Over the last decade, the “financial independence, retire early” (FIRE) movement has become one of the hottest mantras for those under 60. 1 But the truth is that if you want to leave the workforce in the prime of your life, you’ll need to make even bigger investments and cut costs even more than you think.

Are you dreaming of kissing your 9-to-5 goodbye while you’re still young enough to truly enjoy freedom? You’re not alone! The FIRE movement (Financial Independence, Retire Early) has exploded in popularity, and retiring at 40 is the ultimate goal for many of us ambitious planners.

But let’s get real – early retirement requires some serious money. Today, I’m breaking down exactly how much cash you’ll need to stash away to make this dream your reality.

The Magic Number: How Much You Actually Need

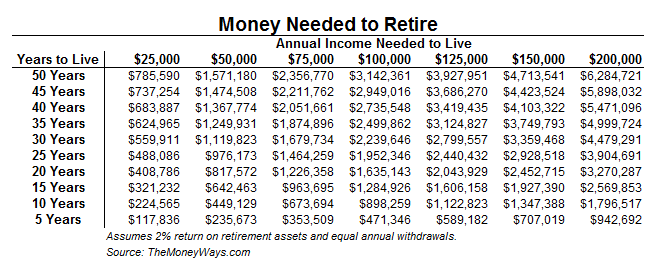

Alright, let’s cut to the chase. According to the latest data from 2025, if you want to retire at 40 and live on about $50,000 per year, you’ll need approximately $1.25 million in your retirement accounts.

But wait – that’s just the starting point. Many financial experts suggest you might need closer to $2. 5 million dollars if you want to live in comfort or in a pricey area.

Why such a big difference? Well, it all comes down to the famous 4% rule.

Understanding the 4% Rule for Early Retirement

The 4% rule is basically the holy grail of retirement planning. Here’s how it works:

- You withdraw 4% of your total savings in your first year of retirement

- You adjust that amount for inflation each following year

- Your money should theoretically last at least 30 years

So if you’ve saved $1.25 million and follow the 4% rule, you’d withdraw $50,000 in your first year of retirement. If inflation is 2% the next year, you’d withdraw $51,000, and so on.

But here’s the catch – traditional retirement usually starts at 65, meaning those funds need to last about 30 years. If you retire at 40, your money needs to stretch for potentially 50+ years! That’s why some financial advisors recommend using a more conservative 3-3.5% withdrawal rate for early retirees.

Using a 3.5% withdrawal rate, you’d need about $1.43 million to generate that same $50,000 annual income. At a 3% rate, you’re looking at $1.67 million.

What Your Expenses Actually Look Like at 40

One big mistake I see people make is underestimating what their expenses will be in retirement. When I first started planning, I thought I’d need way less money than I actually do!

Here’s what you should include in your retirement budget:

- Housing: Mortgage/rent, property taxes, insurance, maintenance

- Healthcare: A MAJOR expense when you retire early (more on this below)

- Transportation: Car payments, maintenance, gas, public transit

- Food & groceries: Don’t forget inflation makes these costs rise yearly

- Utilities: Electric, water, internet, phone, streaming services

- Childcare/education: If you have kids or plan to in the future

- Entertainment & travel: You’re retiring early to enjoy life, right?

- Taxes: Yes, you’ll still pay these in retirement!

I was shocked to find that my “retirement” budget wasn’t that much less than my working budget when I added it all up. In fact, some categories, like travel and health care, had much higher scores!

The Healthcare Conundrum

This is the part nobody talks about enough! When you retire at 40, you won’t qualify for Medicare for another 25 years. That means you’ll need to cover health insurance completely on your own.

According to 2025 data, a 40-year-old can expect to pay at least $500 per month per person for private health insurance – that’s $6,000 per year minimum, and often much more. Plus, these plans typically come with deductibles between $2,000 and $7,500 annually.

For a couple, we’re talking $12,000+ in premiums alone each year, not including actual healthcare costs. Over 25 years until Medicare eligibility, that’s a minimum of $300,000 just for insurance premiums!

This is why so many early retirement plans fail – they don’t adequately account for healthcare costs.

Sample Calculation: How Much You Need to Save

Let’s break this down with some real numbers. Say you’re 25 years old now and want to retire at 40:

- You need $1.25 million by age 40 (using the 4% rule)

- You have 15 years to save this amount

- You expect a 7% average annual return on your investments

How much would you need to save monthly? About $3,000 per month or $36,000 per year!

