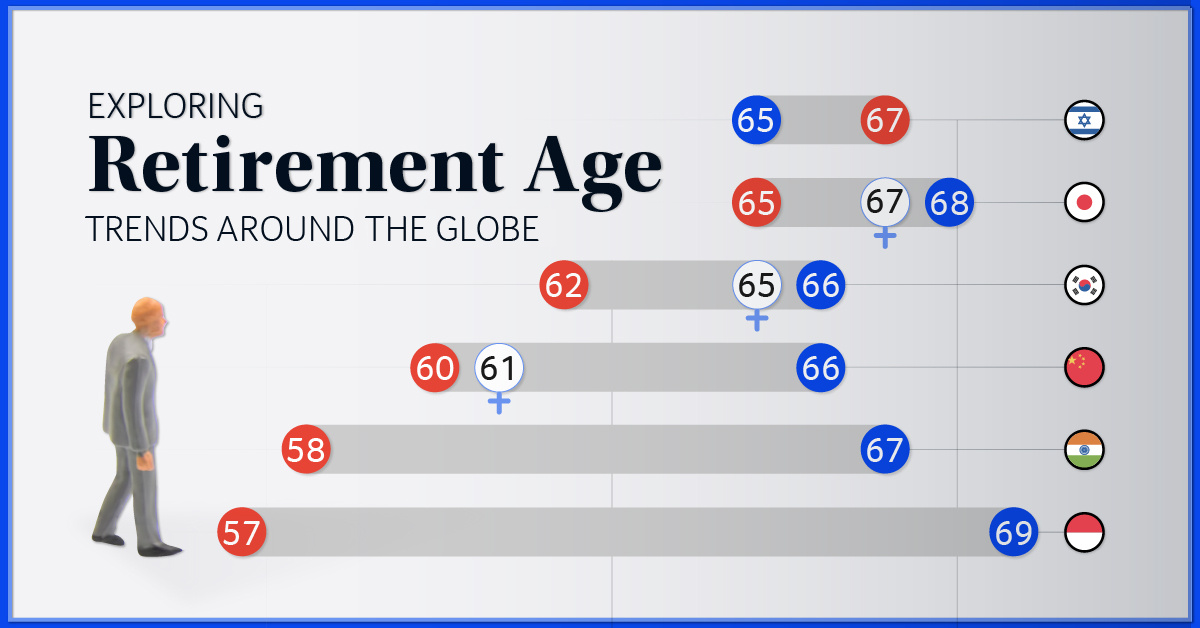

Have you been daydreaming about saying goodbye to your morning commute and hello to leisurely breakfasts on your patio? If you’re approaching your mid-60s, retirement might be on your mind more than ever. But is 66 actually a good age to retire? Let’s dive into everything you should consider before making this life-changing decision.

Why Age 66 Matters in the Retirement Timeline

The age of 66 falls right in that sweet spot where several important retirement milestones converge. It’s not arbitrary – there are some solid reasons why many financial experts consider this a strategic time to retire.

For starters, depending on your birth year, your Full Retirement Age (FRA) for Social Security is likely between 66 and 67. This means you can collect your complete Social Security benefit without any reductions. If you were born between 1943 and 1954, your FRA is exactly 66. If you were born after that, your FRA increases gradually until it reaches 67 for those born in 1960 or later.

The Financial Picture at 66

By age 66, most of us have worked for decades and saved a lot of money for retirement. But is it enough? Here’s how your money might look now that you’re this old:

Social Security Benefits

At age 66, you can get your full Social Security retirement benefit. This is a huge benefit compared to retiring earlier. If you had retired at age 606.2, which is the earliest age to claim Social Security, your benefit would be cut by about 25 to 30 percent.

Medicare Coverage

You can already get Medicare, which starts when you turn 65. This gets rid of one of the hardest parts of retiring early: getting cheap health insurance. These changes will make a HUGE difference for most retirees I’ve talked to!

Retirement Savings

By 66, you’ve likely maxed out your peak earning years and had significant time to build your nest egg. You’ve also given your investments more time to grow through compound interest.

