The current high interest rate environment is putting a strain on many Americans finances. After years of keeping rates near zero to stimulate the economy during the pandemic, the Federal Reserve aggressively increased rates starting in early 2022 to cool stubbornly high inflation. While the Fed has kept rate hikes paused for the last several meetings, the federal funds rate currently stands at its highest level in 23 years.

But now finances have been stretched thin by rising costs of essentials like food, housing and energy, so many people have had no choice but to turn to borrowing products, like credit cards, to help cover their costs. Carrying credit card debt can be crippling to your finances, especially now that the average credit card rate hovers above 21%. After all, the minimum payments alone may not cover much more than the interest charges on your balance, causing the total balance to rise uncontrollably.

In turn, getting out of high-interest credit card debt needs to be a top priority for most people. But how much credit card debt does the average American have now, and what are some potential strategies to help get rid of it?

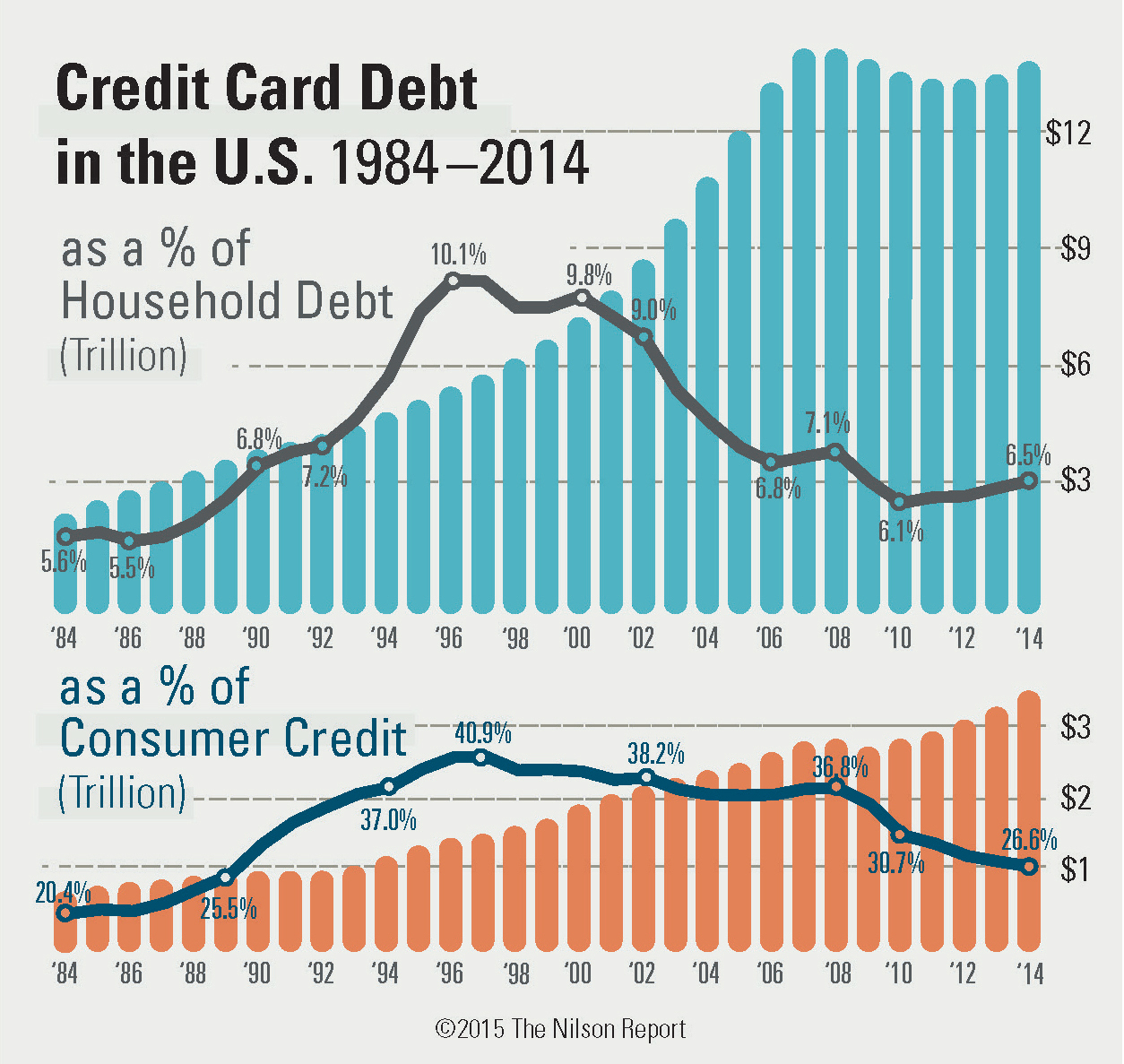

Credit card debt is a growing problem for many American families. With the cost of living rising faster than incomes in recent years, more households have turned to plastic to cover everyday expenses and make ends meet. According to the latest data the average family now owes over $8000 in credit card debt.

