Everyones dream retirement looks different. If you want to travel, play golf, fish, volunteer, spend time with family, or do anything else in retirement, you need to make sure you have enough money saved. Those with enough savings and investments to afford a $10,000 monthly budget in retirement have plenty of options for where to spend their golden years.

If youre looking for places to retire on $10,000 a month, you can choose from beachfront towns, mountain destinations, big cities and nearly anywhere in between. Weve scoured the U. S. looking for tax-friendly destinations, comfortable climates and access to world-class recreation that could be a perfect fit for retirees. Heres a closer look at five of the best places to retire with $10,000 per month.

Have you ever caught yourself daydreaming about retirement and wondering if $10k monthly would give you the lifestyle you want? Your not alone! This question crosses the minds of so many people planning their golden years. Today, I’m gonna break down everything you need to know about retiring on $10,000 a month – is it enough, how much you’d need saved, and some real-talk about what retirement actually costs.

The Reality Check: What Does the Average Retiree Actually Spend?

Before we talk about whether $10,000 is enough, let’s take a look at how much most retirees spend now.

According to recent data from the Bureau of Labor Statistics households led by someone 65 or older spent an average of $64326 in 2023. That breaks down to about $5,360 per month. But here’s the kicker – most retirees spend WAY less than this amount!

A 2022 survey by the Employee Benefit Research Institute found that a whopping 68% of retirees between ages 62-75 spend less than $3,000 per month. Check out this breakdown:

| Monthly Spending | Percentage of Retirees |

|---|---|

| Less than $1,000 | 15% |

| $1,000 – $1,999 | 33% |

| $2,000 – $2,999 | 20% |

| $3,000 – $3,999 | 13% |

| $4,000 – $4,999 | 8% |

| $5,000 – $5,999 | 5% |

| $6,000 – $6,999 | 2% |

| $7,000 or more | 3% |

If you were to spend $10,000 a month in retirement, you would be in the top 10% of people who do that!

So How Much Do You Actually Need to Retire on $10K Monthly?

