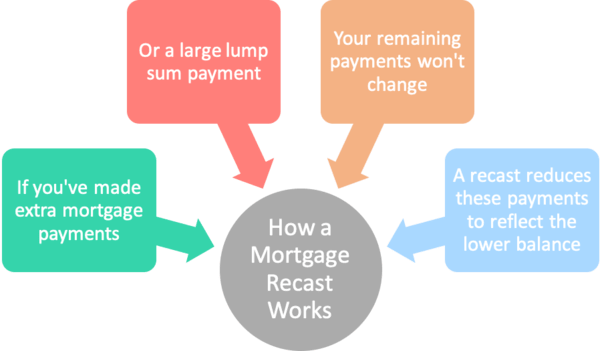

If you have a large sum of cash burning a hole in your pocket and are looking for lower mortgage payments, consider asking your lender for a mortgage recast. A mortgage recast is a way to change how much you pay monthly without refinancing your mortgage. The lender will apply your extra funds to your loan balance, then recalculate how much you have to pay each month. You’ll see lower monthly payments and save thousands in interest over the life of the loan.

We’ll walk you through the finer details of a mortgage recast, go over how it differs from a refinance and help you decide whether it’s right for you.

A recast fee is a one-time administrative fee charged by mortgage lenders when homeowners request a mortgage recast. Recasting a mortgage involves making a lump sum payment toward the loan balance and having the lender re-amortize the remaining principal over the remaining loan term. This results in lower monthly payments without refinancing the loan.

What is Mortgage Recasting?

Mortgage recasting allows borrowers to reduce their monthly mortgage payments by making a lump sum payment toward the principal balance. The lender then re-calculates the loan payments based on the updated balance and remaining term.

Unlike refinancing, mortgage recasting does not change the interest rate or loan terms The borrower continues paying the same interest rate but on a lower principal amount.

To recap the main steps in recasting a mortgage are

- Contacting the lender to confirm recast eligibility

- Making a large lump-sum payment toward the principal

- Paying a recast fee charged by the lender

- Having the lender re-amortize the loan and provide updated monthly payments

Recasting can save thousands of dollars in interest over the loan term while providing immediate monthly payment relief. It offers a simpler and less expensive alternative to refinancing for borrowers who can afford a large lump-sum payment.

What is a Recast Fee?

The recast fee is an administrative fee charged by the mortgage lender to process the recast request. It covers the lender’s costs for re-amortizing the loan balance and generating a new payment schedule.

Typical recast fees range from $100 to $500, with an average of around $250. The exact fee amount depends on the lender. Government-backed FHA, VA, and USDA loans do not allow recasting, so the fee only applies to conventional mortgages.

The relatively small recast fee provides big savings compared to refinancing closing costs that can total 2% to 6% of the mortgage amount. The streamlined administrative process is another recast benefit versus the extensive paperwork and underwriting involved in refinancing.

What are the Requirements for Mortgage Recasting?

Here are some common requirements borrowers must meet to recast their mortgage:

-

Loan Type – Most conventional loan types can be recast, including fixed-rate, adjustable-rate, jumbo, and high-balance mortgages. Government-backed loans are not eligible.

-

Minimum Lump Sum – Lenders often require minimum lump-sum payments of $5,000 to $10,000 towards the principal to process a recast.

-

Payment History – Many lenders mandate 12 months of on-time payments before approving a recast request.

-

Home Equity – Some lenders want borrowers to have 20% to 30% equity before recasting. This ensures the borrower has sufficient collateral.

-

Prepayment Penalty – Loans with prepayment penalties cannot be recast until the penalty period expires.

Always confirm the specific recast requirements with your mortgage lender before initiating the process. Having a loan that allows recasting is the critical first step.

Pros and Cons of Mortgage Recasting

Recasting a mortgage provides several benefits but also some limitations to consider.