Required Minimum Distributions

You’re not yet required to take minimum distributions from your retirement accounts, which typically start at age 72 (previously 70½), giving you more flexibility in your withdrawal strategy

Questions to Ask Yourself Before Retiring at 66

Before you decide if 66 is the right age for you to retire, here are some important questions you should honestly answer:

1. Can you afford to stop working?

This is the million-dollar question (sometimes literally). Have you calculated your retirement income needs? A common rule of thumb suggests you’ll need about 70-80% of your pre-retirement income to maintain your standard of living.

2. Are you ready to stop working?

Beyond finances, there’s the psychological aspect. Some people love their jobs and aren’t mentally prepared to retire. My neighbor Tom retired at 66 and was back consulting part-time within 3 months because he missed the mental stimulation!

3. Can your retirement portfolio handle market declines?

At 66, you still have a potentially long retirement ahead – possibly 20-30 years. Is your portfolio diversified enough to weather market fluctuations?

4. What will you be retiring TO?

Retirement isn’t just about leaving work behind; it’s about embracing a new lifestyle. Do you have hobbies, volunteer opportunities, travel plans, or other activities to fill your days?

5. Have you considered healthcare costs?

While Medicare provides coverage, it doesn’t cover everything. Have you factored in supplemental insurance costs and potential long-term care needs?

Pros and Cons of Retiring at 66

Let me break down the advantages and disadvantages of choosing 66 as your retirement age:

Pros:

- You’re eligible for full Social Security benefits

- Medicare coverage is already in place

- You’ve had more time to build your retirement savings

- You can still expect many healthy, active retirement years

- You avoid early withdrawal penalties from retirement accounts

Cons:

- You miss out on increased Social Security benefits from delaying until 70

- You have fewer years of peak earning potential compared to working until 70

- Your retirement savings need to last longer than if you retired later

- You may miss the social connection and purpose that work provides

How Retiring at 66 Compares to Other Ages

To help you see the bigger picture, I’ve put together this comparison of different retirement ages:

| Age | Social Security | Medicare | Retirement Savings | Considerations |

|---|---|---|---|---|

| 55 | Not eligible yet | Not eligible yet | Needs to last ~30+ years | Early withdrawal penalties; need health insurance |

| 62 | Eligible but reduced by ~25-30% | Not eligible yet | Needs to last ~25+ years | Need health insurance until 65 |

| 65 | Eligible but reduced if before FRA | Just became eligible | Needs to last ~20+ years | First age for Medicare |

| 66 | Full benefits for many | Already eligible | Needs to last ~20+ years | Full retirement age for many |

| 70 | Maximum benefits (8% increase per year after FRA) | Already eligible | Needs to last ~15+ years | Less time to enjoy retirement |

Financial Reality Check: The Numbers Behind Retiring at 66

Let’s get down to brass tacks with some real numbers. If your goal is to have an annual retirement income of $60,000, here’s how retiring at different ages might affect your savings needs:

- At age 62: If you receive about $22,120/year from Social Security, you’d need to withdraw about $37,880/year from savings, requiring approximately $947,000 in total savings (assuming a 4% withdrawal rate).

- At age 66: If you receive about $30,000/year from Social Security, you’d need to withdraw about $30,000/year from savings, requiring approximately $750,000 in total savings.

- At age 70: If you receive about $39,690/year from Social Security, you’d need to withdraw about $20,310/year from savings, requiring approximately $507,750 in total savings.

These numbers show that waiting until 66 versus 62 can significantly reduce the amount you need to have saved!

Making Your Decision: Is 66 Right for YOU?

Ultimately, the “right” retirement age isn’t about what works for most people—it’s about what works for YOU. Here are some factors that might make 66 a particularly good retirement age for your situation:

- You’ve reached your financial goals and have sufficient savings

- Your job is physically demanding or causing health issues

- You have plans or dreams you want to pursue while still relatively young and healthy

- Your spouse is already retired or retiring soon

- You’ve calculated that your Social Security benefits plus savings will meet your needs

On the flip side, you might consider working beyond 66 if:

- You enjoy your work and it gives you purpose

- You want to maximize your Social Security benefits

- You’re still catching up on retirement savings

- You want to continue employer-sponsored health benefits

- You have longevity in your family and are concerned about outliving your money

Steps to Take if You’re Planning to Retire at 66

If you’ve decided that 66 is indeed the right age for you to retire, here’s what you should do in the years leading up to it:

- Meet with a financial advisor – About 10 years before retirement is ideal to start serious planning

- Calculate your expected expenses – Be realistic about your lifestyle and healthcare costs

- Determine your income sources – Social Security, pensions, retirement accounts, etc.

