Your credit score is a rating that has been calculated by credit bureaus, to give potential lenders an idea of your creditworthiness.

Your credit score is important if you ever need to take out a loan, mortgage or credit card, as it will impact whether the loan is approved and the kind of interest rate you’ll be offered.

But how does a credit score work, and what is a “good” credit score? Why is a credit score so important, and how can you improve your credit score? In this article, we’ll answer all these questions, as well as more of the most common credit score FAQs.

Your credit score is one of the most important numbers in your financial life This three-digit number essentially represents your creditworthiness and can impact everything from your ability to get approved for loans and credit cards to even rent an apartment or land a new job So what is considered an average or good credit score in Canada? Let’s take an in-depth look.

What is a Credit Score?

A credit score is a numerical representation of your creditworthiness. Credit scoring models analyze your credit history and financial information to generate a score that ranges from 300 to 900.

The higher your score, the lower the risk you pose to lenders. Those with excellent credit scores tend to get approved for credit and qualify for the best rates, while those with poor scores may get denied or have to pay higher interest rates.

There are two main credit bureaus in Canada that calculate credit scores – Equifax and TransUnion While they use similar scoring models, the scores they generate for an individual can differ slightly.

When you apply for credit, lenders will usually check your score with both bureaus. FICO is another company that generates credit scores using data from both Equifax and TransUnion.

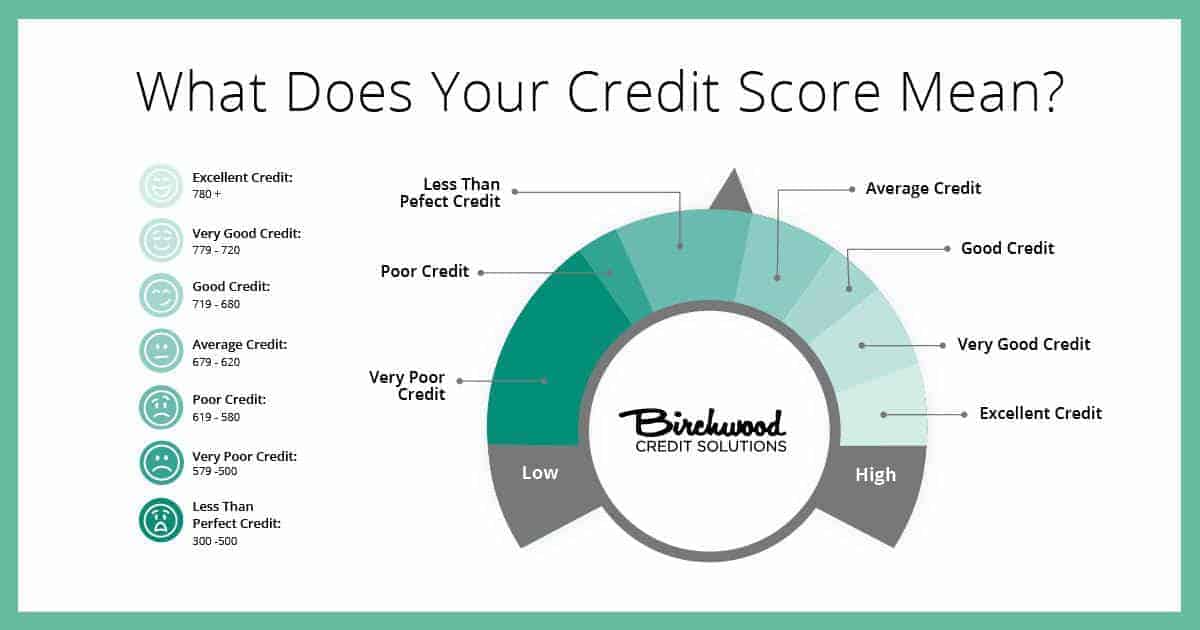

What is Considered a Good or Bad Score in Canada?

Credit scores in Canada range from 300 to 900. Here is how the score ranges generally break down:

- 300 to 574 – Poor – Individuals with scores in this range will have trouble getting approved for credit.

- 575 to 659 – Below Average – Applicants with scores here may get approved but with less than favorable rates and terms.

