One of your top priorities when buying a house is probably having enough cash on hand to make a down payment. You may wonder how much you need to save for a down payment or if buying a home without one is possible.

We’ll look at the typical down payment requirement for different loan types and discuss the average amount that buyers pay upfront so you’ll have an idea of what to expect on your journey to homeownership.

Buying a house is an exciting milestone in life, but saving up for the down payment can feel daunting As a first-time homebuyer, you may wonder what percentage of the home’s price you should plan to put down The answer isn’t one-size-fits-all, but looking at the average down payment can provide a helpful benchmark.

Typical Down Payment Amounts

According to data from Forbes Advisor, the average down payment for a house nationwide is 14.4% of the purchase price, or around $34,248 based on median home values. However, this percentage varies significantly based on factors like your location, credit, and whether you’ve owned a home before.

For example, first-time homebuyers typically put down less than repeat buyers who have built up home equity And those purchasing in high-cost areas like California or New York need larger down payments to buy a comparable home to other parts of the country.

Here’s an overview of typical down payments:

- Nationwide: 14.4%

- First-time buyers: 6-10%

- Repeat buyers: 17-23%

- High-cost areas: 15-20%+

While 20% is ideal, it’s becoming less common for buyers to put that much down. Per NerdWallet, the median down payment across all buyers is around 18% of the purchase price.

Minimum Down Payment Requirements

The minimum you can put down depends on the mortgage program:

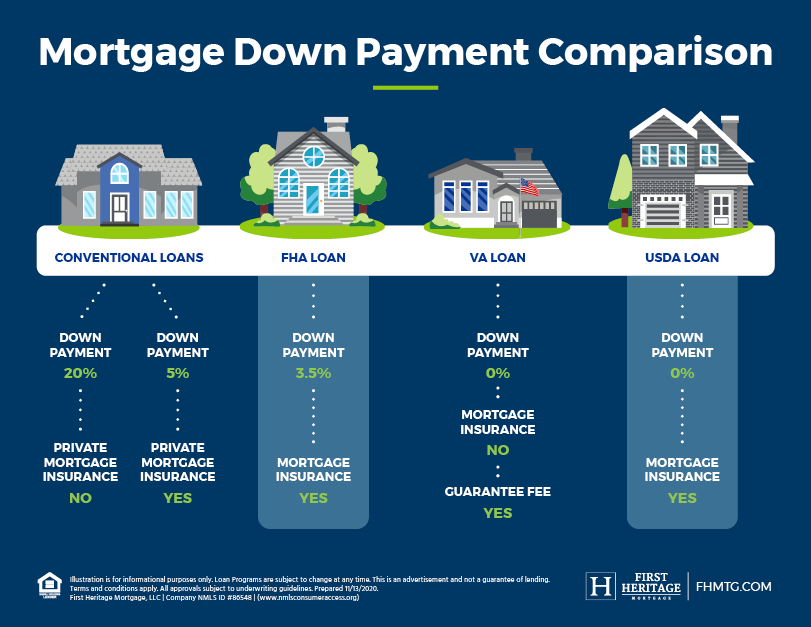

- Conventional loans: Usually 3-5%

- FHA loans: 3.5%

- VA/USDA loans: 0%, in most cases

Conventional loans with down payments under 20% require private mortgage insurance until you reach that threshold through payments or appreciation. Government programs charge upfront and annual mortgage insurance fees but allow lower down payments or none at all if you qualify.

Jumbo loans typically call for a minimum 10-20% down payment depending on the lender, since they exceed conforming loan limits and are viewed as higher risk.

How Much Should You Put Down?

Aim to put down as much as you’re comfortable with, keeping a healthy emergency fund and money for closing costs and home repairs. A higher down payment results in lower interest rates and monthly payments. But you don’t want to drain all your savings.

Run the numbers with a down payment calculator to see the impact on your monthly payment. If you’re having trouble saving up, look into down payment assistance programs offered in your state.