How Widespread Is Credit Card Debt?

Credit card debt is very common among U.S. households. Recent surveys found that nearly 80% of families with credit cards carry a balance from month to month. The total revolving debt on credit cards held by American consumers reached $1.08 trillion in February 2023. With over 169 million credit card accounts open nationwide, that works out to around $6,355 in credit card debt per cardholding household.

Breaking Down The Average Balances

While the average credit card debt comes out to $8057 per family balances vary widely across different demographics. In general, older generations tend to carry higher credit card balances than younger households.

- Baby Boomers (ages 57-75): $9,096 average credit card debt

- Gen X (ages 41-56): $8,208

- Millennials (ages 27-40): $5,231

- Gen Z (ages 18-26): $2,381

Credit card debt also differs by income level. Middle class families tend to have the highest average balances.

- Households earning $40k-100k: $8,9134

- Over $100k household income: $7,314

- Under $40k household income: $5,527

What’s Driving High Balances?

Several factors have driven the growth in credit card debt among U.S. families in recent years:

- Stagnant wages – Incomes have not kept pace with the rising cost of living, leading more households to rely on credit cards to pay regular bills.

- Emergency expenses – Surprise home repairs, medical bills, car troubles – when an emergency strikes, many turn to credit cards if they lack savings.

- Reduced access to other borrowing options – Stricter lending criteria have made personal loans harder to qualify for.

- Easier access to credit cards – Banks have increased credit limits and reduced requirements.

- Consumer spending habits – Younger generations tend to spend more impulsively via credit cards.

For many families, credit card debt can quickly snowball out of control due to compounding interest charges. With average card interest rates near 20%, a $5,000 balance can grow to over $8,000 in less than 5 years if only minimum payments are made.

Strategies To Pay Down Credit Card Debt

The best approach to credit card debt depends on your financial situation Here are some top strategies to consider

-

Debt snowball – Focus on paying off your lowest balance cards first, then roll those payments to next highest debts. This gives a psychological boost from quick small wins.

-

Balance transfer card – Transferring high-interest balances to a 0% promotional card stops interest fees temporarily so you can pay down principal faster.

-

Debt consolidation loan – Borrowing a fixed-rate installment loan at lower interest and using it to pay off all cards consolidates debt into one payment.

-

Budgeting and lifestyle changes – Reducing expenses frees up cash flow to accelerate paying off your credit card balances.

-

Debt management plan – This consolidates payments and secures lower interest rates from card issuers. Typically a 36-60 month program.

-

Bankruptcy – This provides legal debt relief by discharging qualifying credit card balances, but damages your credit.

-

Home equity loan – If you have equity available, this lets you borrow at lower rates against your home value to pay off card debt.

The Bottom Line

From medical bills to home repairs to daily necessities, Americans rely on credit cards more than ever. But with interest rates high, credit card debt can quickly become unmanageable. If your family is carrying high revolving balances, make paying them down a top priority for financial health. Implementing the right payoff strategy for your situation can help you finally break free from expensive card debt.

Pay it off with a personal loan

Taking out a personal loan — which has an average rate of about 12% currently — can save a significant amount of money compared to the rate of 21% (or higher) that many credit cards currently charge. And, using a fixed-rate personal loan to pay off credit card balances consolidates multiple payments into one while lowering the interest costs over the life of the loan.

Focus on the debt avalanche or snowball method

With the debt avalanche approach, you pay minimum amounts on all your debts except the one with the highest interest rate, which you attack with any extra funds available. Once that debt is paid off, you “avalanche” all available payments onto the next highest-rate debt, and so on, accelerating your debt payoff.

Similar to the avalanche method, the snowball method also helps keep you on track with paying down your credit cards. The big difference is that you focus on the smallest balances first to score quick wins that can motivate you to keep going. Once the smallest debt is paid, you roll those payments onto the next smallest, and the next, gaining momentum like a snowball rolling downhill.

What Is the Average Credit Card Debt Per Family? – CreditGuide360.com

FAQ

How much does the average family have in credit card debt?

| Debt type | Average balance (2023 ) | Average balance (2024) |

|---|---|---|

| Auto loan | $23,792 | $24,297 |

| Credit card debt | $6,501 | $6,730 |

| Student loan debt | $38,787 | $35,208 |

| Total debt | $104,215 | $105,056 |

How many people have $20,000 in credit card debt?

44% say inflation has “caused them to carry a larger monthly credit card balance.” Of those respondents, 39% have at least $10,000 to $20,000 of credit card debt. That includes 26% of Millennials.

Is $6,000 in credit card debt a lot?

The average American household has over $6,000 in credit card debt, which can be a challenging amount to manage. If you’re just making minimum payments, expect to stay in credit card debt for many years – about 25 years on $6,000, by our calculations.

How much debt is too much for a family?

As a general rule, your total debts (excluding mortgage) should be no more than 10 percent to 15 percent of your take-home pay.