- 660 to 739 – Good – Scores in this range are considered average or fair. Applicants will likely get approved for credit.

- 740 to 799 – Very Good – Individuals with scores here are seen as having good credit and qualify for competitive rates.

- 800+ – Exceptional – Those with scores of 800 or higher have excellent credit and get the best rates and terms.

So in general, you want your credit score to be above 660 to be considered having good credit. But the higher the better when it comes to qualifying for the most favorable lending offers.

What is the Average Credit Score in Canada?

The average credit score in Canada is around 680 to 700, according to leading credit scoring companies. Here are some reported national averages:

- Equifax – 691

- TransUnion – 673

- FICO – 760

- Borrowell – 672

As you can see, average credit scores from different sources tend to range between 670 to 700.

FICO scores skew higher at 760, but that is because their model gives more weight to your payment history, which tends to be positive for most people.

Just because 680 is an average score doesn’t necessarily mean it’s good. Ideally you want your score to be over 700, and excellent scores are over 760.

Average Credit Score by Age

Your age can impact your credit score quite a bit. Generally, older individuals have higher scores while younger adults tend to have lower scores. Some key factors why this age gap exists:

-

More Credit History – Older consumers simply have longer credit histories established over their lifetime. FICO and other credit scoring models like to see a long track record of responsible use.

-

Higher Incomes – As we get older, our incomes tend to rise. Higher earnings makes it easier to manage debts and avoid missed payments.

-

More Assets – Similarly, older individuals have had more time to build up real estate and other assets. This provides more financial stability.

Here are some average credit scores by age group in Canada:

- 18 to 25 years old: 692

- 26 to 35 years old: 697

- 36 to 45 years old: 710

- 46 to 65 years old: 718

- Over 65 years old: 750

As expected, seniors have the highest average scores while young adults have the lowest.

Average Credit Score by Province

Your province of residence can also impact your credit score average. Here are some reported provincial averages:

- Ontario: 686

- British Columbia: 694

- Alberta: 658

- Quebec: 678

- Atlantic Provinces: Mid to high 600s

In general, individuals in Ontario and British Columbia tend to have the highest average credit scores. Meanwhile, prairie provinces like Alberta tend to score lower.

This provincial variation can be attributed to differences in average incomes as well as economic conditions. For example, Alberta was hit hard by the oil price crash in 2014-15 which led to job losses and missed debt payments.

How to Check Your Credit Score

Checking your credit score regularly is important to monitor your credit health. Here are some options to access your scores:

-

Get your free credit report – You can order your free Equifax and TransUnion credit reports once a year which will include your scores.

-

Sign up for free score access – Equifax and borrowell provide free ongoing access to your Equifax credit score when you sign up for an account.

-

Use a credit monitoring service – For a monthly fee, companies like Borrowell and Credit Karma provide unlimited access to your Equifax and TransUnion scores as well as credit report monitoring.

-

Check with your bank – Many banks like RBC and TD include free credit scores on their online banking sites for customers.

Checking at least annually is recommended. Check more often if you are monitoring your credit or about to apply for a mortgage or other major credit product.

How to Improve Your Credit Score

If your score is lower than you would like, here are some tips to improve it:

- Always pay all your bills on time – payment history is a major factor.

- Keep credit card balances low – high utilization hurts.

- Limit credit inquiries – too many applications in a short time can lower your score.

- Build credit history – the longer your history, the better.

- Don’t close old accounts – keep your oldest cards open.

- Review reports for errors – correct any mistakes that may be dragging down your score.

- Consider credit counseling if needed – they can help get you back on track.

With diligence and patience, you can improve your credit score over time. Maintaining good credit hygiene leads to better scores and access to credit.

The Takeaway

Your credit score is one of the most important factors when applying for loans, mortgages, and credit cards. Scores range from 300 to 900. The average Canadian has a score between 670 to 700. Scores above 760 are considered excellent while scores below 660 still have room for improvement. Regularly check your credit score and work to improve it over time. An excellent credit score will save you money on interest and open doors to great financial opportunities.

How does a credit score work in Canada?

