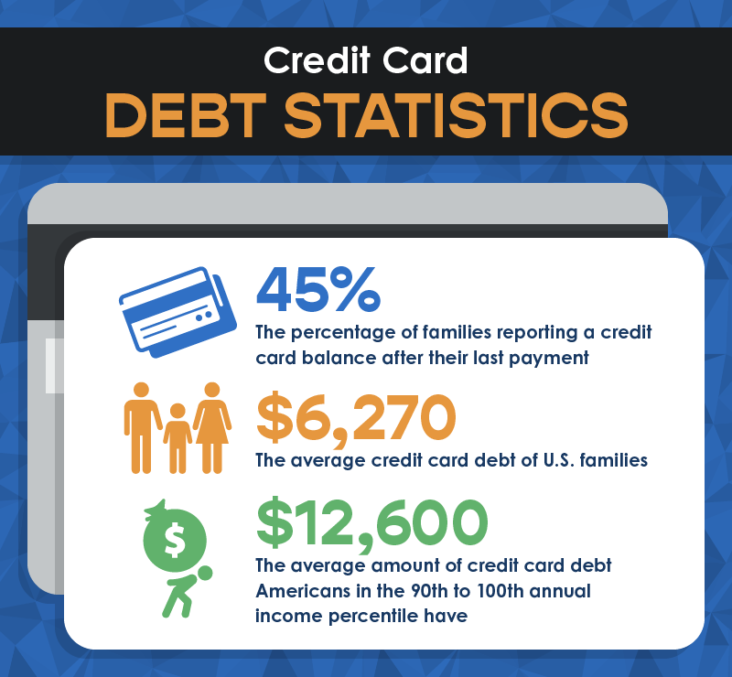

The average credit card balance among U.S. consumers was $6,730 as of Q3 2024, an increase of 3.5% from the third quarter of 2023.

Despite record-high annual percentage rates (APRs) for consumers, credit card debt grew at a slower rate in 2024 than it did in 2023. The total amount of consumer credit card debt in the U.S. grew 8.6% to reach $1.16 trillion as of the third quarter (Q3) of 2024, according to Experian data.

Among those consumers who carry a balanceârevolvers, in industry jargonâthe average balance grew 3.5% to reach $6,730 as of Q3 2024. That increase from 2023 marks the slowest annual growth since the start of the pandemic.

This pullback in credit card debt growth reflects that more consumers are reining in their spending, with some simply refusing to take on more debt. The current social media trend du jour, broadly termed low-buy or no-buy, has consumers eliminating or greatly reducing nonessential spending. Rising credit card balances may be a big reason why.

Credit card issuers are making their own changes as well, says Rakesh Patel, executive vice president for the Experian Consumer Services Marketplace.

“With the economic climate, along with rising delinquency and charge-off rates, lenders are taking more of a conservative position on acquiring new customers,” Patel says. “To manage risk and impending economic change, they are also looking at alternative data points such as income, cash flow and employment to help make better underwriting decisions.”

As part of Experians regular review of consumer debt and credit trends in the U.S., were taking a look at some top-line numbers around the credit card market that powers the U.S. economy in 2025 and beyond.

Hey there, folks! Ever wondered how deep in the hole the average American was back in 2022 with credit card debt? Well lemme tell ya straight up the average credit card balance per person in 2022 was a hefty $5,910. Yup, that’s a lotta plastic pain for a lotta people. If you’re feeling the weight of your own card statements, you ain’t alone in this financial kerfuffle. In this post, we’re gonna dive into what that number really means why it got so darn high, how it stacks up against other years, and where different folks across the U.S. stood with their debt. Plus, I’ll toss in some tips to help us all climb outta this mess. So, grab a coffee, and let’s chat about this money madness!

What Was the Deal with Credit Card Debt in 2022?

Let’s get right to the meat of it. That $5,910 average balance in 2022 wasn’t just a random figure—it came from a whole lotta spending and economic chaos. Picture this: we’re coming off the tail end of the pandemic, folks are itching to get out, travel, eat at restaurants, and just live a little after being cooped up. But, dang, prices for everything—gas, groceries, you name it—shot through the roof with inflation. So, what do we do? We swipe those cards like there’s no tomorrow.

