Key takeaway: Your 401(k) is part of your net worth, but its role in defining “high net worth” depends on liquidity and specific criteria.

Hey there! I’ve been diving deep into personal finance lately, and one question keeps popping up in conversations with my friends and family “Is a 401(k) considered an asset?” It’s actually a super important question that affects how you view your financial health, especially when planning for major life events like buying a home, getting married, or unfortunately, going through a divorce

The short answer? Yes, your 401(k) is definitely an asset. But there’s a lot more to understand about why that matters and how it impacts your overall financial picture. Let’s break it down together!

What Exactly Is an Asset Anyway?

Before we dive into the 401(k) specifics, let’s get clear on what an asset really is. In the simplest terms, an asset is anything you own that has positive financial value.

Assets typically include

- Cash and cash equivalents

- Investment portfolios (stocks, bonds, mutual funds)

- Real estate properties

- Vehicles

- Valuable personal items

- And yes, retirement accounts!

Basically, if something makes you wealthier or could potentially be converted into money, it’s considered an asset. The key point is that assets have positive value—meaning they’re worth more than what you owe on them.

Understanding Your 401(k) as an Asset

Most of the time, your employer will set up a 401(k) for you. The account is managed by your employer, but it is yours as an individual. You can choose the investments in the account, borrow money against it (though I don’t normally suggest this!), and move it from one employer to another.

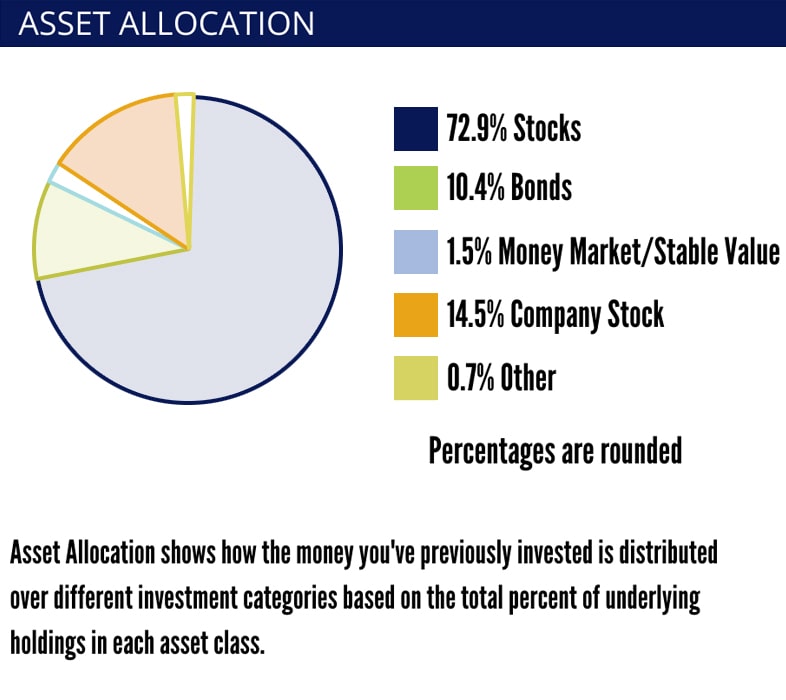

Your 401(k) holds a mix of investments that might include:

- Stocks

- Bonds

- Mutual funds

- Index funds

- Cash

This portfolio of investments makes your 401(k) a financial asset—and potentially a very valuable one! In fact, for many Americans, retirement accounts are the second-largest portion of household net worth, right after home equity.

Why It Matters That Your 401(k) Is an Asset

Understanding that your 401(k) is an asset matters for several reasons:

1. Net Worth Calculations

When you’re figuring out your net worth (assets minus liabilities), your 401(k) should definitely be included. It gives you a more accurate picture of your financial health.

2. Major Life Events

During significant life events, you may need to disclose your assets:

- When applying for a mortgage

- During marriage or divorce proceedings

- When creating an estate plan

- For bankruptcy filings

3. Financial Planning

Recognizing your 401(k) as an asset helps you make better decisions about your overall financial strategy. It’s not just “money for later”—it’s real wealth you’re building now.

Assets vs. Liabilities: Know the Difference

It helps to know what something is against in order to fully understand why your 401(k) is an asset.

A liability is anything that costs you money or makes you owe money. Common liabilities include:

- Credit card debt

- Student loans

- Car loans

- Mortgages (when you owe more than the home is worth)

It’s important to note that just because you lose money on an investment doesn’t mean it becomes a liability. It’s still an asset even if the value of your 401(k) drops during a market downturn. It’s just worth less than it did before.

The real test is whether you can sell something and receive money (even if it’s less than you paid), versus owing money on something that exceeds its value.

Formal vs. Practical Asset Definitions

When determining what counts as an asset, there are two main approaches:

Formal Definition

This includes literally anything with potential or realized financial value—from your home down to small items like books or furniture. This comprehensive approach is typically used for legal proceedings, tax purposes, or divorce settlements.

Side note: When doing formal asset accounting, items worth less than $25 are usually excluded as “de minimis” (too minor to matter).

Practical Definition

This focuses on things you could reasonably convert to cash if needed—items with meaningful value that someone would actually want to buy. Under this definition, you wouldn’t count old paperbacks or random household items.

Under BOTH definitions, your 401(k) qualifies as an asset! It contains investments that have real, convertible value.