Here are some tips for boosting your down payment savings:

- Reduce monthly expenses to free up more cash flow

- Pick up a side gig for extra income

- Build savings with your tax refund each year

- Withdraw retirement account contributions penalty-free

- Ask family for gift funds with proper documentation

Down Payment Trends and Statistics

While down payments are rising in some of the most affordable areas, high-cost markets like California, Washington, and New Jersey see declines as home prices drop, per Realtor.com. Here are some interesting down payment stats:

- Louisiana has the lowest down payment of 9.2%

- Washington, D.C. has the highest at 20.4%

- The typical down payment drops from 17% for ages 59-68 to 10% for ages 25-33

- 12 states have average down payments under 12% of the purchase price

The bottom line is that today’s 20-something first-time buyers rarely put down 20% on their first home. Aim for an amount you can manage based on your budget and goals. With the right mortgage program and strategy, homeownership is achievable even with a modest down payment.

Is it better to put a large down payment on a house?

Making a larger down payment can seem like a high priority because it typically results in paying less interest over time and eliminating private mortgage insurance (PMI) fees on a conventional loan (assuming the down payment amounts to at least 20% of the purchase price).

It’s essential, however, to analyze your financial situation to determine whether a large down payment is a good option for you. Waiting until you have enough savings for a large down payment could lead you to spend more money in the meantime.

You could end up paying more in rent, for example, than you would save by eliminating PMI and reducing the amount of interest you pay. You could also end up missing an ideal moment to make a move in a hot housing market.

Getting approved for a mortgage will reveal the kind of terms that the down payment you plan to make will qualify you for.

Pros of a 20% down payment

Avoiding PMI isn’t the only benefit of putting 20% down on your loan. Other advantages include:

- Access to a lower interest rate

- A smaller loan amount

- Lower monthly mortgage payments

- Less interest owed over the life of the loan

You can save thousands of dollars over time by reducing the amount of money you borrow and the interest you pay on the mortgage loan.

How important is the down payment when buying a house? (CLIP)

FAQ

How much do you need for a down payment on a $300,000 house?

If you want to buy a $300,000 house, your down payment amount can range from $9,000 to $60,000. That’s between 3% and 20% of the home price, depending on your loan type. A conventional loan typically requires a down payment of at least 3%. But an FHA loan requires 3.5%, or $10,500.

Is 10% down payment enough for a house?

While 20% down is often recommended, putting down 10% is still a solid option for many home buyers, especially if you have good credit and stable income.

What is the normal down payment on a home?

| State | Average down payment (percentage) | Median down payment (dollars) |

|---|---|---|

| California | 18.5% | $96,100 |

| Colorado | 18.3% | $75,048 |

| Connecticut | 17.8% | $57,025 |

| Delaware | 17.6% | $53,646 |

Is $10,000 a good down payment for a house?

In most parts of the country, a $10,000 down payment can get you a lovely home. Only in really expensive housing markets might it be too little. But, if you work in one of those, there’s a good chance you can afford to save more. Be sure to thoroughly research down payment assistance programs where you’re buying.

How much a down payment should you put on a house?

Next, it’s wise to figure out a precise amount you can reasonably expect to use as a down payment. “Ideally, you want a down payment of at least 20% of the home’s purchase price,” Ramsey wrote. “Putting down 20% allows you to avoid paying for private mortgage insurance (PMI).” “If you’re a first-time home buyer, saving 5-10% is okay too.

What is the average down payment for a house in 2022?

The National Association of Realtors (NAR) states that the average down payment on a house for first-time home buyers is 6% versus 17% for repeat buyers in 2022. However, the share of first-time buyers fell to 22% in 2022, dropping from 34% in 2021. The average down payment for a house differs widely by state due to different home prices.

How much Down do you need to buy a house?

The standard down payment is 20 percent, but there are loan options available that require as little as 3 percent down. According to the Zillow Group Consumer Housing Trends Report, 52 percent of repeat buyers put 20 percent or more down.