Yes, if you open and put money into an individual retirement account (IRA), you can lower your taxable income and your tax bill. But it depends, first and foremost, on the type of IRA you have. Contributing to a traditional IRA reduces your adjusted-gross income (AGI) for the year, which could put you in a lower tax bracket. However, contributing to a Roth IRA doesnt reduce your taxable income since youre contributing after-tax dollars in order to withdraw them tax-free down the road.

There are a lot of people like you who are wondering if putting money into a Roth IRA will help them pay less tax this year. This question makes it hard for many people to figure out how to save for retirement. Allow us to make things clear by learning the exact way that Roth IRAs impact your AGI.

The Quick Answer: No, Roth IRA Contributions Don’t Reduce AGI

I’ll give it to you straight: Roth IRA contributions do NOT reduce your AGI or your taxable income for the current year. This is because Roth IRAs are funded with after-tax dollars.

Now don’t click away because you think Roth IRAs aren’t worth it. There’s a lot more to this story. They won’t lower your taxes right now, but they will save you a lot of money in the long run.

Understanding AGI and How Retirement Accounts Affect It

First, let’s get clear on what AGI actually is. Your Adjusted Gross Income (AGI) is the amount of money you made during the tax year after any deductions were taken into account. It’s very important since it has a direct impact on how much tax you pay.

Many people try to reduce their AGI because lower AGI = lower tax bill. But not all retirement accounts impact your AGI the same way:

- Traditional IRA contributions: REDUCE your AGI (with some limitations)

- Roth IRA contributions: DO NOT reduce your AGI

- 401(k) contributions: REDUCE your AGI

Traditional IRAs vs. Roth IRAs: The Tax Difference

Traditional IRAs:

- Funded with pre-tax dollars

- Contributions can reduce your AGI and current tax bill

- You’ll pay taxes when you withdraw funds in retirement

- Required Minimum Distributions (RMDs) start at age 72

Roth IRAs:

- Funded with after-tax dollars

- Contributions do NOT reduce your AGI or current tax bill

- Tax-free growth and qualified withdrawals

- No RMDs during your lifetime

- Contributions can be withdrawn anytime without penalty

As Kimberly Lankford from Kiplinger puts it “A Roth IRA can give your retirement strategy a real boost, so it’s worth taking the time to see if you can contribute to one”

Why Choose a Roth IRA If It Doesn’t Lower Your AGI?

You might be thinking “If Roth IRAs don’t reduce my taxes now. why bother?” Great question! Here’s why Roth IRAs are still awesome

- Tax-free growth: Your investments grow without tax liability

- Tax-free withdrawals: Qualified distributions in retirement are completely tax-free

- No RMDs: Unlike traditional IRAs, Roth IRAs don’t require withdrawals during your lifetime

- Access to contributions: You can withdraw your contributions (not earnings) anytime without taxes or penalties

- Tax diversification: Having both pre-tax and after-tax money gives you flexibility in retirement

If you think your tax rate will be higher when you retire than it is now, the Roth IRA is a great way to save money. Many younger workers and early-career professionals benefit from this approach.

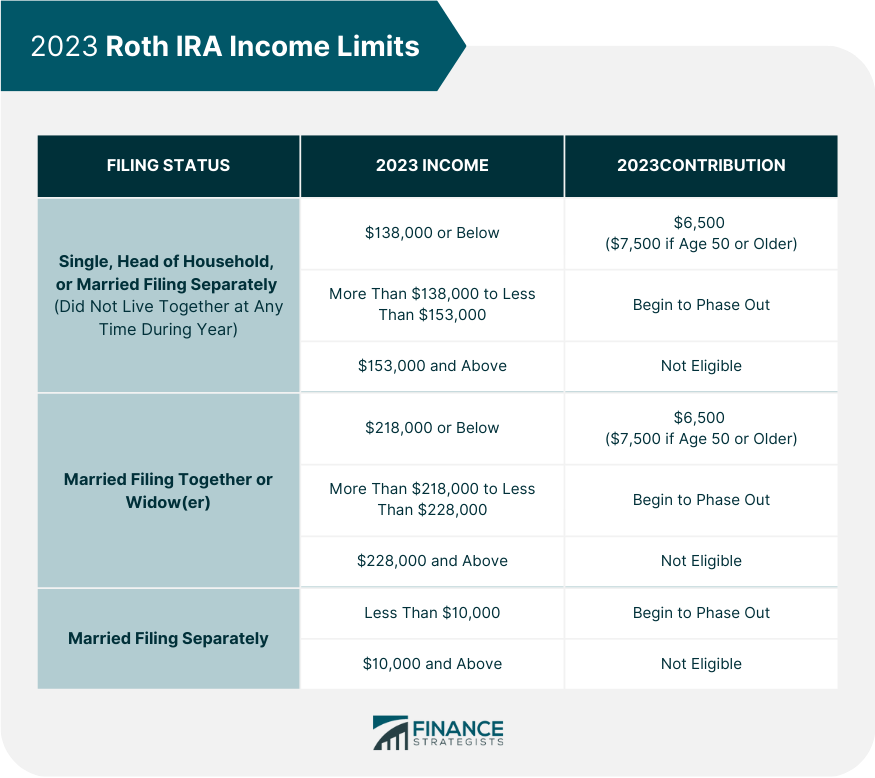

Income Limits for Roth IRA Contributions (2025)

