Knowing what your super balance should be for your age can help you get ready for retirement.

Check what your super balance should be now to retire comfortably. And see how your super savings compare to the average super balance by age.

Ever wondered if your retirement nest egg is big enough compared to other Aussies? You’re not alone! As a financial blogger who’s been researching this topic for years, I’ve discovered some pretty eye-opening facts about our nation’s super balances.

Let me tell you how much super the average Australian retiree has, whether that’s enough for a comfortable life, and what you can do if you’re behind (don’t worry, there’s still hope!)

The Retirement Reality Check: Average Super Balances

When I look at the latest data from the Australian Taxation Office (ATO), I can’t help but feel a bit concerned for many Aussies approaching retirement. Let’s get straight to the numbers:

For Australians aged 60-64 (those approaching retirement):

- Men: $402,838 average super balance

- Women: $318,203 average super balance

For those aged 65-69 (recently retired):

- Men: $453,075 average super balance

- Women: $403,038 average super balance

Pretty shocking, right? But here’s the real kicker…

The Gap Between What We Have and What We Need

According to the Association of Super Funds Australia (ASFA), to enjoy a “comfortable” retirement at age 67, you need:

- $690,000 for a couple

- $595,000 for a single person

These figures assume you:

- Own your home outright (no mortgage)

- Will receive a part-pension

- Take your super as a lump sum

When I compare these targets with the actual average balances, it’s clear that many Aussies are falling short – especially women, who face an even bigger super gap due to career breaks and the gender pay gap.

What Does “Comfortable” Retirement Actually Mean?

Perhaps you want to know what ASFA means by a “comfortable” retirement. Basically, it means you can:

- Participate in various recreational activities

- Buy household goods when needed

- Afford private health insurance

- Own a decent car

- Purchase good clothes and electronics

- Take occasional domestic and international trips

In dollar terms, ASFA estimates that to live comfortably, retirees aged 65-84 need:

- $75,319 per year for couples

- $53,289 per year for singles

That’s quite a bit more than just getting by on the basics!

