

- Throughout retirement: Maintain 2-3 years of expenses in cash/short-term investments to avoid selling in down markets

Common Mistakes to Avoid

In my years helping retirees, I’ve seen these mistakes repeated often:

- Withdrawing too much too soon – The first years of retirement are crucial for long-term success

- Not accounting for inflation – What costs $50,000 today might cost $67,000 in 10 years

- Ignoring tax planning – Smart withdrawal sequencing can save thousands in taxes

- Keeping too much in cash – Inflation will erode your purchasing power

- Not adjusting your strategy – Life changes, markets fluctuate – your plan should adapt

Final Thoughts

There’s no one-size-fits-all “best” way to withdraw from your 401(k) after retirement. The optimal approach depends on your:

- Total retirement savings

- Other income sources (Social Security, pensions)

- Health and life expectancy

- Tax situation

- Legacy goals

- Risk tolerance

For most retirees, a combination of these strategies works better than relying on just one method. And don’t be afraid to adjust your approach as circumstances change.

While managing your own withdrawals is certainly doable, this is also an area where a good financial advisor can potentially add significant value – helping you optimize your withdrawal strategy, minimize taxes, and ensure your money lasts as long as you need it.

What withdrawal strategy are you considering for your retirement? Have questions about making your 401(k) last? Drop a comment below, and I’ll try to help!

Finding the right withdrawal strategy

A key question that many retirees ask is How long will my money last in my retirement?

Fidelity recommends taking out no more than 4% to 5% of your savings in the first year of retirement as a starting point. Then, you should increase that amount every year by the rate of inflation.

There are several approaches you can take to determine which account you should withdraw the money from. The traditional approach is to withdraw first from taxable accounts, then tax-deferred accounts, and finally Roth accounts where withdrawals are tax free. The goal is to allow tax-deferred and Roth assets the opportunity to grow over more time.

For most people with multiple retirement savings accounts with differing tax-treatments, a better approach might be proportional withdrawals. When an investor sets a goal amount, they take money out of each account based on how much of their overall savings is in that account. This means that your tax bill will be more stable in retirement, and you may pay less in taxes over your lifetime and make more after taxes. To get started, consider these simple strategies that can help you get more out of your retirement savings, depending on your situation.

Ways to withdraw money in retirement

If youre retired that probably means no more regular paycheck, and you may need to turn to your investments for income. However, the impact of taxes is just as important to consider now as it was when saving for retirement.

The good news is that in retirement there may be more options to increase after-tax income, especially when savings span multiple account types, such as traditional retirement accounts, Roth accounts, and taxable accounts. The downside is that choosing which accounts to draw from and when can be a complicated decision.

“Many people are seeking ways to help reduce the taxes that they will pay over the course of their retirement,” says Andrew Bachman, CFA®, CFP®, director of financial solutions at Fidelity Investments. “Timing is critical, so how and when you choose to withdraw from various accounts—workplace savings plans, IRAs accounts, and brokerage or savings accounts—can impact your taxes in different ways.”

What to do with your 401k When you Retire ? | On The Money

FAQ

Is it better to withdraw monthly or annually from a 401k?

Well the answer is obvious, leaving the most money invested is optimal. That’s why monthly is better than yearly, given those 2 choices. But if you want to go shorter, that’s fine too. It will just be harder to keep track of because you’ll have to make withdrawals more often.

At what age is 401k withdrawal tax-free?

Withdrawals from a 401(k) aren’t always tax-free at a certain age. Withdrawals from a Roth 401(k) are tax-free when you are 59½ and have had the account for at least five years.

What is the best order to withdraw retirement funds?

What’s the order in which I should tap into my retirement accounts? In this case, the conventional wisdom goes that you should withdraw from your taxable accounts first, then tax-deferred, then tax-free.

What is the most tax efficient way to withdraw from a 401k?

Finding the right withdrawal strategy The traditional approach is to withdraw first from taxable accounts, then tax-deferred accounts, and finally Roth accounts where withdrawals are tax free. The goal is to allow tax-deferred and Roth assets the opportunity to grow over more time.

How do I withdraw money from my retirement account?

Consider these retirement account withdrawal strategies: Take required minimum distributions to avoid penalties. Withdraw funds in years when you are in a low tax bracket. Convert to a Roth. Incorporate charitable giving from your IRA.

How do I withdraw money from my 401(k)?

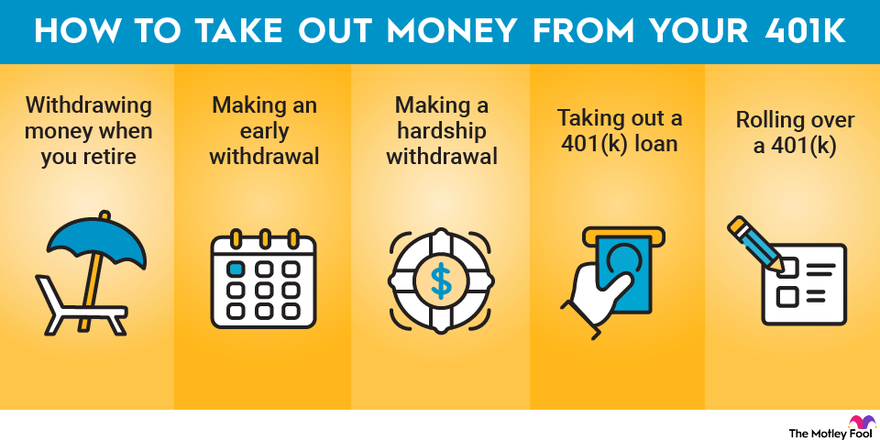

There are a few different ways to take money out of your 401(k), each with its own pros and cons. Here are the best ways to use each one. 1. Withdrawal While Still Working: If you’re still working, your plan may let you make withdrawals while you’re still working (usually after age 59½). These are rare and subject to your employer’s plan rules. Pros: Cons:

Do I need to take money out of a 401(k)?

You may need to take money out of a 401 (k). Here’s what you need to know. Withdrawals from a 401 (k) after age 59 1/2 are penalty-free. Early withdrawals face a 10% penalty unless exceptions like disability or the Rule of 55 apply. You can avoid taxes and penalties if you roll over 401 (k) funds into another 401 (k) or an IRA.

What is a 401(k) withdrawal?

A withdrawal permanently removes money from your retirement savings for your immediate use, but you’ll have to pay extra taxes and possible penalties. Let’s look at the pros and cons of different types of 401 (k) loans and withdrawals—as well as alternative paths. 401 (k) withdrawals

Can I take early 401(k) withdrawals?

In other words, you can only take those penalty-free early 401 (k) withdrawals from the plan you were contributing to at the time you left or were let go. The money in other retirement plans must remain in place until you reach age 59½ if you want to avoid the penalty and potential additional tax liabilities. 3.

Do you have to pay back 401(k) withdrawals?

Pros: You’re not required to pay back withdrawals of the 401 (k) assets. Cons: Hardship withdrawals from 401 (k) accounts are generally taxed as ordinary income. Also, a 10% early withdrawal penalty applies on withdrawals before age 59½, unless you meet one of the IRS exceptions. Sign up for Fidelity Viewpoints weekly email for our latest insights.