Not everyone can contribute directly to a Roth IRA. For 2025, here are the income limits:

Single filers:

- Full contribution if MAGI is below $150,000

- Partial contribution if MAGI is $150,000-$165,000

- No contribution if MAGI exceeds $165,000

Married filing jointly:

- Full contribution if MAGI is below $236,000

- Partial contribution if MAGI is $236,000-$246,000

- No contribution if MAGI exceeds $246,000

The maximum contribution amount is $7,000 for 2025 ($8,000 if you’re 50 or older).

7 Strategies to Lower Your MAGI to Qualify for Roth Contributions

If your income is too high to contribute to a Roth IRA directly, don’t worry! Here are seven strategies that can help lower your Modified Adjusted Gross Income (MAGI) so you might qualify:

1. Contribute to a Traditional IRA

Unlike Roth contributions, traditional IRA contributions can reduce your MAGI. For 2025, you can contribute up to $7,000 ($8,000 if you’re 50+).

2. Maximize Your Workplace Retirement Plan

Contributing to a 401(k), 403(b), 457 plan, or Thrift Savings Plan reduces your MAGI. The contribution limit for 2025 is $23,500, plus a $7,500 catch-up contribution if you’re 50+. ($11,250 for 2025 for some plans!)

3. Contribute to a Health Savings Account (HSA)

If your health insurance has a high enough deductible, you can contribute to an HSA. For 2025, the limit is $4,300 for individual coverage and $8,550 for family coverage, plus $1,000 extra if you’re 55+. These contributions reduce your MAGI.

4. Use a Flexible Spending Account (FSA)

If your employer offers an FSA, you can contribute up to $3,300 in 2025 to pay for healthcare expenses. This reduces your MAGI. You can’t usually contribute to both an HSA and healthcare FSA in the same year.

5. Use a Dependent Care FSA

If you pay for childcare, you might be able to contribute up to $5,000 to a dependent care FSA, which also reduces your MAGI.

6. Lower Your Self-Employment Income

If you have self-employment income, make sure you’re claiming all eligible deductions on Schedule C. You might also consider setting up a SEP IRA or Solo 401(k).

7. Harvest Capital Losses

If you have investments that have decreased in value, consider selling them to realize the loss. You can offset up to $3,000 of ordinary income with capital losses, which reduces your MAGI.

The Backdoor Roth IRA Option

If your income is too high to contribute directly to a Roth IRA, you still have the “backdoor Roth” option. This involves:

- Contributing to a non-deductible traditional IRA (which has no income limits)

- Converting the traditional IRA to a Roth IRA

If you don’t have other traditional IRA money, you’ll only pay taxes on any earnings between the contribution and conversion. This strategy is a bit more complex, so it might be worth talking to a financial advisor about it.

As explained by Kiplinger: “If you still don’t fall below the modified adjusted gross income cutoff, you can make a non-deductible IRA contribution and then convert it to a Roth.”

Traditional IRA Deductibility Limits for 2025

If you’re covered by a workplace retirement plan, here are the income limits for deducting traditional IRA contributions:

Single filers:

- Full deduction if MAGI is under $79,000

- Partial deduction if MAGI is $79,000-$89,000

- No deduction if MAGI exceeds $89,000

Married filing jointly (IRA contributor is covered by a workplace plan):

- Full deduction if MAGI is under $126,000

- Partial deduction if MAGI is $126,000-$146,000

- No deduction if MAGI exceeds $146,000

If you’re not covered by a workplace plan but your spouse is, different limits apply.

The Long-Term Tax Benefits of Roth IRAs

Even tho Roth IRAs don’t reduce your AGI now, they provide significant long-term tax benefits:

- Tax-free qualified withdrawals: Once you’re 59½ and have had the account for at least five years, all withdrawals are completely tax-free.

- No impact on Social Security taxation: Traditional IRA withdrawals can make your Social Security benefits taxable, but Roth withdrawals won’t.

- No Medicare IRMAA surcharges: Roth distributions don’t count toward the income thresholds that trigger higher Medicare premiums.