And here’s the kicker by the end of 2022 the total credit card debt across the U.S. hit a staggering $986 billion. That’s right billion with a “B.” It blew past the pre-pandemic highs and showed just how much we leaned on credit to keep up with life. Compared to 2021, when the average balance was around $5,221, that’s a jump of over 13%. We’re talking double-digit growth in just one year, y’all. It’s like our wallets took a punch and kept on staggering.

Now, I remember 2022 pretty well I was trying to budget for a lil’ vacation, but every time I checked my card statement, it felt like the numbers were mocking me. That average of $5,910? It felt close to home for a lotta us, I bet. But why did it spike so much? Let’s break it down some more

Why Did Credit Card Debt Skyrocket in 2022?

There’s a few big reasons why 2022 turned into a debt disaster for so many. I’ve been mulling over this, and it makes sense when you think about how the world was spinning back then.

- Inflation Went Nuts: Prices for just about everything climbed like crazy. Food, fuel, rent—you couldn’t escape it. When your paycheck don’t stretch as far, swiping a card becomes the quick fix, even if it bites ya later.

- Post-Pandemic Splurging: After being locked down, we were all desperate to get out and spend. Vacations, dinners, concerts—heck, even just buying stuff we missed out on. That “treat yo’self” vibe added up fast.

- Interest Rates Climbed: The big wigs at the Federal Reserve hiked up interest rates to cool down inflation, which meant credit card APRs went through the roof, over 20% on average. If you carried a balance, that interest piled on like a bad snowball.

- Back to Normal Spending: During the pandemic, a lotta folks cut back on big expenses. But in 2022, we went back to regular life—travel, events, all that jazz—and the cards got a workout.

I ain’t saying we’re all reckless, but sometimes life just throws curveballs, and credit cards feel like the only catch. For me, it was car repairs in ‘22 that got me in a bind. What about you? Bet there’s a story behind your balance too.

How Does 2022 Compare to Other Years?

Now, let’s put this $5,910 in perspective by looking at the bigger timeline. I’ve been keeping an eye on these trends, and it’s wild to see how debt’s been creeping up.

- 2021: Average balance was $5,221. That’s a good bit lower than 2022, with about a 1.8% drop from 2020. Folks were still cautious post-COVID, I reckon.

- 2022: Bam, we hit $5,910. A 13.2% jump from ‘21. That’s when inflation and spending really kicked us in the pants.

- 2023: Fast forward, and the average climbed to $6,501. Another increase, but slower, around 10% or so from 2022.

- 2024: By Q3 of ‘24, we’re looking at $6,730 per person. Up 3.5% from ‘23, but the growth ain’t as wild as before. Maybe we’re getting a grip?

- 2025: Early data for this year shows around $6,455. A slight dip from ‘24, but still higher than 2022. We ain’t outta the woods yet.

So, 2022 was kinda the start of a steep climb. It’s like we hit a hill and kept rolling up, just not as fast lately. Makes me wonder if we’ve learned anything, or if high prices are still keeping us strapped.

Who Was Carrying the Most Debt in 2022? Breaking It Down by Age

Not everyone owed the same in 2022. Different age groups had different burdens, and I find this super telling about where folks are in life. Here’s how it shook out with average balances:

| Generation | Age Range (in 2022) | Average Credit Card Debt (2022) |

|---|---|---|

| Generation Z | 18-25 | $2,854 |

| Millennials | 26-41 | $5,649 |

| Generation X | 42-57 | $8,134 |

| Baby Boomers | 58-76 | $6,245 |

| Silent Generation | 77+ | $3,316 |

Gen X was hauling the heaviest load at over eight grand—yikes! I figure they’re in that sandwich stage, paying for kids, maybe helping parents, and juggling mortgages. Millennials weren’t far behind the national average, probably ‘cause we’re buying houses (or trying to) and starting families. Gen Z, bless ‘em, had the least, likely ‘cause they’re newer to credit and ain’t had time to rack it up yet. And the older folks? They’ve either paid stuff off or just ain’t spending as much.

