As Head of Financial Planning, Jason is a strategic partner who is responsible for developing the strategy, managing the planner teams, and coordinating personal financial planning activities across Citizens Wealth Management to help clients navigate and grow in changing circumstances.

Today, the average American retires at around age 63. But what if youre thinking about how to retire at 50 instead?.

For some people, this type of early retirement is their top financial goal. Their dream is to work hard and sacrifice throughout their early years so they can live the rest of their lives on their own terms.

Of course, living below your means in your 20s, 30s, and 40s isn’t the only way to get 10 or more years extra before retirement. Youll also have to maximize your biggest accumulation years and make savvy investment decisions along the way.

There are lots of factors at play when trying to retire by 50. Here are eight considerations to get you started.

Dreaming of leaving the workforce earlier than most? You’re not alone. Many of us fantasize about saying goodbye to the alarm clock and hello to leisurely mornings before we hit the traditional retirement age. But can you actually retire at 54? The short answer is yes—with careful planning and some strategic financial moves.

It is possible to retire early at age 54, but you need to plan more carefully than if you were to retire at the normal age of 65 or 67. I will tell you everything you need to know to make this dream come true.

The Financial Reality of Retiring at 54

Retiring just one year before the commonly targeted early retirement age of 55 might seem like a small difference, but it can have significant implications for your financial planning Here’s why

-

Longer retirement: If you retire at 54 and live to 90, you’ll have 36 years of living costs to pay for without a regular paycheck.

-

No Social Security yet: You won’t be eligible for Social Security retirement benefits until age 62 at the earliest, leaving an 8-year gap.

-

Limited access to retirement accounts: Most retirement accounts have restrictions on penalty-free withdrawals before 59½.

-

Healthcare coverage gap: Medicare eligibility doesn’t start until age 65, so you’ll need to find other health insurance for 11 years.

How Much Money Do You Need to Retire at 54?

How much you’ll need depends on how you want to live in retirement, but here are some general rules:

The Multiplier Rule

Many financial experts suggest having 7-10 times your annual income saved by your mid-50s. So if you earn $100,000 annually, you should aim for $700,000 to $1,000,000 in retirement savings.

However, I think this is actually a bit simplistic. Your actual needs will depend on:

- Your expected annual expenses in retirement

- Whether you’ll have any part-time income

- Your investment returns during retirement

- Your life expectancy

- Healthcare costs

- Inflation rates

The 4% Rule

Another approach is the 4% rule, which suggests you can withdraw 4% of your retirement savings in your first year of retirement, then adjust that amount for inflation each subsequent year.

For example, if you want $80,000 in annual retirement income, you’d need:

$80,000 ÷ 0.04 = $2,000,000 in retirement savings

But I gotta be honest with you—the 4% rule was developed assuming a 30-year retirement period. Since you’re retiring at 54, you might need to be more conservative and use a 3-3.5% withdrawal rate instead.

Accessing Your Money Before 59½

One of the biggest challenges of retiring at 54 is accessing your retirement funds without penalties. Here are some strategies:

1. Rule of 55 (Almost)

The IRS Rule of 55 allows penalty-free withdrawals from your current employer’s 401(k) or 403(b) if you leave your job in or after the year you turn 55. Since you’re retiring at 54, you’d miss this by one year—unless you can delay your official retirement date until your 55th birthday.

2. Substantially Equal Periodic Payments (SEPP)

The IRS 72(t) provision allows penalty-free withdrawals from IRAs through substantially equal periodic payments. These payments must continue for five years or until you reach 59½, whichever is longer.

3. Roth IRA Contributions

You can withdraw your original Roth IRA contributions (but not earnings) at any time without penalties or taxes, provided the account has been open for at least five years.

4. Non-Retirement Savings

This is where having significant investments outside retirement accounts becomes crucial. Taxable brokerage accounts, high-yield savings accounts, and other investments can provide income without age restrictions.

Bridging the Healthcare Gap

Healthcare is often the biggest financial challenge for early retirees. Here are your options for coverage between 54 and Medicare eligibility at 65:

1. COBRA Coverage

You can continue your employer’s health plan through COBRA for up to 18 months, but you’ll pay the full premium plus an administrative fee.

2. Health Insurance Marketplace

You can purchase a plan through the Affordable Care Act marketplace. Depending on your income, you might qualify for premium subsidies.

3. Spouse’s Health Plan

If your spouse continues working, joining their health plan is usually the most cost-effective option.

4. Healthcare Sharing Ministries

These are not insurance but can provide some coverage at lower costs than traditional insurance.

Remember that healthcare costs alone could easily reach $15,000-$20,000 annually for a couple in their 50s and early 60s. That’s a significant expense to build into your retirement budget!