- Estate planning advantages: Roth IRAs can be excellent wealth transfer vehicles for your heirs.

Making the Right Choice for Your Situation

So, should you contribute to a Roth IRA even tho it doesn’t reduce your AGI? It depends on your situation:

A Roth IRA might be best if:

- You expect to be in a higher tax bracket in retirement

- You’re in a low tax bracket now

- You want tax-free withdrawals in retirement

- You want flexibility to access contributions if needed

- You want to avoid RMDs during your lifetime

A traditional IRA might be better if:

- You want to reduce your current AGI and tax bill

- You expect to be in a lower tax bracket in retirement

- You need the tax deduction now to afford retirement contributions

While Roth IRA contributions don’t reduce your AGI, they offer significant tax advantages that can make them a powerful part of your retirement strategy. The choice between traditional and Roth accounts isn’t just about getting a tax break today—it’s about optimizing your overall tax situation across your entire lifetime.

As Dechtman Wealth Management points out, “Contributions to a Roth IRA do not lower adjusted gross income. However, Roth IRAs can potentially reduce overall tax liability in the long term through tax-free investment growth and disbursements.”

What retirement savings strategy are you currently using? Have you found ways to balance current tax benefits with long-term tax planning? We’d love to hear your experiences in the comments!

How Does an IRA Affect My Taxes?

With a traditional IRA, you can make contributions with pre-tax dollars, thereby reducing your taxable income. Your investments will grow tax-free until you take distributions at the age of 59½, where you will then be taxed on the amount distributed. Roth IRAs are different because they are funded with money that has already been taxed. This means that they don’t change your taxes and you won’t have to pay taxes on the money when you take it out.

How to Reduce Your MAGI

Here are some ways to reduce your income so you may contribute to a Roth IRA.

How to lower your AGI or MAGI – Benefits of tax planning

FAQ

How can I legally reduce my AGI?

How to reduce AGIContribute to a Health Savings Account. If you participate in an eligible Health Savings Account, you may have the option to contribute up to $4,150 to their HSA accounts for 2024, and families can contribute up to $8,300. Retirement savings. Student loan interest deduction. Educator expenses.

Can I contribute to a Roth IRA if I make $300,000 a year?

No, with an income of $300,000, you likely cannot contribute directly to a Roth IRA, as this exceeds the income limits for 2025, which are less than $150,000 for single filers and $236,000 for joint filers.

Can I reduce my taxable income by contributing to an IRA?

When you file your federal income tax return, you might be able to deduct the amount you put into your IRA. See IRA contribution limits. Aug 26, 2025.

Does putting money into a Roth reduce taxable income?

Contributions to a Roth account are made on a “post-tax” basis. You pay taxes up-front and contributions cannot be deducted from your yearly income, but when you reach retirement age both the earnings and contributions can be withdrawn tax-free.

Can a Roth IRA reduce your AGI?

Yes, they surely can. Contributions to a traditional IRA are made with pre-tax dollars and do reduce your AGI. However, contributions to a Roth IRA do not lower adjusted gross income.

Does a Roth IRA reduce adjusted gross income?

Contributions to a traditional IRA can reduce your adjusted gross income (AGI) for that year by a dollar-for-dollar amount. It may be hard to lower your AGI if you have a traditional IRA and a workplace retirement plan. This is because of your income and the plans you have. Contributions to a Roth IRA do not lower your adjusted gross income.

Do deductible IRA contributions reduce adjusted gross income (AGI)?

Deductible contributions to a traditional IRA reduce Adjusted Gross Income (AGI), a key component of MAGI. Lowering AGI can help taxpayers qualify for income-sensitive tax benefits. For the 2024 tax year, the maximum deductible contribution is $6,500, or $7,500 for individuals aged 50 and over.

Do Roth IRA contributions reduce taxable income?

Therefore, they do reduce your AGI (in most cases). However, you will pay taxes when you withdraw the funds at retirement. Roth IRA contributions are not tax-deductible, and therefore do not reduce your AGI. Similarly, a Roth IRA does not reduce taxable income in years when you make a contribution.

Do IRA contributions lower adjusted gross income?

A question we get asked a lot is whether or not putting money into an IRA can lower your adjusted gross income. The answer is yes, they can — but not always. You can contribute to an IRA to reduce taxes, but those contributions won’t always lower your AGI. Let’s see how and why. Do IRA Contributions Reduce AGI?.

Are Roth IRA contributions tax deductible?

Roth IRA contributions are not tax-deductible, and therefore do not reduce your AGI. Similarly, a Roth IRA does not reduce taxable income in years when you make a contribution. However, there are no taxes on investment growth or withdrawals in retirement (i.e. after you turn 59 ½) and you’ve had the account for over five years.