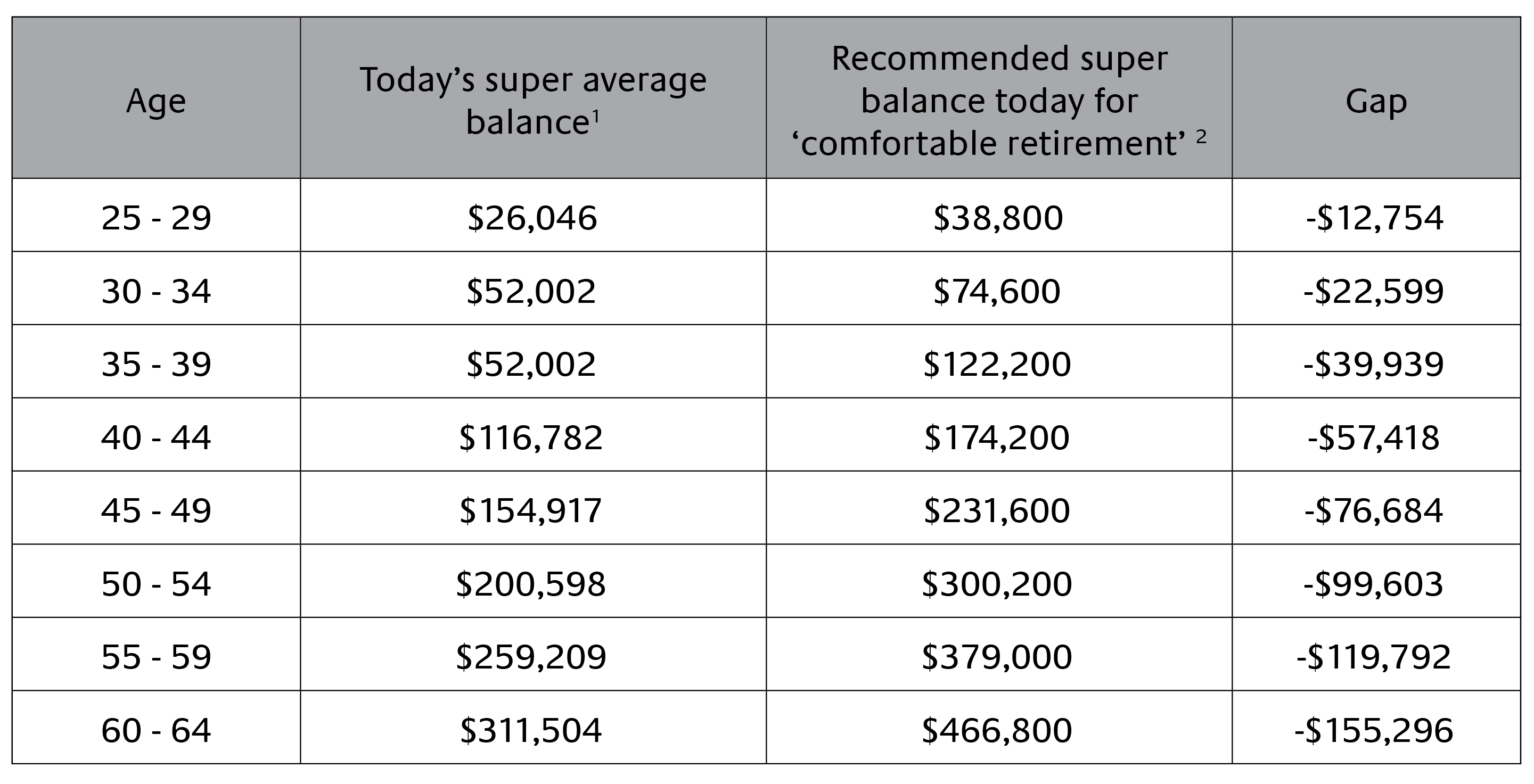

How Do Average Super Balances Change With Age?

This table, based on data from the ATO, shows the average amount of money in superannuation accounts for each age group:

| Age | Men’s Average Balance | Women’s Average Balance | Gap |

|---|---|---|---|

| 18-24 | $8,148 | $7,328 | $820 |

| 25-29 | $25,981 | $23,429 | $2,552 |

| 30-34 | $56,344 | $46,289 | $10,055 |

| 35-39 | $95,937 | $75,785 | $20,152 |

| 40-44 | $139,431 | $107,538 | $31,893 |

| 45-49 | $190,716 | $142,037 | $48,679 |

| 50-54 | $246,955 | $182,167 | $64,788 |

| 55-59 | $316,457 | $236,530 | $79,927 |

| 60-64 | $402,838 | $318,203 | $84,635 |

| 65-69 | $453,075 | $403,038 | $50,037 |

The fact that the gap gets bigger as we age until we get close to retirement is very scary. The pay gap between men and women between the ages of 60 and 64 is a huge $84,635. This is mostly because women take time off to care for others and there is still a pay gap between men and women, which according to the Workplace Gender Equality Agency is about 204.2 percent for pre-retirees.

Are You On Track? Super Balance Targets By Age

To help you figure out if you’re on track, here’s what your super balance should ideally be at different ages to reach that comfortable retirement goal:

| Age | Target Balance for Comfortable Retirement |

|---|---|

| 23 | $5,500 |

| 25 | $18,500 |

| 30 | $59,000 |

| 35 | $101,500 |

| 40 | $156,000 |

| 45 | $213,000 |

| 50 | $281,000 |

| 55 | $361,000 |

| 60 | $453,000 |

| 65 | $549,000 |

| 67 | $584,000 |

When I compare these targets with the actual averages, I can see many Aussies are falling behind. For example, the average 40-44 year old man has about $139,431 (vs target of $156,000), while women in the same age group have just $107,538 – a shortfall of nearly $50,000!

And this gap only gets bigger as we age.

Why Are Super Balances Lower Than They Should Be?

There are several reasons why your super balance might be lower than others in your age group:

- Your income level – Since super contributions are a percentage of your earnings, lower income means lower contributions

- Fund performance – Poor-performing super funds can significantly impact your balance over time

- Investment options – Being too conservative with your investments, especially when young

- Multiple accounts – Having super spread across multiple funds, each charging fees

- Career breaks – Time out of the workforce (especially for women raising children)

- The gender pay gap – Women earning less than men in equivalent roles

As financial adviser Kurt Ford explains, “Because your super guarantee is your super’s lifeblood of contributions, any change to your income will in turn affect your super balance over the long term.”