I’m in that Millennial bracket myself, and seeing $5,649 so close to the average makes me sweat a bit. Where do you fall? Does this match your crew’s vibe?

Where in the U.S. Was Debt the Highest in 2022?

Location matters too, ya know. Some states had folks drowning in debt more than others in 2022. Here’s a peek at the highs and lows based on what I’ve come across:

- Highest Average Balances:

- Alaska: Around $7,863 (by ‘24, it was over $8K—ouch!)

- Hawaii: Close to $7,107, probably ‘cause living there costs an arm and a leg.

- Connecticut: About $7,381, with high incomes but high expenses too.

- Lowest Average Balances:

- West Virginia: Around $5,005, one of the few under $5K.

- Kentucky: Hovering near $5,304, keeping it lower than most.

- Iowa: About $5,227, pretty frugal compared to the coasts.

States with higher costs of living or bigger incomes tend to carry more debt. Makes sense, right? If you’re in Cali or New York, your balance might’ve jumped big time in ‘22—some places saw increases of 17% or more! Me, I’ve lived in a middle-of-the-road state, and even then, keeping under that national average felt like a dang Olympic sport.

What Was Behind Those Numbers for Different Groups?

Let’s dig a lil’ deeper into why some generations and states had it worse. For Gen X, like I said, they’re often stuck between caring for young’uns and aging folks, plus they’ve had years to build up debt. Millennials, well, we’re hitting life milestones—weddings, homes, kids—and sometimes credit’s the only way to swing it when savings ain’t there.

Gen Z’s lower debt might be ‘cause they’re just starting out, and many are wary after seeing older folks struggle. Boomers and the Silent Generation often got their finances more locked down, or they’re on fixed incomes and can’t splurge much. Still, even their balances crept up a bit in ‘22.

As for states, places like Alaska and Hawaii got crazy high costs. A loaf of bread might cost double what it does elsewhere! Meanwhile, states like West Virginia might not have the same income levels, but living’s cheaper, so debt stays lower. It’s all a big ol’ puzzle of income, expenses, and lifestyle.

How Did 2022 Debt Affect Us on the Daily?

Carrying around $5,910 or more ain’t just a number—it’s stress, man. I remember checking my balance back then and feeling my stomach drop. High debt means high interest payments, especially with APRs over 20%. That’s money that coulda gone to savings or a fun night out, just vanishing into thin air.

Plus, in 2022, more folks were “revolvers”—that’s fancy talk for carrying a balance month to month—than those paying off their cards in full. About 43% of accounts were revolving, compared to just 33% paying off every month. That means a lotta us were stuck in a cycle, paying interest on interest. It’s a trap I’ve fallen into, and lemme tell ya, it ain’t fun.

And delinquencies—late payments—were ticking up too. Not as bad as pre-pandemic, but still, more accounts were 30, 60, or even 90 days late. That’s a sign folks were struggling to keep up. I’ve been late on a payment or two myself, and the fees just make it worse.

What Can We Do About Credit Card Debt? Tips to Get Free

Alright, enough gloom. Let’s talk about getting outta this hole. Whether your debt in 2022 was near that $5,910 average or way higher, there’s ways to tackle it. I’ve tried a few of these, and they’ve helped me chip away at my own mess.

- Balance Transfer Cards: Grab a card with a 0% intro APR, usually for 12-18 months. Move your debt there, and pay hard on the principal without interest eating you alive. Watch out for transfer fees, though, usually 3-5%. Saved my bacon once!

- Debt Consolidation Loan: If your credit’s decent, get a personal loan with a lower rate than your cards. Use it to pay off the cards, then focus on one monthly payment. Just don’t, and I mean don’t, rack up more card debt after.

- Side Hustles: Pick up extra cash with a gig. Drive for rideshare, freelance, walk dogs—whatever fits. I started selling old junk online, and every bit helps knock down that balance.

