Theres not a one-size-fits-all solution for the number of credit cards a person should own. However, its generally a good idea to have two or three active credit card accounts, in addition to other types of credit such as student loans, an auto loan or a mortgage.

Just remember: The number of credit cards you own is less important than how you use them. Be sure that you can keep up with your existing monthly payments before considering a new credit card.

Hey there, fam! Ever wondered if stacking up a bunch of credit cards in your wallet is gonna boost that credit score of yours? Well, I’m here to spill the tea The quick answer? Yeah, having more credit cards can increase your credit score, but only if you play your cards right (pun totally intended) It ain’t a magic trick—it’s all about how you manage ‘em. Stick with me as I break this down into bite-sized pieces, share some real-talk advice, and maybe even throw in a story or two from my own messy financial journey.

The Big Picture: Can More Cards Really Help?

Let’s get straight to the point. Having more credit cards can help your credit score in a couple of key ways, mainly by lowering your credit utilization rate and diversifying your credit mix. But, and this is a big ol’ but, it can also backfire if you’re not careful. Miss a payment or rack up debt, and you’re in for a world of hurt. So, before you go applying for every shiny card offer in your inbox, let’s dig into how this actually works.

Your credit score—think of it as your financial report card—is based on a few major factors We’re talking payment history, credit utilization, length of credit history, types of credit, and new credit inquiries More cards can play a role in a few of these areas, but they gotta be handled with care. Here’s the deal, straight from my own hard-learned lessons.

How Credit Scores Work (In Plain English)

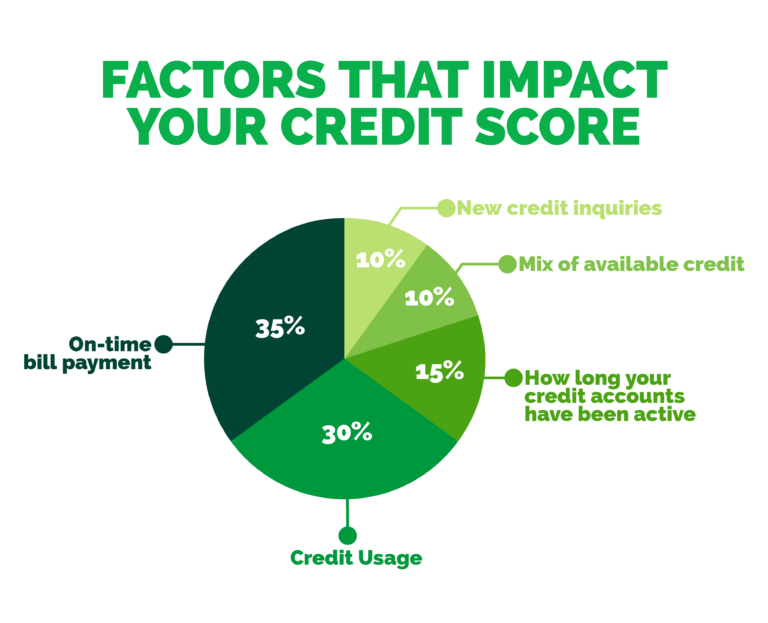

Before we dive into the nitty-gritty of multiple credit cards, let’s make sure we’re on the same page about what a credit score even is. It’s a number, usually between 300 and 850, that tells lenders how risky it is to let you borrow money Higher is better, obviously The big dogs like FICO and VantageScore calculate it based on stuff like

- Payment History (35%): Do you pay your bills on time? Late payments are a huge no-no and can tank your score faster than you can say “overdraft fee.”

- Credit Utilization (30%): This is how much of your available credit you’re using. Keep it low, like under 30%, and you’re golden.

- Length of Credit History (15%): How long you’ve had credit accounts open. Older accounts help show you’re not a newbie.

- Credit Mix (10%): Having different types of credit—like cards, loans, or a mortgage—shows you can juggle different debts.

- New Credit (10%): Applying for new accounts can ding your score temporarily ‘cause it looks like you might be desperate for cash.

Now, where do more credit cards fit into this puzzle? Mainly in utilization and mix, but they can mess with new credit inquiries too. Let’s break that down next.

How More Credit Cards Can Boost Your Score

Alright, here’s the good stuff—why having more than one or two cards might actually be a smart move for your score. I’ve been there, juggling a couple of cards, and lemme tell ya, it can work if you’re strategic.

- Lower Credit Utilization Rate: This is the biggie. Say you’ve got one card with a $1,000 limit and you’re spending $400 a month. That’s 40% utilization, which ain’t great—lenders wanna see under 30%. Now, add a second card with another $1,000 limit. Your total limit is $2,000, and if you’re still spending $400, your utilization drops to 20%. Boom, that’s better for your score! More cards mean more available credit, so you’re less likely to look maxed out.