Real-World Example: How Your 401(k) Functions as an Asset

Let me walk you through a quick example to illustrate why your 401(k) is undoubtedly an asset:

Sarah has $100,000 in her 401(k), invested in a mix of stock and bond funds. This account:

- Has real monetary value

- Could be converted to cash (though with potential tax penalties if withdrawn early)

- Grows in value over time

- Belongs to Sarah personally

Even though Sarah can’t easily access this money without penalties until retirement age, it’s still her asset. It represents a portion of her total wealth and financial security.

When Might Your 401(k) Not Be an Asset?

There’s really only one scenario where your 401(k) might not be considered an asset: if it has a negative balance. This is extremely rare and would likely only happen if:

- You’ve borrowed against your 401(k) and owe more than its current value

- You’ve made prohibited transactions that resulted in penalties exceeding the account value

For the vast majority of people, a 401(k) will always be an asset—even during market downturns when the value temporarily decreases.

Do You Have to Claim Your 401(k) as an Asset?

This is where things get interesting. In most financial situations where you’re required to list assets, yes, you’ll need to include your 401(k). This includes:

- When applying for certain types of financial aid

- During divorce proceedings

- When filing for bankruptcy

- In estate planning

However, one benefit of 401(k) accounts is that they have special protections in bankruptcy proceedings. Under federal law, 401(k) assets are generally protected from creditors, meaning you can keep these retirement funds even if you file for bankruptcy.

The Bigger Picture: 401(k)s in Your Financial Health

Your 401(k) isn’t just any asset—it’s potentially one of your most important ones for long-term financial security. Here’s why:

Tax Advantages

Contributions to traditional 401(k)s are tax-deferred, meaning you don’t pay income tax on that money until withdrawal. This can significantly boost your saving power.

Employer Matching

Many employers match a portion of your contributions—essentially giving you free money that immediately increases your asset’s value.

Long-term Growth

Through the power of compounding returns, your 401(k) can grow substantially over decades of saving.

Retirement Security

This asset is specifically designed to provide income during your retirement years when you’re no longer earning a salary.

Common Questions About 401(k)s as Assets

Can creditors take my 401(k) if I default on debts?

Generally no. 401(k) accounts have strong protections against most creditors under federal law.

Should I include my 401(k) when calculating my net worth?

Absolutely! It’s a significant financial asset that represents your future security.

Does my 401(k) count as an asset for mortgage qualification?

Typically, lenders don’t count retirement assets directly when calculating your debt-to-income ratio. However, they may consider these assets as part of your overall financial picture and stability.

What happens to my 401(k) asset during divorce?

In most states, 401(k) assets accumulated during marriage are considered marital property subject to division. The exact split depends on your state’s laws and your specific situation.

Maximizing Your 401(k) as an Asset

Since your 401(k) is indeed a valuable asset, here are some strategies to maximize its value:

-

Contribute enough to get your full employer match – This is essentially free money that immediately increases your asset’s value.

-

Diversify your investments – Spread your 401(k) holdings across different asset classes to manage risk.

-

Regularly review your allocations – As you age, you might want to adjust your investment mix to become more conservative.

-

Avoid early withdrawals – Taking money out before retirement not only reduces your asset’s value but also incurs taxes and penalties.

-

Consider increasing contributions over time – As your income grows, try to contribute more to build this asset faster.

The Bottom Line

Your 401(k) is definitely an asset—and potentially one of your most significant ones. It’s a portfolio of investments that holds real financial value and belongs to you, even if you can’t access it without penalties until retirement age.

Understanding that your 401(k) is an asset helps you make better financial decisions and gives you a more accurate picture of your overall wealth. While it’s designed primarily for retirement, recognizing its place in your current financial landscape is crucial for comprehensive planning.

So next time someone asks “Is a 401(k) an asset?”—you can confidently answer yes and explain exactly why that matters!

Need Help With Retirement Planning?

If you’re looking to make the most of your 401(k) and other retirement assets, it might be worth consulting with a financial advisor. They can help you develop a personalized strategy based on your specific goals and circumstances.

Remember, your 401(k) isn’t just some abstract account for the future—it’s a real, valuable asset that’s working for you right now. Treat it with the attention and care it deserves!

What questions do you have about your 401(k) or other retirement assets? Drop ’em in the comments below, and I’ll do my best to answer!

High Net Worth Requirements

Once you know your net worth, figuring out if you’re a high-net-worth person is all about your liquid assets, or things that can be quickly turned into cash. Generally, someone is considered a high-net-worth individual (HNWI) if they have at least $1 million in liquid assets.

The Securities and Exchange Commission (SEC) uses slightly different benchmarks. According to the SEC, a person qualifies as wealthy if they have:

- $750,000 in investable assets, or

- $1.5 million in total net worth.

In 2023, the global HNWI population reached 22. 8 million people, controlling about $86. 8 trillion in wealth. North America leads with the largest share, home to approximately 7. 9 million HNWIs.

However, not all assets count toward high-net-worth status. The following are typically excluded:

- Primary residence value

- Fine art collections

- Antiques

- Other illiquid assets

These exclusions ensure that wealth calculations focus on resources that are readily accessible.

401(k)s in Net Worth Calculations

A 401(k) is a key part of net worth calculations. These accounts hold securities and investment products that carry either current or potential value. In the U. S. , 401(k)s and other retirement accounts make up a large portion of household wealth, often dominating financial portfolios.

For individuals with significant wealth, 401(k)s and IRAs can account for as much as 55% of their total assets.

That said, there are instances where adjustments to the value of these accounts may be necessary.