5 Ways to Boost Your Super Balance (It’s Not Too Late!)

If you’re panicking about your super balance, don’t worry! There are several things you can do to give it a boost:

-

Find and consolidate lost super – Check for forgotten accounts from previous jobs. You can do this through your myGov account linked to the ATO.

-

Make additional contributions – Consider salary sacrificing (pre-tax) or making after-tax contributions to your super.

-

Get your partner involved – Partners can boost each other’s super through splitting or spouse contributions.

-

Give your fund a health check – Review your insurance, fees, and investment options. As Kurt Ford suggests, ask yourself:

- Does your fund provide value for money?

- Are you invested in the right option for your age?

- Are you paying for appropriate insurance?

-

Check for government co-contributions – If you’re a low- or middle-income earner making personal after-tax contributions, the government may chip in up to $500.

The Super Guarantee is Increasing (Good News!)

One piece of good news is that employer super contributions are increasing. Currently, employers must pay 11% of an employee’s ordinary time earnings into super (if you’re over 18, or under 18 but working more than 30 hours a week).

And this is scheduled to increase to 12% on July 1, 2025. While this might not seem like much, over your working life, that extra 1% can add up to tens of thousands of dollars!

How Do I Check My Super Balance?

Checking your super balance is super easy:

- Log into your myGov account

- Click on Australian Taxation Office under linked services

- Tap the Menu button (three horizontal lines)

- Select Super from the drop-down menu

- Choose either Information or Manage options

You can also use the ATO’s tools to search for lost super, combine accounts, and compare super funds.

Final Thoughts: It’s Never Too Late!

I’ve been studying super for years, and one thing I know for sure is that it’s never too late to improve your retirement prospects. Even small changes now can make a big difference later.

As Rebekah Sarkoezy from Super Consumers Australia says, “If you’re looking to make voluntary contributions to top up your super balance, make sure to set aside an amount that you can easily afford because you won’t be able to access that money until retirement.”

Remember, every dollar you put into super now will compound over time. Even if you’re just a few years from retirement, boosting your contributions can still make a meaningful difference to your lifestyle in those golden years.

Have you checked your super balance lately? What strategies are you using to boost your retirement savings? Share your thoughts and experiences in the comments below!

If your balance is on track

Great work on having a solid super balance already. Of course, how much you should have depends on your personal goals. So, think about whether you need to add a little extra.

Keep in mind your yearly limit for super contributions.

Whether youre behind or ahead, a financial adviser can help you get more from your super. Your ART membership includes advice about your super account. 5.

How much super should I have at my age?

| Age (years) | Super balance |

|---|---|

| 25 | $26,000 |

| 30 | $66,500 |

| 35 | $111,500 |

| 40 | $168,000 |

| 45 | $226,000 |

| 50 | $296,000 |

| 55 | $377,000 |

| 60 | $469,000 |

| 65 | $571,000 |

Source: ASFAs Super Balance Detective, accessed May 2025.

How Much Super Do You Need To Retire in Australia? 7 Key Factors To Consider

FAQ

How much super does the average Australian retire with?

If you were born in 1964, the ASFA Super Guru website recommends a super balance of $469,000 at age 60 to allow for a comfortable lifestyle in retirement. The average super balance for Australians aged 60-64 was $402,838 for males and $318,293 for females, as at June 2021. How much super should you have as a couple?.

How long will $1,000,000 last in retirement in Australia?

$1 million is enough for a comfortable retirement if you retire at age 65. This will provide a single person with an income of $60,000 p. a. and a couple with $77,000 p. a. , including Age Pension for around 30 years, based on an investment return of 6% p. a. and 3. 0% p. a. inflation.

What is considered wealthy in retirement in Australia?

With that being said, what is a wealthy retirement? Well, according to ASFA, a comfortable retirement for a couple is around $72,000 per year and $51,000 for a single person. Taking this into account, I would think that a retirement income of, say, 30% more than these amounts would be a very wealthy retirement.

How much do I need to retire on $100,000 a year in Australia?

You need $2. 0M to retire on $100,000 per year in Australia if you retire at age 60; and $1. 7M to retire on $100,000 per year if you retire at age 65. These amounts will provide you with an income of $100,000 per year until age 95.