- Better Credit Mix: If you’ve only got one card and no other loans, your credit mix is pretty boring. Adding another card or two, especially if they’re different types (like a rewards card versus a basic one), can show lenders you’re versatile. Pair that with a car loan or something, and you’re lookin’ diverse, which they love.

- Access to Rewards: Okay, this don’t directly boost your score, but hear me out. More cards often mean more perks—cashback, travel points, whatever. If you’re using these cards smartly and paying ‘em off, you’re building good habits while getting a lil’ somethin’ extra. I got a card just for gas rewards, and it’s saved me a ton while helping my credit game.

So, yeah, more cards can help. But don’t go wild just yet. There’s a flip side, and it’s a doozy.

The Risks of Piling Up Credit Cards

I ain’t gonna sugarcoat it—having a bunch of credit cards can bite you in the backside if you’re not careful. Me and my pal, we done learned the hard way a few years back when we thought more cards equaled more “freedom.” Nah, it equaled more headaches. Here’s what can go wrong:

- Overspending Temptation: More cards mean more limits, and it’s real easy to think, “Oh, I’ll just put this on the new card.” Next thing you know, you’ve got balances on three cards you can’t pay off. High balances jack up your utilization rate and hurt your score, not to mention the interest fees. Yikes!

- Missing Payments: Juggling due dates for two cards is one thing, but five? Forget about it. Each card got its own date, interest rate, minimum payment—keeping track is a nightmare. Miss a payment, and your payment history takes a hit. That’s 35% of your score right there, folks.

- Hard Inquiries Ding: Every time you apply for a new card, the lender checks your credit. That’s called a hard inquiry, and it can drop your score a few points for a short time. One or two ain’t bad, but if you’re applying for cards left and right, it looks like you’re in financial trouble. Lenders don’t like that vibe.

- Too Many Cards, Too Much Hassle: Honestly, managing more than a couple cards can just be a pain. Different terms, fees, rewards programs—it’s a lot. If you’re not organized, you’re setting yourself up for late fees and stress.

So, while more cards can help, they can also mess you up big time if you ain’t got a handle on your spending or organization. Let’s talk about finding that sweet spot.

How Many Credit Cards Should You Have?

Here’s the million-dollar question: what’s the right number of cards? Well, there ain’t a one-size-fits-all answer, but most financial gurus (and my own experience) suggest sticking to 2-3 active credit cards. Why? It’s enough to get the benefits—like lower utilization and a decent mix—without overwhelming you with payments and due dates.

If you’ve already got 2-3 cards and you’re managing ‘em fine—paying on time, keeping balances low—there’s probably no need to get more just for the sake of your score. But if you’ve only got one, adding another could help, especially if your utilization is high. Just make sure you’re ready for the responsibility. Ask yourself:

- Can I keep track of another payment date?

- Will I be tempted to spend more than I can pay off?

- Do I really need another card, or am I just chasing rewards?

If the answers are “yes, no, yes,” then go for it. Otherwise, hold off.

Tips for Managing Multiple Credit Cards Like a Pro

Alright, if you’re set on having more cards or already got a few, let’s make sure you don’t crash and burn. Here’s some straight-up advice from yours truly on handling multiple cards without losing your mind:

- Set Up Auto-Payments: Most banks let you automate payments so you never miss a due date. I’ve got mine set to pay the full balance every month—saves me the headache of remembering. If you can’t pay in full, at least set it to cover the minimum so you avoid late fees.

- Track Spending with Apps: Use a budgeting app or even just a spreadsheet to see what you’re spending on each card. I use a lil’ app on my phone to keep tabs, and it’s a game-changer. Keeps me from overspending, ya know?

- Keep Utilization Low: Try to use less than 30% of your total credit limit across all cards. If one card’s getting close, switch to another for purchases ‘til you pay it down. Simple, but effective.

- Pay Off Balances Monthly: If you can, pay off every card in full each month. Interest charges are a killer, and carrying a balance don’t do your score no favors. I learned this after racking up a dumb amount of interest one year—never again!

- Check Statements Regularly: Skim your statements for weird charges or fees. Fraud happens, and catching it early can save your score (and your wallet). I check mine every week or so, just to be safe.

- Space Out Applications: Don’t apply for a bunch of cards at once. Spread ‘em out—maybe one every 6 months or so—to avoid too many hard inquiries piling up. I made that mistake once, applied for three in a month, and my score took a nosedive.

Follow these, and you’ll be fine. It’s all about discipline, y’all.