Pros of Recasting

- Lower monthly mortgage payments

- Interest savings over the loan term

- Maintain existing low interest rate

- Avoid refinance closing costs

- Streamlined documentation process

Cons of Recasting

- Large lump sum payment required

- Loan payoff date unchanged

- Not available for all mortgage types

- Some lenders don’t offer recasting

- Small administrative fee charged

For borrowers who meet eligibility requirements and have funds available, recasting offers an easy way to reduce mortgage payments without the hassle of refinancing. However, it is not universally available and requires having extra cash to make the principal paydown.

Alternatives to Mortgage Recasting

If you cannot or choose not to recast your mortgage, here are a couple alternatives for reducing your payments or interest costs:

-

Refinancing – This involves taking out a new mortgage loan to pay off your existing one. You can potentially get a lower rate or change loan terms.

-

Making Extra Principal Payments – Adding even small extra amounts to your regular mortgage payments will pay down the balance faster and save on total interest.

-

Biweekly Payments – Dividing your monthly payment in half and paying every two weeks accelerates payoff by making an extra monthly payment each year.

-

Loan Modification – You may qualify to have your lender formally modify the loan terms to reduce your monthly payment through an extended term, interest rate reduction, or other changes.

For borrowers who don’t quite have the lump sum for a recast, these options allow you to chip away at your mortgage principal or interest costs over time.

Is Mortgage Recasting Right for You?

Here are some final tips on whether mortgage recasting aligns with your situation:

-

Recasting works best if you have a large cash amount readily available and want immediate payment relief.

-

Make sure your lender allows recasting for your specific loan program before pursuing this option.

-

Consider if you could qualify for refinancing and a better rate with your improved financial profile before recasting.

-

Don’t tap emergency funds or retirement savings to pay the recast lump sum – prioritize financial security.

-

Recasting may not be your best option if you want to pay off your home faster or shorten the loan term.

While not universally available, mortgage recasting provides a fast, low-cost way to garner mortgage savings if you meet eligibility criteria. Understanding the recast process, fee involved, and alternatives can help determine if this option makes sense for your situation. Carefully weigh the pros, cons and your financial priorities when deciding.

Mortgage recast example

Let’s say your loan is a 30-year fixed-rate mortgage with a 6.94% interest rate and a remaining balance of $98,900. You’ve decided to put $60,000 toward the recast, and your lender is charging a $500 recast fee. Here’s how a recast will change your mortgage:

| Current loan | After a recast | |

|---|---|---|

| Monthly payment amount | $1,983.83 | $769.71 |

| Remaining interest amount | $18,118.89 | $7,755.08 |

In this example, recasting will save you $1,214 per month and $9,864 over the life of the loan.

Pros and cons of a recast mortgage

- Lower payments. You can get a lower monthly payment and pay less interest over the life of the loan.

- Same interest rate. Your current interest rate stays the same so, at times when you can’t refinance into a loan with a lower interest rate, a recast can still make sense.

- Lower fees. Most lenders charge a $150 to $500 fee for a mortgage recast, which is much cheaper than paying refinance closing costs.

- Less paperwork. You won’t need to provide income documents or any other qualifying financial paperwork like you would when refinancing.

What is a Mortgage Recast? Pros and Cons

FAQ

What is a typical recasting fee?

You pay the recasting fee, if applicable: If your lender charges a fee for recasting, it’ll typically cost between $150 and $500.

Is loan recasting a good idea?

A mortgage recast is a good idea if you’ve paid down your mortgage balance quickly and prefer to have lower monthly payments.

What is the purpose of a recast?

A mortgage recast is when a borrower makes a lump-sum payment toward the balance on their home loan, and the lender recalculates their repayment schedule based on the new lower loan balance. The primary purpose of mortgage recasting is to reduce your monthly mortgage payment.

What is an example of recasting a mortgage?

Let’s say you just came into $100,000 and you started with a $300,000 mortgage. When doing a recast, you would put this $100,000 down toward the principal. You’d tell the bank you’d want to do a recast and they would reduce the balance from $300,000 to $200,000.