Social Security Considerations

While you can’t claim Social Security at 54, understanding how it fits into your long-term plan is important:

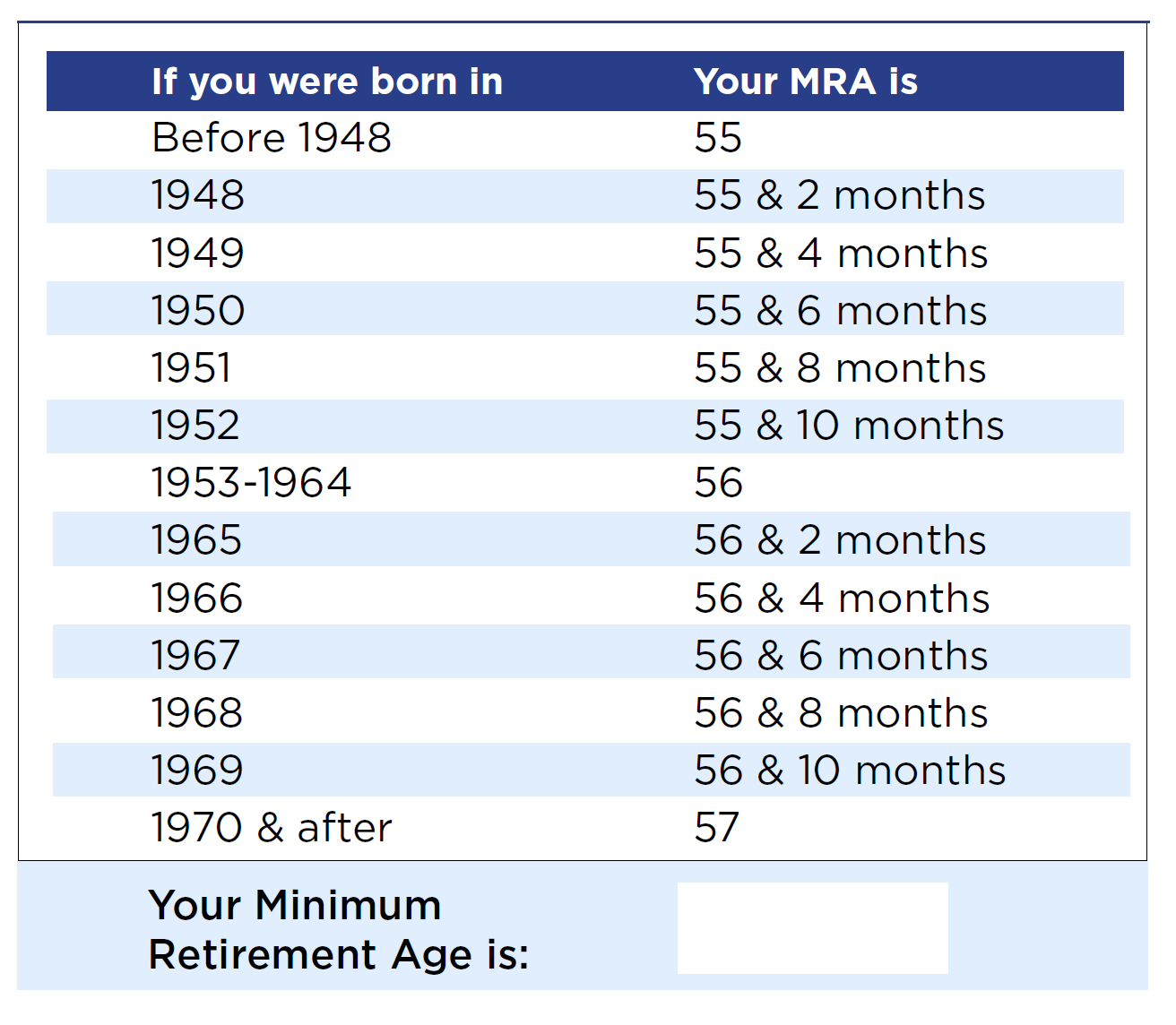

- The earliest you can claim is age 62, but benefits will be permanently reduced by up to 30%.

- Full retirement age (FRA) is between 66-67, depending on your birth year.

- Delaying benefits until age 70 increases your monthly payment to 132% of your regular benefit amount.

For many early retirees, it makes financial sense to delay Social Security as long as possible, living off other savings first, to maximize this guaranteed lifetime income.

Creating Multiple Income Streams

Diversifying your income sources is crucial for early retirement success. Consider these options:

1. Dividend-Paying Investments

High-quality dividend stocks or funds can provide regular income without selling assets.

2. Rental Properties

Real estate can generate ongoing passive income while potentially appreciating over time.

3. Part-Time Work or Consulting

Many “retirees” continue working 10-20 hours weekly in fields they enjoy, providing both income and purpose.

4. Annuities

An annuity contract can provide guaranteed income starting at your chosen date, though they come with fees and less flexibility.