Here’s a table showing different target amounts and what you’d need to save monthly:

| Retirement Fund Target | Monthly Savings Needed (15-year timeline) |

|---|---|

| $1.25 million (4% rule) | $3,000 |

| $1.67 million (3% rule) | $4,000 |

| $2.5 million (comfort cushion) | $6,000 |

These numbers assume a consistent 7% return with no market volatility, which isn’t realistic – the real world has ups and downs. You might need to save even more to account for market fluctuations.

No Social Security Safety Net

Here’s another reality check – if you retire at 40, you won’t have access to Social Security benefits until much later. Social Security is designed to replace about 40% of your pre-retirement income, but only if you’ve contributed to it through payroll taxes for many years.

By retiring early, you’ll not only have to wait until your 60s to collect, but your benefit amount will likely be lower because you contributed for fewer years. This means your investment portfolio needs to carry more weight!

The FIRE Approach: Making It Possible

So, is retiring at 40 just a pipe dream? Not always! The FIRE movement suggests two main ways to make it happen:

- Extreme saving: Save 50-70% of your income during your working years

- Significantly reduced expenses: Live well below your means both before and during retirement

Many successful early retirees combine traditional retirement accounts (401(k)s, IRAs) with taxable brokerage accounts. Since you can’t access most retirement accounts without penalties until age 59½, you’ll need accessible funds to bridge that gap.

Real Talk: Is Retiring at 40 Realistic for You?

I’ll be honest – retiring at 40 isn’t for everyone. It requires:

- A high income during your working years

- Extreme discipline with spending and saving

- Willingness to live frugally for decades

- Careful planning for healthcare costs

- Flexibility to adjust if market conditions change

For many of us, a modified approach might be more realistic. This could mean:

- Semi-retirement at 40 (working part-time)

- Changing to a lower-paying but more fulfilling career

- Taking a sabbatical for a few years, then returning to work

- Working until 50 instead of 40

My Personal Take: Finding Balance

When I first heard about the FIRE movement, I was crazy about the idea of retiring at age 40. To reach that goal, I spent less, invested more, and pretty much put my whole life on hold.

But along the way, I realized something important – the point of retiring early is to enjoy life more, not less. If you’re miserable for 15 years just to retire early, you might be missing the point.

Now I’m aiming for a more balanced approach – saving aggressively but still enjoying my journey. Maybe I’ll retire at 45 or 50 instead of 40, but I’ll have enjoyed the ride much more.

Action Steps: Start Your Early Retirement Journey

If you’re serious about retiring at 40, here’s how to get started:

- Calculate your target number: Use the 4% rule as a starting point, but consider a more conservative 3-3.5% withdrawal rate

- Max out tax-advantaged accounts: Contribute the maximum to 401(k)s, IRAs, and HSAs

- Open taxable investment accounts: You’ll need these to access funds before age 59½

- Slash your expenses: Housing and transportation typically offer the biggest savings opportunities

- Increase your income: Consider side hustles, job changes, or additional education to boost earnings

- Research healthcare options: This will be your biggest expense before Medicare eligibility

- Build flexibility into your plan: Consider part-time work or passive income streams in retirement

Final Thoughts: Is It Worth It?

Retiring at 40 requires significant sacrifice and planning. For some, it’s absolutely worth it. For others, a more moderate approach provides better life balance.

The most important thing is to start planning early. Even if you don’t reach your goal of retiring at 40, you’ll be in a much stronger financial position than most of your peers.

Remember, retiring early isn’t just about having enough money – it’s about creating a life you don’t need to retire from. Sometimes the best approach isn’t retiring completely, but rather finding work you genuinely enjoy that gives you the freedom and flexibility you crave.

What do you think? Is retiring at 40 one of your goals, or are you aiming for something different? I’d love to hear your thoughts and plans in the comments below!

Note: This article was last updated on October 3, 2025, with the most current retirement planning data available. Everyone’s situation is unique, so consider consulting with a financial advisor before making major retirement decisions.

How Will You Cover Health Care Needs?

And that doesnt even cover one of the biggest spending categories for any retiree: health care. Those who retire at an age when most people are considered “mid-career” face something of a conundrum. Theyre far too young for Medicares relatively low premiums and unable to get subsidized care through an employer.

