You’re not the only one worried about your retirement. Many companies are having trouble keeping their pension promises, so it’s important to know if your pension plan is underfunded for your financial future.

I’ve spent countless hours researching this topic, and I’m here to share everything you need to know about identifying underfunded pension plans. This knowledge could literally save your retirement!

What Is an Underfunded Pension Plan?

An underfunded pension plan is pretty straightforward—it’s a company-sponsored retirement plan that has more liabilities than assets. In plain English, this means the plan doesn’t have enough money to pay all the benefits it has promised to current and former employees.

This is a risky situation because promises to pay pensions to current and former employees are often legally binding. There’s no guarantee that future retirees will get the benefits they were promised or that current retirees will continue to get their set payments if the plan doesn’t have enough money in it.

Key Signs of an Underfunded Pension Plan

Determining if a pension plan is underfunded isn’t always straightforward, but here are some clear indicators:

- The funded ratio is below 100% – This ratio compares assets to liabilities

- Disclosures in company financial statements – Required to be reported in annual reports

- Increased employer contributions – Companies trying to make up shortfalls

- Plan freezes or benefit reductions – May signal funding problems

- PBGC involvement – Intervention by the Pension Benefit Guaranty Corporation

How to Check Your Pension Plan’s Funding Status

Review the Funded Status

The simplest way to determine if a pension plan is underfunded is to check its funded ratio. This compares the plan’s assets to its liabilities:

- Funded Ratio = Plan Assets ÷ Plan Liabilities

- A ratio below 100% indicates underfunding

- The lower the percentage, the more severe the underfunding

For example, if a plan has $800 million in assets but $1 billion in debt, its funded percentage ratio would be 80%, which means it’s not enough money by 2020.

Examine Financial Statements

Companies are required to disclose pension information in their annual financial statements. Here’s what to look for:

- Check the company’s 10-K annual financial statement

- Look for the footnotes section which contains pension disclosures

- Compare the “fair value of plan assets” to the “accumulated benefit obligation”

- If assets are less than obligations, there’s a pension shortfall

You may have to look a little further, but this information is available to the public for all companies that are traded on the stock market.

Check Annual Reports and Form 5500

Pension plans must file Form 5500 with the IRS and Department of Labor. These documents contain detailed information about the plan’s financial status:

- Request a copy of Form 5500 from your plan administrator

- Look at Schedule B or SB for defined benefit plans

- Check the funding target attainment percentage (FTAP)

- Plans with FTAP less than 80% are considered “at risk” for underfunding

Ask for Actuarial Valuations

Actuaries regularly evaluate pension plans to determine their funding status:

- Request actuarial reports from your plan administrator

- Review the assumptions used (investment returns, life expectancy, etc.)

- Overly optimistic assumptions might mask underfunding

- Look for recent changes in assumptions that suddenly “improve” funding status

Underfunded vs. Overfunded Pensions

To better understand underfunding, it helps to contrast it with overfunding:

| Characteristic | Underfunded Pension | Overfunded Pension |

|---|---|---|

| Assets vs. Liabilities | Assets < Liabilities | Assets > Liabilities |

| Risk to Retirees | Higher risk of reduced benefits | Lower risk to benefits |

| Employer Action | May require increased contributions | May allow reduced contributions |

| Regulatory Concern | Higher scrutiny | Lower concern |

| Disclosure Requirements | More extensive | Less extensive |

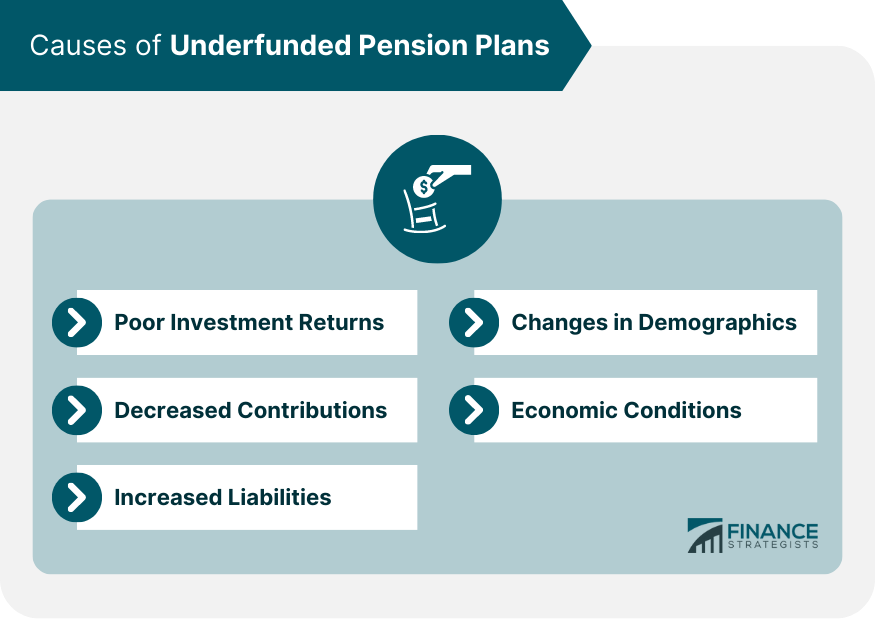

Common Causes of Pension Underfunding

Understanding why pensions become underfunded can help you assess your own plan’s risk factors:

• Investment losses: Market downturns can significantly reduce pension assets

• Interest rate changes: Lower rates increase the present value of future liabilities

• Inadequate employer contributions: Companies may not contribute enough

• Aging workforce: More retirees drawing benefits than active workers contributing

• Overly optimistic assumptions: Using unrealistic expectations for investment returns

• Economic downturns: Reduced company profits limiting ability to fund pensions

Many companies used overly optimistic assumptions during good economic times, only to face reality during downturns. For example, a company might assume a long-term investment return of 13%, when 10% or less is more realistic.

What Happens When a Pension Plan Is Underfunded?

If your pension plan is underfunded, several things might happen:

- Increased employer contributions: The company may need to put more money into the plan

- Benefit freezes: The company might stop offering new benefits or freeze existing ones

- Plan restructuring: Benefits may be recalculated or payment options changed

- PBGC intervention: In severe cases, the government’s pension insurer may step in

- Reduced benefits: In extreme cases, benefits might be reduced (though there are legal protections)

It’s important to note that just because a plan is underfunded doesn’t mean it will fail. Many underfunded plans continue to pay benefits as promised while working toward better funding.

What to Do If Your Pension Plan Is Underfunded

If you discover your pension plan is underfunded, don’t panic! Here are some steps you can take:

Monitor Plan Updates

Stay informed about changes to your plan’s funding status:

- Read all communications from your employer or plan administrator

- Attend any informational meetings about the pension plan

- Join employee advocacy groups focused on retirement benefits

Understand PBGC Coverage

The Pension Benefit Guaranty Corporation provides insurance for many private-sector pension plans:

- Check if your plan is covered by the PBGC

- Understand the maximum benefit guarantees (which may be less than your full pension)

- Keep track of PBGC announcements related to your industry or employer

Diversify Your Retirement Savings

Don’t put all your eggs in one basket:

- Increase contributions to other retirement accounts like IRAs or 401(k)s

- Consider additional personal savings for retirement

- Explore other income sources for retirement (part-time work, rental income, etc.)

Consult a Financial Advisor

Get professional help to assess your situation:

- A financial advisor can help evaluate your specific risk

- They can suggest strategies to mitigate potential pension shortfalls

- They can help rebalance your overall retirement plan

Real-World Example of Checking for Underfunding

Let me walk you through a simple example:

- I requested my company’s latest annual report

- In the financial statement footnotes, I found:

- Pension assets: $850 million

- Pension obligations: $1.1 billion

- Calculating the funded ratio: $850 million ÷ $1.1 billion = 77%

- Conclusion: The plan is underfunded by 23%

I also noticed that the company had increased its contributions over the past three years, which confirmed they were trying to address the shortfall.

The Regulatory Framework

Understanding the regulatory environment can help you determine if your pension is at risk:

- The Employee Retirement Income Security Act (ERISA) sets minimum funding standards

- The Pension Protection Act of 2006 strengthened funding requirements

- A plan is considered “at risk” if its funding target attainment percentage is less than 80%

- Plans below 60% funded face severe restrictions on lump-sum payments and benefit increases

Determining if your pension plan is underfunded isn’t just an academic exercise—it’s essential for your financial security. By checking the funded ratio, reviewing financial statements, examining Form 5500, and understanding actuarial assumptions, you can get a clear picture of your pension’s health.

Remember, an underfunded plan doesn’t automatically mean you’ll lose benefits, but it’s a warning sign that shouldn’t be ignored. The best approach is to stay informed and diversify your retirement savings so you’re not entirely dependent on any single source of retirement income.

Have you checked your pension plan’s funding status? What steps are you taking to ensure your retirement security? I’d love to hear your thoughts and experiences in the comments below!

FAQs About Underfunded Pension Plans

Q: Can an underfunded pension plan recover?

A: Yes, with increased employer contributions, strong investment returns, and careful management, underfunded plans can improve their financial position over time.

Q: Will I lose my pension if my plan is underfunded?

A: Not necessarily. Many protections exist, including PBGC insurance for private-sector plans. However, in extreme cases, benefits might be reduced.

Q: How often should I check my pension plan’s funding status?

A: At minimum, review it annually when new financial statements are released, or whenever major company changes occur.

Q: Can employees contribute more to help fund an underfunded pension?

A: This depends on your specific plan’s rules. Some plans allow for additional employee contributions, while others don’t.

Q: What’s the difference between an underfunded and an unfunded pension plan?

A: An underfunded plan has some assets, but not enough to cover all obligations. An unfunded plan is a pay-as-you-go system that uses the employer’s current income to fund pension payments.