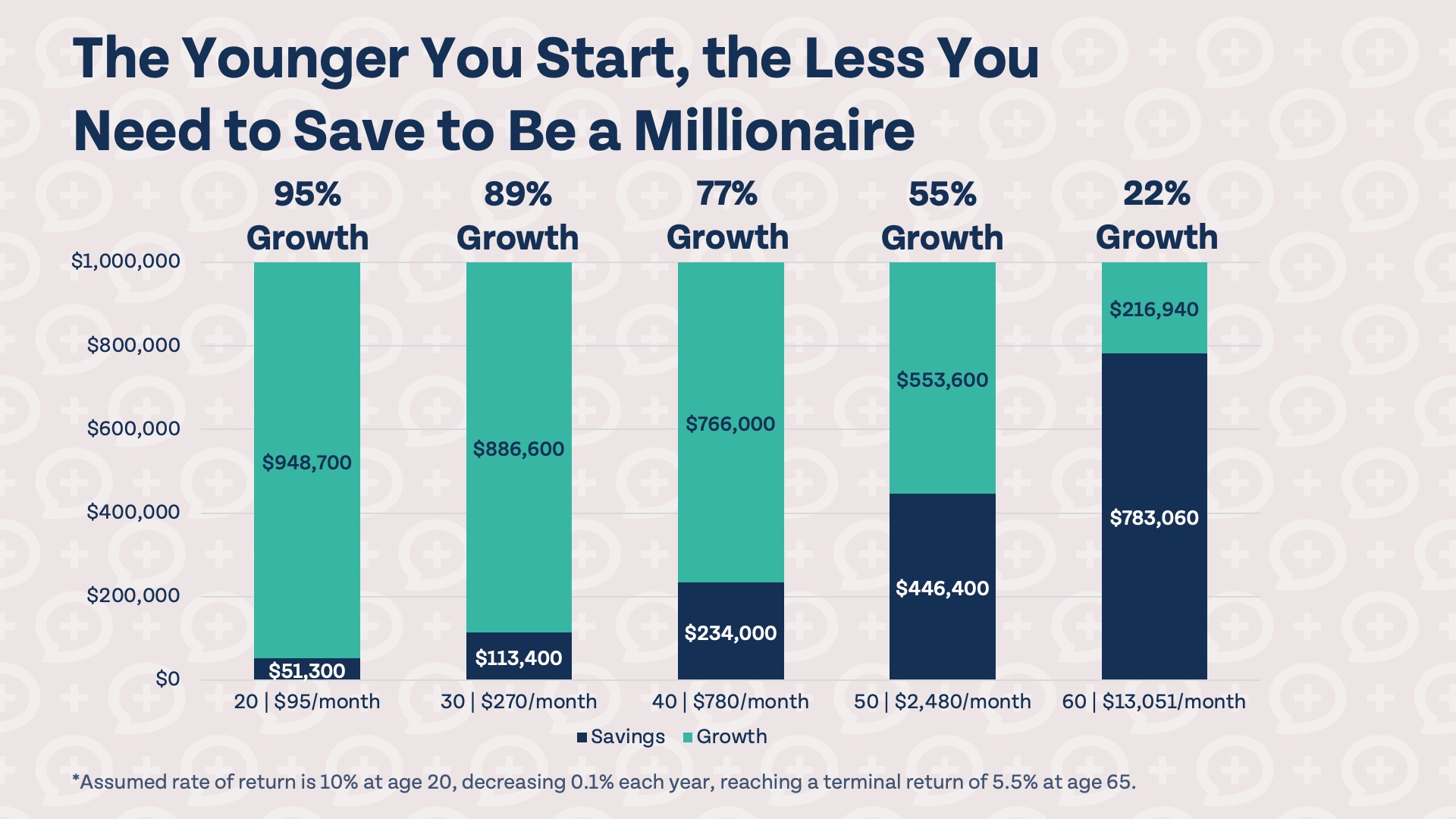

The classic answer financial advisors give starts with the 4% rule This rule suggests you can withdraw 4% of your portfolio each year and likely make it through a 30-year retirement without running outta money.

Let’s do some quick math:

- $10,000 per month = $120,000 per year after taxes

- Assuming you need to withdraw around $144,000 before taxes

- Using the 4% rule: $144,000 ÷ 0.04 = $3.6 million

So that’s our starting point – $3. 6 million. But wait! Don’t panic yet. This number can vary DRAMATICALLY based on three key factors.

Three Factors That Could Slash Your Magic Number by Millions

1. Other Income Sources You Have

This is huge. Any income that’s not coming from your investment portfolio reduces how much you need saved. Social Security is the big one for most people, but also consider:

- Pensions

- Rental income

- Annuities

- Part-time work

- Other passive income

Let’s say you and your spouse collect $3,700 combined monthly from Social Security (which is pretty close to average for higher earners). That’s $44,400 per year you DON’T need to pull from investments.

Recalculating our numbers, we’d need:

- $10,000 – $3,700 = $6,300 per month from investments

- $6,300 × 12 = $75,600 annually

- Adding taxes, let’s say you need to withdraw about $90,000

- $90,000 ÷ 0.04 = $2.25 million

That’s a $1.35 million difference just from Social Security! And we haven’t even factored in other potential income sources.

2. Account Types and Tax Efficiency

Where your money is stored matters almost as much as how much you have. Different accounts have completely different tax consequences:

- Traditional IRA/401(k): Withdrawals taxed as ordinary income

- Roth IRA/401(k): Tax-free withdrawals

- Taxable brokerage accounts: Capital gains tax rates (usually lower)

Let me give you a real example from a recent Monte Carlo simulation. If all of your $2.25 million was in a traditional IRA, you’d need to withdraw more to net $10k monthly after taxes. But if that same money was in a Roth IRA, you’d only need about $2.1 million for the same lifestyle – that’s a $150,000 savings!