A Personal Story: My Credit Card Mishap

Lemme tell ya a quick story about how I almost screwed myself over with credit cards. A few years back, I thought I was hot stuff, applying for every card with a cool design or signup bonus. I ended up with, like, six cards. Sounds dope, right? Wrong. I was spending left and right—new sneakers on this card, dinner on that one, a random gadget on another. Before I knew it, I had balances on all of ‘em, and I couldn’t keep track of due dates. Missed a couple payments, got slapped with fees, and my score dropped like a rock. Took me months to dig outta that hole.

What’d I learn? More cards ain’t better unless you’ve got a grip on your habits. I cut down to just two cards after that, paid off the rest, and focused on keeping my spending in check. Now, my score’s better than ever, and I ain’t stressing over a wallet full of plastic. Moral of the story: quality over quantity, fam.

Other Factors That Matter More Than Card Count

While we’re on the topic, let’s not forget that the number of cards you’ve got ain’t the only thing—or even the main thing—affecting your credit score. Honestly, these other factors often matter way more:

- Payment History: Like I said earlier, this is the biggest chunk of your score. Pay on time, every time. One late payment can haunt you for years.

- Debt Levels: Even with a bunch of cards, if you’re carrying high balances, your score suffers. Focus on paying down debt before worrying about adding cards.

- Length of History: Keep older accounts open if you can. Closing an old card shortens your credit history, which can hurt. I’ve got a card from 10 years ago I barely use, but I keep it active just for this reason.

So, don’t get too hung up on how many cards you’ve got. It’s just one piece of the puzzle. Focus on the big picture—being responsible with whatever credit you’ve got.

When Should You Apply for a New Card?

Timing matters when it comes to getting a new card. Don’t just apply ‘cause you’re bored or saw a sweet ad. Here’s when it makes sense:

- Your current utilization is high (over 30%), and you need more available credit to bring it down.

- You’ve got a specific need, like a travel rewards card for a big trip, and you know you can manage the extra account.

- Your finances are stable, and you’ve got a handle on existing debt and payments.

And when not to apply? If you’re already struggling with payments, got a bunch of recent inquiries, or just don’t need it. Wait ‘til you’re in a better spot. I’ve turned down card offers even with killer bonuses ‘cause I knew I wasn’t ready. Patience pays off.

Wrapping It Up: More Cards, More Responsibility

So, does having more credit cards increase your credit score? It can, if you use ‘em to keep your utilization low and diversify your credit mix. But it ain’t a guarantee, and it sure as heck ain’t worth the risk if you’re not disciplined. Stick to 2-3 cards, manage ‘em like a boss, and focus on paying on time and keeping debt low. That’s the real secret to a killer score.

I’ve shared my two cents—and my dumb mistakes—hoping it helps you avoid the same traps. Got more than a couple cards already? Cool, just keep an eye on spending. Only got one? Might be worth getting another if you’re ready. Whatever you do, make sure it fits your life and your budget. Drop a comment if you’ve got a credit card story to share—I’m all ears! Let’s keep this money convo goin’.

Issues with having multiple credit cards

Despite the potential benefits, owning multiple credit cards is not without its downsides. The biggest risk is that you can easily spend more in credit than youre able to repay in cash. Plus, keeping track of multiple credit cards — all with different interest rates, due dates, minimum payments and other fees — can become overwhelming.

Additionally, charge offs, late payments and high credit utilization rates can create negative marks on your credit reports if you are not careful.

Before opening a new credit card account, be sure that youre ready for the additional financial responsibility. Keep an eye on your spending habits and find ways to organize your finances.

Is it good to have multiple credit cards?

Having multiple credit cards, along with other types of credit, can be a good thing, as long as you use each one responsibly.

Two factors that contribute to your credit score are the number and type of credit accounts. If your goal is to get or maintain a good credit score, two to three credit card accounts, in addition to other types of credit, are generally recommended. This combination may help you improve your credit mix.

Lenders and creditors like to see a wide variety of credit types on your credit report. Keeping up with multiple credit accounts suggests to lenders that you understand how credit works and know how to manage the amounts you borrow.

Many credit cards also offer borrowers access to special rewards programs. These might include cashback options for certain purchases, travel benefits or other types of rewards.

How Many Credit Cards Should You ACTUALLY Have?

FAQ

Does having more credit cards increase credit score faster?

Having multiple cards can help you build credit more quickly, but your focus should remain on using your card (or cards) responsibly for the best impact on your credit. Too many cards could tempt you to overspend or run up your balances, so be diligent about managing your budget no matter how many cards you have.Feb 28, 2025

Are 4 credit cards too many?

What is the 2/3/4 rule for credit cards?

How much does adding a credit card increase your credit score?

Rossman notes that when people open a new credit card, doing so essentially lowers the average age of their credit accounts. “I would say for most people, the total impact is probably not going to be more than 10 to 20 points and probably shouldn’t linger more than like three to six months,” says Rossman.