- Consider a retirement “test run” – Live on your projected retirement budget for a few months

- Create a withdrawal strategy – Decide which accounts to tap first

- Plan your Social Security claim – Decide exactly when and how to claim benefits

- Review your healthcare options – Look into Medicare supplemental plans

- Pay down debt – Aim to enter retirement with as little debt as possible

- Update your estate plan – Ensure your will, power of attorney, and healthcare directives are current

- Consider a phased retirement – Maybe reduce hours before fully retiring

Real Talk: What Nobody Tells You About Retiring at 66

I wanna get real with you for a minute. While 66 can be a great age to retire from a financial perspective, there are some things people don’t talk about enough:

- The identity shift is HARD – After decades of defining yourself by your career, the transition can be jarring

- You might get bored – I’ve seen it happen to friends who retired without enough interests or activities lined up

- Your social circle might shrink – Many of our social connections come through work

- You might disagree with your spouse – If you’re married, suddenly spending 24/7 together requires adjustment

- Healthcare costs can shock you – Even with Medicare, out-of-pocket costs can be higher than expected

So, is 66 a good age to retire? For many people, yes! It offers a nice balance between financial security and having plenty of healthy years to enjoy retirement. You’ll receive your full Social Security benefit, you’re covered by Medicare, and you’ve likely had plenty of time to build your nest egg.

However, the perfect retirement age is different for everyone. It depends on your financial situation, health, career satisfaction, and personal goals. The most important thing is to make a thoughtful, informed decision rather than simply retiring when you hit a certain age.

What age are you planning to retire? Have you thought about these considerations? I’d love to hear your thoughts in the comments below!

The PERFECT Age to Retire (Backed by Data)

FAQ

Is 66 too early to retire?

The traditional retirement age in the U. S. is typically considered 65 (67 for younger generations), but many people choose to retire before or after this age. Knowing your retirement readiness is a personal decision that hinges on both financial and non-financial factors.

What is the average Social Security check at the age of 66?

NerdWallet and The Motley Fool say that the average Social Security check for a worker retired at age 66 in late 2024 was about $1,764.

Is it better to retire at 66 or 67?

It depends on health and wealth. Generally, it is better to wait until 70. Full Retirement Age of 67 (for those born after 1960) is next best. Age 62 is a worst case scenario. Every year one waits they receive an approximate 8% increase in the annuity. An increase in annuity rate that high is tough to beat.

What is the healthiest age to retire?

Retirement Researchers: Insights into Longevity and the Optimal Retirement Age. Retirement researchers reveal that retiring between 65 and 70 often maximizes longevity by balancing mental stimulation, social engagement, and financial stability.

Is 65 a good age to retire?

People used to think that 65 was the best age to retire, but now it seems like people are retiring at different times and in different ways. “This is not your parents’ or grandparents’ retirement,” says Marilyn Suey, certified financial planner and founder of The Diamond Group Wealth Advisors in San Ramon, California.

What is a good age to retire?

Part of a sound retirement planning strategy involves choosing the right age to retire. Most people retire between the ages of 66 and 67. This is when they can start getting their full Social Security retirement benefit.

Is 66 a good age to retire?

Determining whether you’re ready for retirement depends on a variety of personal and non-financial factors. Pros of Retiring at 66: Full Social Security Benefits: For those born between 1943 and 1959, 66 is the full retirement age for Social Security benefits. This means you can receive the maximum amount of benefits without any reductions.

What is a good retirement age for a 60-year-old?

For those born in 1960 or later, the full retirement age is 67. Between the ages of 67 and 70, your Social Security benefit will increase by 8% for each year you delay taking it until you turn 70.

What happens if you retire at 66?

Increased Financial Security: By age 66, many individuals have accumulated a significant amount of savings and investments, which can provide financial security during retirement. Opportunity to Work Part-Time: If you choose, you can still work part-time after retiring at 66. This can provide additional income and keep you engaged in the workforce.

What is a normal retirement age?

The normal retirement age is typically 66 to 67 for most people – this is when you can begin drawing your full Social Security retirement benefit. However, the median age is only 62, meaning many people retire before becoming eligible for their full Social Security benefits.