Several aspects of your financial life are included in your credit report and credit score. Banks, credit unions, credit card companies and other financing companies send information to Equifax and TransUnion. This credit score could then be referred to by lenders, car leasing, mobile phone and insurance companies, landlords and even some employers.

On the whole, you do have to give permission to allow a company or landlord to carry out a credit check on you (although in PEI, Nova Scotia and Saskatchewan, they only need to tell you that they’re checking your score).

Several types of behaviour can harm your credit score, including:

- Missing a payment on a loan, mortgage, credit card or mobile phone.

- Owing a large percentage of your available credit (typically, over 30% can have an impact).

- Declaring bankruptcy.

- Having a consumer proposal.

- Having a debt that’s gone to a collection agency.

- Whenever a lender pulls your credit report.

- Fraud alerts on your account.

- Having a short history of borrowing money.

- Having very few or many loans or credit cards.

Declaring bankruptcy or having a consumer proposal will severely affect your credit score and you will probably find it extremely difficult to get a loan or other credit for several years afterwards. Ironically, if you don’t borrow money, you won’t have a credit history and therefore probably won’t have a credit score at all.

Why is a credit score important?

One of the main ironies of your credit score is that the better you manage your credit, the better your score is and the better the interest rates you qualify for are. The worse you manage your credit, the more expensive loans become, making it more difficult to manage your credit.

Your credit score could have an impact on:

- Getting a loan.

- Buying a home.

- Getting a low interest rate on a loan.

- Having more financial options available to you.

- Finding an apartment to rent.

- Getting a job.

If you have a poor credit score, getting a mortgage could be very difficult; you may have to go with a “B lender”, which would charge a higher interest rate than the average. Similarly, securing a loan at a good interest rate could be difficult and you may struggle to sign up for a new credit card.

A low credit score will also make renting a new property more difficult. Landlords want to know that you’re able to pay your rent promptly and are unlikely to become a problem tenant. If you have a low credit score, they’ll be more likely to rent the place out to someone with better credit.

From a financial planning point of view, having a low credit score can limit your borrowing options. Certain types of loans, such as mortgages and home equity lines of credit, can be really useful in helping you to reach your long-term financial goals. A poor or even fair credit score can put these options out of reach, making it far more difficult to reach those financial goals in good time.

Having a poor credit score can also limit your employment opportunities. Some employers insist on pulling your credit score before offering you a job. This is particularly likely if you’re applying for a role in the financial services sector; they will want to see that you are capable of not only managing your own money but also that you’re not in a position where you might be open to bribery.

Federal government employees are also required to have credit checks before their job offer is made. The idea behind this is that if a job candidate has a large amount of debt, they might be more open to committing unethical acts and pose a security risk.

What’s the Average Credit Score in Canada? #creditscore #creditrepair

FAQ

What percentage of people have an 800 credit score in Canada?

People with scores in this range often find it easier to secure loans because they’re seen as low-risk borrowers. In fact, 42% of Canadians have credit scores of 800 and above, which shows that achieving this level of creditworthiness is possible for close to 1 in 2 Canadians.

Does anyone have a 900 credit score in Canada?

While it’s technically possible to have a credit score of 900 in Canada, a 900 is relatively rare and most Canadians will have credit scores that fall within the Fair range.

What is the average credit score in Canada?

In Canada, credit scores range from 300 to 900, 900 being a perfect score and 300 the lowest. According to data from a 2022 survey, the average credit score in Canada is 672, and 694 in British Columbia. Your credit score is used by lenders to determine what kind of borrower you are.

How common is a 700 credit score?

Do Canadians have good credit scores?

In other words, all the financial doors are open to Canadians with excellent credit scores and banks roll out the red carpet to get their business. The median credit score in Canada is 749, which means 50% of the population has excellent credit.

How do I find out my credit score in Canada?

There are two credit bureaus in Canada: Equifax and TransUnion. You can go directly to the bureaus to find out your score, but there may be a cost involved. Alternatively, you can use free services. Sign up with Borrowell to access your Equifax credit score for free.

Is 900 a good credit score in Canada?

While possible, getting a perfect credit score of 900 in Canada is rare. What is a bad credit score in Canada? A bad credit score is one of 559 or lower. A Fair score of 560 to 659 could also be insufficient to apply for credit in many situations.