A Sample Early Retirement Budget at 54

Here’s what a realistic monthly budget might look like for a couple retiring at 54:

| Expense Category | Monthly Cost |

|---|---|

| Housing (mortgage/rent, taxes, insurance, maintenance) | $2,000 |

| Healthcare (insurance premiums, out-of-pocket) | $1,500 |

| Utilities (electricity, water, internet, phone) | $500 |

| Food (groceries, dining out) | $800 |

| Transportation (car payment, gas, maintenance, insurance) | $600 |

| Travel/Entertainment | $1,000 |

| Miscellaneous (clothing, gifts, etc.) | $500 |

| Total | $6,900 |

This budget totals $82,800 annually. Using a 3.5% withdrawal rate, you’d need approximately $2.37 million in retirement savings to generate this income sustainably.

Real-Life Strategies from Someone Who Did It

When I retired at 54 last year, I relied on several key strategies that made early retirement possible:

- Maximized retirement contributions: I took full advantage of catch-up contributions after 50

- Developed multiple income streams: I built a rental property portfolio providing $3,000 monthly

- Started a side business: My consulting work brings in about $2,000 monthly with just 10 hours of work

- Downsized early: We moved to a smaller home in a lower-cost area five years before retirement

- Planned for healthcare: We set aside $300,000 specifically for healthcare costs until Medicare eligibility

Common Questions About Retiring at 54

Can I start my own business to supplement retirement income?

Absolutely! Starting your own business can be an excellent strategy. The IRS allows you to contribute up to $69,000 for 2024 (plus $7,500 catch-up if you’re over 50) to retirement accounts through your business, depending on the type of plan you set up.

Should I pay off my mortgage before retiring at 54?

There’s no one-size-fits-all answer. Having no mortgage reduces monthly expenses, but maintaining a low-interest mortgage while keeping more money invested could potentially yield higher returns. I personally chose to pay off my mortgage for the peace of mind.

How do I pressure-test my retirement plan?

Run scenarios for unexpected events like:

- Living 10 years longer than expected

- A major market downturn early in retirement

- Higher-than-anticipated inflation

- Unexpected long-term care needs

What if I’m behind on retirement savings in my late 40s?

Consider these acceleration strategies:

- Maximize catch-up contributions to retirement accounts

- Reduce current expenses dramatically to increase savings

- Develop additional income sources

- Consider working until 55 or 56 instead

Final Thoughts: Is Retiring at 54 Right for You?

Early retirement at 54 isn’t just about having enough money—it’s about crafting a meaningful post-career life. Before making the leap, ask yourself:

- What will give my days purpose and structure?

- Have I built strong social connections outside of work?

- Do I have hobbies and interests to pursue?

- Have I stress-tested my financial plan with a professional advisor?

For me, retiring at 54 was the right decision because I had both the financial foundation and a clear vision for this next life chapter. With careful planning, strategic saving, and realistic expectations, you too might find that retiring at 54 isn’t just a dream—it’s an achievable reality.

Remember that working with a qualified financial advisor who specializes in early retirement planning can help you navigate the complexities and develop a personalized roadmap to retire at 54 with confidence.

Have you started planning for early retirement? What strategies are you implementing to reach your goals sooner? I’d love to hear about your journey in the comments below!

Know what type of retirement you want

Everyone has different expectations for retirement. Thats why theres no universal answer to the question of how much you need to retire.

One guideline is to expect to need between 60% and 100% of your annual pre-retirement income for every year of retirement. Where you fall in this spectrum depends on the type of retirement you envision. For instance, if you want to travel the world, you could easily spend 10% of your previous yearly income. But if youre envisioning a modest retirement lifestyle, you may only need 60% of your previous salary.

To get a ballpark figure of how much youll need, start by estimating your expected income by age 50. Depending on the type of retirement you want, multiply that salary number by anywhere between 0. 6 (60%) and 1. 0 (100%) to get an idea of how much youll need to finance each year of your retirement.

For a retirement lifestyle similar to your current lifestyle:

- Salary at 50 years old x 1. 0 (100%) = Annual retirement allowance.

For a more modest retirement lifestyle:

- Salary at 50 years old x 0. 6 (60%) = Annual retirement allowance.

Max out your retirement accounts

Tax-advantaged retirement accounts like 401(k)s and IRAs have annual contribution limits. For people younger than 50, the 2025 limit for 401(k) contributions is $23,500 while IRAs are limited to $7,000. People age 50 or older can contribute $8,000 to IRAs. By maxing out one or all of your retirement accounts, youll have more tax-advantaged retirement money that can compound over the years.

However, finding $23,500 to contribute to your 401(k) every year takes more than cutting back on discretionary spending. Thats especially true when youre in your 20s and still climbing the professional ladder. To live as cheaply as possible in your 20s, don’t take any expensive trips and keep driving your used car as long as it works, or don’t get one at all if you can. Direct all of those extra funds toward the future. The sooner you can max out your retirement accounts, the better. Some people find that automatically contributing to your 401(k) and IRA each pay period can help increase your savings over time.