Its easy to feel like everyone has their financial act together—everyone, that is, except you. But the truth is that a lot of people worry about their money and wonder how they’re doing, especially when it comes to saving for retirement.

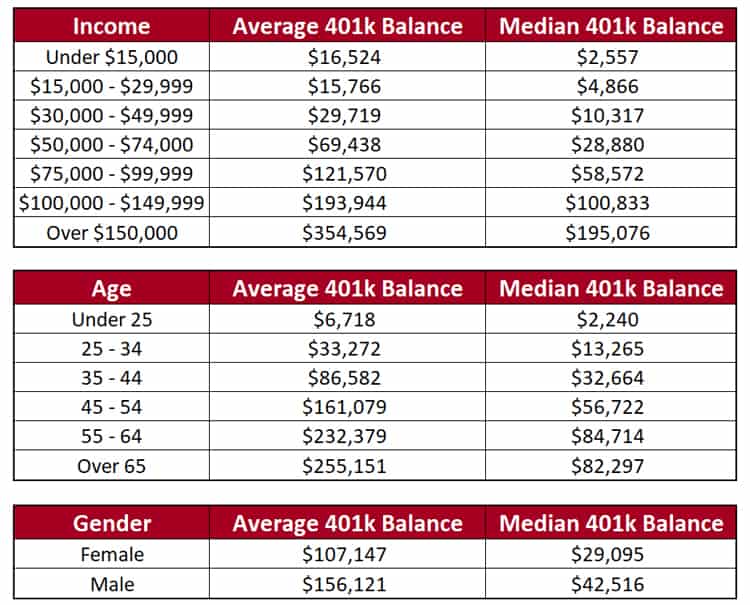

You might want to look at the average amount saved for retirement by age to see how you stack up against other people. That way, you can compare your retirement savings with people who have been working and saving for about the same amount of time as you. You’ll also want to check to see if you’re on track for retirement. Luckily, Fidelity has a simple rule that can help (more on that later).

If you’re approaching your mid-50s and wondering whether your retirement savings are on track, you’re not alone As someone who’s helped many clients navigate this exact concern, I can tell you that most Americans are curious about how their 401(k) stacks up against their peers.

But here’s the thing: what people have saved and what financial experts say they should save isn’t always the same. Let’s look at the numbers and see where you stand,

The Ideal 401(k) Balance at Age 55

The SmartAsset article talks about Fidelity’s retirement savings guidelines. According to them, you should have saved seven to eight times your annual salary in all of your retirement accounts by the time you turn 55.

Let’s put that into perspective:

- If you earn $100,000 annually, your target would be $700,000-$800,000

- If you earn $75,000, your target would be $525,000-$600,000

- If you earn $50,000, your target would be $350,000-$400,000

This recommendation is based on having enough money to maintain your current lifestyle throughout retirement.

The Reality: What People Actually Have Saved

However, real-world data tells a different story. Looking at the most recent information from three different sources:

According to Empower (August 2025 data):

- Average 401(k) balance for people in their 50s: $622,566

- Median 401(k) balance for people in their 50s: $251,758

According to Vanguard data (cited in SmartAsset):

- Average 401(k) balance for those aged 55 to 64: $244,750

- Median 401(k) balance for those aged 55 to 64: $87,571

According to USA Today/Empower (June 2025 data):

- Average 401(k) balance for people in their 50s: $568,040

It’s important to note the big difference between the average and median numbers. The average is inflated by a small group of people with very large balances, while the median (the middle number when all balances are arranged from lowest to highest) gives us a better idea of how much the average saver has saved.

Why Is There Such a Gap?

I’ve worked with enough clients to know there are several reasons why most people don’t reach the recommended savings targets:

-

Many people don’t start saving seriously until they are in their 30s or 40s, so they miss out on decades of growth that builds on itself.

-

Life happens: From raising kids to paying for college to medical emergencies, competing financial priorities often divert money from retirement accounts.

-

Income fluctuations: Career changes, layoffs, and periods of unemployment can interrupt consistent saving.

-

Market volatility: Downturns can temporarily reduce account balances, especially for those heavily invested in stocks.

-

Inconsistent contributions: Not everyone maxes out their 401(k) every year or takes full advantage of employer matching.

Is It Too Late If You’re Behind?

Absolutely not! At 55, you still have time to significantly improve your retirement outlook. Here are some powerful strategies I recommend to my clients:

1. Take Advantage of Catch-Up Contributions

Once you hit 50, the IRS allows you to contribute extra to your retirement accounts:

- In 2025, you can contribute up to $23,500 to your 401(k), plus an additional $7,500 in catch-up contributions, for a total of $31,000.

- You can also add an extra $1,000 to IRA contributions (for a total of $8,000 in 2025).

2. Run the Numbers

Let’s see how much impact maxing out your contributions could have:

If you’re 55 with $250,000 saved (around the median), and you:

- Contribute the maximum $31,000 annually

- Earn a 7% average annual return

- Continue until age 67 (12 years)

Your balance could grow to approximately $1.1 million! That’s the power of compound interest and consistent saving, even late in the game.

3. Rethink Your Timeline

If you’re significantly behind:

- Consider delaying retirement by a few years

- Look into partial retirement, where you work part-time

- Evaluate whether you could downsize your home or relocate to a lower-cost area

4. Optimize Your Investments

At 55, you still have 10-15 years before you’ll need to access most of your retirement funds. Make sure your asset allocation isn’t too conservative. Many people make the mistake of investing too cautiously too early.