It certainly helps if youre eligible for coverage on a spouses plan, as going it alone can be an expensive undertaking. According to the Kaiser Family Foundation, the average 40-year-old enrolled in a private plan might spend $342 a month for the least-expensive option in 2023, and they would potentially have to pay $472 to stay on the most-expensive plan. 3.

Needless to say, those rates can climb quickly if you have to add kids or a spouse to the plan. And they could rise even further as you get older.

How Much You Need to Budget to Retire at 40

If youre looking for a quick answer, the amount is a lot. Extremely early retirements can be a tricky proposition — youre giving yourself fewer years to build up a reserve of savings and leaving yourself with more years to live off those funds.

The more optimistic FIRE adherents assume that a 4% withdrawal rate from savings, adjusted annually for inflation, will leave them with enough funds for a prolonged retirement (assuming at least half their money is invested in stocks). 2 That means theyd be able to quit their full-time job once theyve saved 25 times their yearly wages. In a low-interest-rate environment, some suggest even greater reserves.

In retirement, you might not need as much money because you won’t have to drive to work every day and won’t have to pay for other things that come with working full-time. But in a lot of cases, your current spending levels are a pretty good starting point for estimating what your post-work budget is going to look like.

Here are the future expenses youll want to consider:

- Housing costs

- Car payments and fuel costs

- Grocery bills

- Utilities

- Student loans and other debt

- Child care costs and college savings, if applicable

- Entertainment and travel expenses

Use your current spending to forecast your needs in retirement. Start Your Free Plan

I Want To Retire At 40 So I Don’t Have To Work

FAQ

Can I retire with $2 million at 40?

Yes, it’s possible to retire at 40 with $2 million, but it requires careful planning, disciplined spending, and a robust investment strategy to account for a longer retirement period, potential healthcare costs, and inflation.

Is $5 million enough to retire at 40?

Yes, $5 million is generally considered a substantial amount that can support retirement at age 40, with a conservative annual withdrawal of around $200,000, but it requires careful financial planning and a conservative lifestyle.

Can I retire at 40 with 1 million dollars?

You might be able to retire at age 40 if you have $1 million, but you need to carefully plan your retirement, be disciplined with your investments, and have a good idea of how much your costs will be, including healthcare and inflation. Your ability to do so depends on factors like your lifestyle and living costs, your chosen investment strategy and withdrawal rate, and your willingness to manage risks like market downturns.

Is $100,000 in retirement at 40 good?

It’s a good sign if you have $100,000 in your 401(k) by the time you’re in your late 30s or early 40s, especially if you make regular contributions and take advantage of employer matches. Starting early and maximizing contributions can significantly impact your retirement savings over time due to compound growth.

How much money do you need to retire at 40?

The amount needed to retire at 40 depends on your spending habits, investment returns and life expectancy. A common approach is to use the 4% rule, which suggests that retirees can withdraw 4% of their savings annually to maintain financial security.

Can you afford retirement in your 40s?

To afford retirement in your 40s and beyond, most people will need to be resourceful and creative to spend the least amount of money to meet their needs and still be happy with their life. If you can really manage to retire at age 40, you won’t be earning much income from Social Security once you begin drawing benefits in your 60s.

How much money do you need to retire comfortably?

What savers think they need to retire comfortably is all over the place. But the magic number is typically north of $1 million, according to industry studies. A study by Schroders says savers think they need $1. 2 million socked away. A Northwestern Mutual study ups the ante to $1. 46 million.

How much money do you need for early retirement?

Upon retirement at age 40, you’ll need enough money to draw down 4% to 5% annually. That’s the cash you’ll have to live on throughout your retirement. Gilmore said, “There’s a simple equation you can use to see if you’re even close to meeting your goal of retiring early.” “Take your living expenses for the year and multiply by 25.

What happens if you retire at 40?

Retiring at 40 also leaves you without access to Social Security or Medicare for 22 to 25 years into retirement, leaving you with one less source of retirement income and one more bill to foot. And when you do reach full retirement age, your Social Security benefit will be reduced due to your lower average earnings.

How much should you save for retirement?

Some experts claim that savings of 15 to 25 times of a person’s current annual income are enough to last them throughout their retirement. Of course, there are other ways to determine how much to save for retirement. The calculations here can be helpful, as can many other retirement calculators out there.