- Credit Counseling: If you’re overwhelmed, hit up a nonprofit credit counseling agency. They can negotiate lower rates or payments with your card companies and set up a plan. Might ding your credit short-term, but long-term, it’s a win.

- Budget Like Crazy: Track every penny. Cut out non-essentials—sorry, daily lattes—and throw extra at your debt. I use a lil’ app to keep me honest, and it’s a game-changer.

Pick one or mix ‘em up, but the key is action. Sitting on that 2022 debt—or whatever you got now—ain’t gonna fix itself. We gotta hustle and get free.

Why Does Knowing the 2022 Average Matter Today?

You might be thinking, “Why care about 2022 when it’s behind us?” Fair point, but hear me out. That $5,910 benchmark shows us where we were when things got tough. It’s a reminder of how fast debt can pile up when life gets pricey. Comparing it to today—where averages are over $6,400—tells us the problem ain’t gone; it’s just shifting.

Plus, understanding 2022 helps us see patterns. If Gen X was hit hardest then, are they still struggling? If inflation drove debt up, what happens if prices spike again? It’s like looking at an old photo to see how much you’ve grown—or if you’re still wearing the same bad outfit, financially speaking.

For me, looking back at ‘22 makes me double down on not letting my balance creep up again. It’s a wake-up call to keep an eye on spending, especially with interest rates still biting hard.

Let’s Wrap This Up with Some Real Talk

So, there ya have it—the average credit card debt in 2022 was $5,910, a number that hit hard for millions of us. It came from a storm of inflation, post-pandemic spending, and sky-high interest rates that made every swipe hurt more. We saw how it varied by age, with Gen X carrying the biggest load, and by state, with places like Alaska topping the charts. Comparing it to years before and after shows we’ve been on a rough ride, and it ain’t over yet.

But, hey, we ain’t helpless. Whether you’re still paying off 2022 debt or just trying not to repeat history, there’s ways to fight back. Balance transfers, side gigs, budgeting—pick your weapon and swing. I’m rooting for us all to get outta this credit card quicksand. Got a story about your debt journey from back then? Drop it in the comments; I’d love to hear how you’re handling it.

Let’s keep this convo going. Share this with a buddy who might need a nudge to face their balance, and let’s work together to make debt a thing of the past. We got this!

Question: How often do you pay off your credit card balance in full?

Finally, consider each generations demand for additional credit in the broader context of how much of their credit each one is using. On average, Gen Z, millennials and Gen X use more than 30% of their credit, while baby boomers and the Silent Generation use less than 30%. Reading across the groups, the strong relationship between average credit utilization and average FICO® Score becomes quite apparent.

| Generation | Average Credit Utilization Ratio | Average FICO® Score |

|---|---|---|

| Generation Z | 37% | 681 |

| Millennials | 36% | 691 |

| Generation X | 34% | 709 |

| Baby boomers | 21% | 746 |

| Silent Generation | 12% | 760 |

Source: Experian data as of Q3 2024

Average Credit Card Balance Increased by 5% to $6,730

The average credit card balance among consumers was $6,730 as of Q3 2024, up by $229 from the previous years average of $6,501. That increase in revolving credit was more or less in line with inflation, which ranged from 2.4% to 3.7% (at an annual rate) between September 2023 and September 2024.

| 2022 | 2023 | 2024 | 2023-2024 Change |

|---|---|---|---|

| $5,910 | $6,501 | $6,730 | +$229 (+3.5%) |

Source: Experian data from Q3 of each year

Credit Card Debt Is RUINING My Life

FAQ

How many people have $20,000 in credit card debt?

44% say inflation has “caused them to carry a larger monthly credit card balance.” Of those respondents, 39% have at least $10,000 to $20,000 of credit card debt. That includes 26% of Millennials.

How much does the average person have in credit card debt?

What is the 2/3/4 rule for credit cards?

Is $6,000 in credit card debt a lot?

The average American household has over $6,000 in credit card debt, which can be a challenging amount to manage. If you’re just making minimum payments, expect to stay in credit card debt for many years – about 25 years on $6,000, by our calculations.