The takeaway? Tax planning is CRITICAL. Having some tax diversification across different account types gives you more flexibility and potentially lowers the total amount you need saved.

3. Withdrawal Rate, Investment Strategy & How Long You’ll Live

This is where things get really personal. Your sustainable withdrawal rate depends on:

- How your money is invested (cash vs. stocks vs. bonds)

- Your retirement timeframe (retiring at 55 vs. 70 makes a huge difference)

- Your health and family history (planning for 20 vs. 30+ years)

If you don’t retire until age 65, but 70, your money doesn’t have to last as long. Additionally, this can lead to a higher withdrawal rate, possibly 5% or even 6% instead of 4%.

In one scenario we analyzed, pushing retirement from age 65 to 75 with a $2.1 million Roth portfolio raised the success probability from 70% to 95% – with the SAME portfolio size! Even more surprising, the analysis showed you could drop the portfolio to $1.6 million (when retiring at 75) and still maintain a 70% probability of success.

That’s a full $2 million less than our original $3.6 million estimate!

The Bottom Line: What’s Your Real Number?

When we pull all these factors together, the range is incredible:

- With no other income sources: $3.6M portfolio needed

- With average Social Security: $2.25M

- With optimal tax structure (Roth): $2.1M

- Retiring later (75) with Roth: $1.6M

That’s potentially $2 million in difference across reasonable scenarios – all while preserving the same $10k monthly lifestyle!

But Wait – Do You Even Need $10,000 Monthly?

Now let’s ask the question that might save you years of unnecessary work: do you actually need $10k per month?

As financial advisor Joe Conroy puts it: “You can have a great retirement on $5,000 a month, and you can have a great retirement on $50,000 a month.”

The classic rule of thumb is that you’ll need about 80% of your pre-retirement income during retirement. But that’s just a starting point – your actual needs could be higher or lower depending on:

- Where you live (huge cost differences between regions)

- Your healthcare needs

- Your hobbies and travel plans

- Whether your mortgage is paid off

- If you plan to help family members financially

Creating Your Personalized Retirement Spending Plan

Instead of focusing solely on that $10k number, I recommend building a retirement budget based on YOUR specific situation. Here’s a simple process:

-

Track your current spending for 3-6 months to establish a baseline

-

Adjust for retirement changes:

- Eliminate work-related expenses (commuting, work clothes, etc.)

- Reduce or eliminate mortgage payments (if applicable)

- Add new leisure activities and travel

- Increase healthcare estimates

- Factor in inflation (about 4% general, 6.5% for healthcare)

-

Consider your retirement phases:

- Early retirement (more active, higher spending on travel/hobbies)

- Mid retirement (settling into routines, often lower spending)

- Late retirement (potentially higher healthcare/assistance costs)

My Personal Take on the $10K Question

I think whether $10,000 monthly is enough really depends on YOU and your specific situation. For most Americans, it’s actually quite generous – remember that 68% of retirees spend less than $3,000 monthly!

But I also know several clients who spend more than $10k monthly and wouldn’t consider cutting back. It’s not about right or wrong – it’s about aligning your retirement vision with financial reality.

What I will say with confidence: many people overestimate what they need for a happy retirement. Studies consistently show that happiness in retirement correlates more strongly with health, relationships, and purpose than with luxury spending.

Final Thoughts: Planning Beyond the Numbers

While figuring out if $10k monthly is enough might seem like a pure numbers game, I encourage you to think beyond the math. Ask yourself:

- What activities truly bring me joy?

- Where do I want to live?

- Who do I want to spend time with?

- What legacy do I want to leave?

Your answers to these questions should shape your financial plan – not the other way around.

Retirement planning isn’t just about hitting a magical number. It’s about creating a life that feels meaningful and secure. For some, that might cost $5k monthly; for others, $15k. The key is designing a retirement that works for YOU.