Beyond the 401(k): A Holistic Approach

Remember that your 401(k) is just one piece of your retirement puzzle. When I work with clients, we always look at the complete picture:

-

Social Security benefits: These will likely provide a significant portion of your retirement income, though you shouldn’t rely solely on them.

-

Home equity: For many Americans, their home is their largest asset. Downsizing or using a reverse mortgage could supplement retirement income.

-

Other retirement accounts: IRAs, Roth IRAs, and taxable investment accounts all contribute to your retirement readiness.

-

Part-time work: Many “retirees” continue earning income through consulting, part-time work, or gig economy jobs.

-

Inheritance: While not guaranteed, potential inheritance could impact your planning.

What To Do Now If You’re 55

-

Get a clear picture of where you stand. Add up ALL your retirement assets, not just your 401(k).

-

Calculate your retirement needs. How much annual income will you need? The rule of thumb is 70-80% of your pre-retirement income.

-

Max out your contributions. Take full advantage of catch-up provisions.

-

Eliminate high-interest debt. It’s hard to build wealth while paying 20% interest on credit cards.

-

Consider working with a financial advisor. A professional can help you create a personalized plan that accounts for your unique situation.

The Bottom Line

While the benchmark of having 7-8 times your salary saved by age 55 is ideal, don’t panic if you’re not there yet. The median 401(k) balance for people in their 50s ranges from $87,571 to $251,758 (depending on which source you look at), which means half of Americans have less than that amount saved.

What matters most isn’t how you compare to others, but whether you’re taking action now to improve your personal situation. Every dollar you save today will work harder for you than dollars saved later.

I’ve seen clients transform their retirement outlook in their 50s with focused effort and smart strategies. With roughly a decade until traditional retirement age, you still have time to make meaningful progress.

Remember, the best time to start saving was 20 years ago. The second best time is today.

FAQ: Common Questions About 401(k) Savings at Age 55

Q: Is it too late to start saving for retirement at 55?

A: No! While you’ll need to be aggressive with your savings, you still have time to build a meaningful nest egg, especially with catch-up contributions.

Q: Should I prioritize paying off my mortgage or saving for retirement?

A: This depends on your mortgage interest rate and other factors, but generally at age 55, retirement savings should take priority if your mortgage rate is low.

Q: What if I can’t max out my 401(k) contributions?

A: Save as much as you can. Even increasing your contribution rate by 1-2% can make a significant difference over time.

Q: Should I be more conservative with my investments at 55?

A: Not necessarily. With potentially 30+ years of life ahead, you still need growth in your portfolio. Consider gradually becoming more conservative as you approach and enter retirement.

Q: What if Social Security isn’t enough to supplement my savings?

A: Develop multiple income streams for retirement, including part-time work, rental income, or delaying retirement to build more savings.

Remember, retirement planning isn’t one-size-fits-all. Your personal circumstances, health, family situation, and goals will all influence your ideal savings target. The most important thing is to have a plan and take consistent action toward it.

Average retirement savings by generation

Not surprisingly, older generations have saved more than the younger ones. Note that the average savings rate overall is 14. 1%, which is close to 15%, the amount that Fidelity suggests saving to maintain your lifestyle in retirement (it includes any match from your employer).

| Average 401(k) balance | Employee contribution | Employer contribution | Contributing to a Roth 401(k) | Investing 100% in target date fund | Loan outstanding | Average IRA balance | |

|---|---|---|---|---|---|---|---|

| Baby boomers | $249,300 | 11.9% | 5.0% | 12.2% | 44.2% | 14.5% | $257,002 |

| Gen X | $192,300 | 10.2% | 5.0% | 14.5% | 54.0% | 25.3% | $103,952 |

| Millennials | $67,300 | 8.7% | 4.6% | 18.3% | 70.1% | 18.4% | $25,109 |

| Gen Z | $13,500 | 7.2% | 3.7% | 18.2% | 81.5% | 6.7% | $6,672 |

Note: TDF stands for target date fund. Source: Fidelity Investments Q4 2024. 401(k) data based on 26,700 corporate defined contribution plans and 24. 5 million participants as of December 31, 2024. These figures include the advisor-sold market but exclude the tax-exempt market. Excluded from the behavioral statistics are nonqualified defined contribution plans and plans for Fidelitys own employees.

Generations as defined by Pew Research: Baby boomers are individuals born between 1946 and 1964, Gen X are individuals born between 1965 and 1980, millennials include individuals born between 1981 and 1996, and Gen Z includes individuals born between 1997 and 2012. Fidelity business analysis of 16. 8 million IRA accounts as of December 31, 2024. Considers only active participants with balance.

The power of consistently investing for retirement

Another way to measure how you are doing is to look at data for people who have been contributing to their workplace retirement plan for years and years. Being in the same plan with the same employer may provide some stability and routine, which may be helpful for saving over a long period of time.

Fidelity Investments Q4 2024 401(k) data based on 26,700 corporate defined contribution plans and 24. 5 million participants as of December 31, 2024. These figures include the advisor-sold market but exclude the tax-exempt market. Excluded from the behavioral statistics are nonqualified defined contribution plans and plans for Fidelitys own employees. Generations as defined by Pew Research: Baby boomers are individuals born between 1946 and 1964, Gen X are individuals born between 1965 and 1980, millennials include individuals born between 1981 and 1996, and Gen Z includes individuals born between 1997 and 2012.

To avoid a savings setback when changing jobs, try to ensure that youre able to save at least as much as you were saving at your previous job. If you cant swing it right away, make an appointment with yourself to check your retirement savings rate again in a few months.