For Urban Amenities: Chicago, Illinois

- Cost of living: 14% above the national average1

- Median home price: $681,8041

- Median monthly rent: $2,0801

- Metro population: 9,262,8252

- State taxes: No taxes on retirement income; 4. 95% on other income3.

Why retire in Denver?

The Mile High City is a top location for outdoor enthusiasts. During the warmer months, you can hike, bike, climb, raft and camp throughout the Front Range of the Rocky Mountains. In the winter, some of the worlds best ski resorts are just a short drive away. The Denver area is also home to excellent parks, museums, theaters and the famous Red Rocks Amphitheatre. Denver residents never run out of things to do.

Even though housing costs are higher than average and the cost of living is higher than the national average, it is still much cheaper than big cities on the East and West coasts. Social Security income isnt taxed once you reach age 65, and the flat 4. 4% tax rate for other income is reasonable compared to many other states. 3. Denver might be a good place to live when you retire if you’re looking for a new place to call home.

Need $10,000 Per Month in Retirement? Here’s How Much to Save.

FAQ

Is $10,000 a month good retirement?

Yes, $10,000 a month is a good, potentially even high, retirement income that allows for a comfortable lifestyle, but it requires significant savings, often in the range of $3. 6 million or more, to sustain according to the 4% rule.

What is a good monthly income to retire on?

There is a wide range of what makes a good monthly retirement income, but a common guideline is to keep your lifestyle at the same level of income you had before you retired. For 2025, U. S. Census Bureau data shows the average retirement income for an individual is about $5,000 per month, and for a couple, it is around $8,300 per month, though median incomes are lower.

How much does the average retired person get per month?

The average monthly income for U. S. A 2024 study by The Motley Fool using data from the U.S. found that the median monthly income for adults 65 and older is about $4,559 and the average monthly income is about $6,996. S. Census Bureau and Bureau of Labor Statistics. The median provides a more realistic view of typical retirement income because the average (mean) can be skewed by a small number of high earners.

Is $12000 a month good for retirement?

Quite an impressive retirement That number is very close to the median retirement income of $54,710 for Americans over 65, which comes from 2023 U.S. S. Census Bureau data. By contrast, aiming for $12,000 per month in retirement income means targeting nearly three times the income of the average retiree.

Can I retire on $10000 a month?

Typically you can generate at least $10,000 a month in retirement income for the rest of your life. This does not include Social Security Benefits. What is a good monthly income to retire on?

How much money do you need to retire on?

Typically you can generate at least $10,000 a month in retirement income for the rest of your life. This does not include Social Security Benefits. What is a good monthly income to retire on? Based on the 80% principle, you can expect to need about $96,000 in annual income after you retire, which is $8,000 per month.

How much money do you need to invest in retirement?

So if you wanted to spend $10,000 per month in retirement, it would mean you’ll need to have around $3 million invested. Though if you’re factoring Social Security payments and other regular income sources, this amount could be less.

What is a good retirement income?

“You can have a great retirement on $5,000 a month, and you can have a great retirement on $50,000 a month,” says Joe Conroy, financial advisor and owner of Harford Retirement Planners in Bel Air, Maryland. However, before you retire, understand what defines a good retirement income for you and where that money will come from.

Can you spend $10,000 a month without running out of money?

Spending $10,000 a month without running out of money during retirement may be possible for you with some careful calculations and saving strategies. As you try to work out how much you’ll need in savings to retire with the spending rate you want, gather information on all the sources of income you’ll have once you stop working.

How much money should a retiree spend in 2023?

Retirees can expect to spend 80% of their pre-retirement income in retirement, according to one rule of thumb. Older Americans spent an average of $64,326 in 2023, but 68% of retirees spend less than $40,000 per year. Social Security represents almost a third of the income received by people older than age 65. Deciding to retire is no small matter.