You changed your traditional IRA to a Roth IRA, but now you’re not sure if you should have done it. The tax bill may have been bigger than you thought, or your finances may have changed. You’re probably wondering: can a Roth conversion be recharacterized?.

I’ve helped many clients navigate this exact situation, and the short answer is: No, Roth conversions can no longer be recharacterized. But don’t worry – there’s more to understand about this topic that might help your retirement planning.

The Current Rules on Roth Conversion Recharacterization

To be very clear, the Tax Cuts and Jobs Act (TCJA) of 2017 got rid of the option to recharacterize Roth conversions beginning in 2018. This means that once you move money from a traditional IRA to a Roth IRA, you can’t take it back.

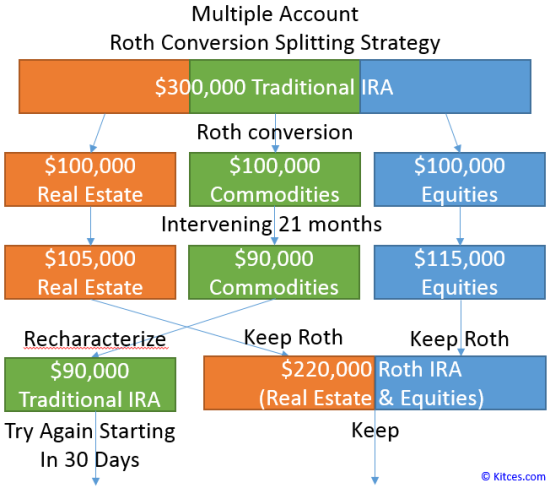

One way to “undo” a Roth conversion before this change was to change it back to a traditional IRA. This was particularly helpful if:

- The value of your investments dropped after conversion

- Your tax situation changed unexpectedly

- You realized the tax bill was larger than anticipated

However, the tax law changes have closed this loophole permanently. The AccountingInsights team says, “Recharacterization is no longer possible for conversions made after 2018.” “.

What Can Still Be Recharacterized?

While Roth conversions can’t be reversed, there are still some recharacterization options available:

Contributions Can Be Recharacterized

You can still recharacterize IRA contributions (not conversions) This means

- You can change a Roth IRA contribution to a traditional IRA contribution

- You can change a traditional IRA contribution to a Roth IRA contribution

This flexibility is particularly valuable if

- You made a Roth IRA contribution but later discovered your income exceeds the eligibility limits

- You contributed to a traditional IRA but realized you can’t deduct the contribution

- Your tax situation changed, making one type of IRA more advantageous than the other

According to Fidelity Investments, “Let’s say you’ve made a wise retirement move and contributed to a Roth or Traditional IRA. But you’ve changed your mind and want to reclassify it as a contribution to the other type of IRA. The IRS lets you—it’s called a recharacterization.”

Recharacterization Deadlines and Rules

If you’re planning to recharacterize an IRA contribution, you need to be aware of the timing:

Deadline for Recharacterizing

The deadline for recharacterizing an IRA contribution is:

- The tax filing deadline for the year (typically April 15)

- Plus any extensions you receive (potentially up to October 15)

As Investopedia explains, “The deadline for recharacterizing an IRA contribution is the tax-filing deadline for that year, including any extensions you qualify to get.”

For example, for contributions made in 2024, you would have until April 15, 2025, to recharacterize. If you file for an extension, you’d have until October 15, 2025.

The Earnings Calculation Requirement

When you recharacterize a contribution, you must include any earnings (or losses) on that contribution. This can be a bit tricky to calculate, but many IRA custodians will do this for you.

Fidelity notes: “When you recharacterize, the IRS requires an earnings calculation to account for any gains or losses on the amount you’re recharacterizing. The calculation is based on the change in value of your entire account, not just the contribution itself.”

Steps to Recharacterize an IRA Contribution

If you need to recharacterize a contribution (remember, not a conversion), here’s what you’ll need to do:

- Confirm the details: Verify the date and amount of your original contribution

- Notify your custodian: Contact your financial institution with a formal recharacterization request

- Complete the necessary forms: Most custodians have specific forms for this process

- Document everything: Keep records of all transactions for tax purposes

The AccountingInsights Team recommends: “Start by verifying the details of your original conversion, including the date, amount, and accounts involved. Accurate records are critical for the process and for amending your tax filings.”

Tax Implications of Recharacterization

Understanding the tax aspects of recharacterization is crucial:

Reporting Requirements

When you recharacterize an IRA contribution, your financial institution will:

- Issue Form 5498 showing both the original contribution and the recharacterized amount

- Provide Form 1099-R showing the distribution from the first IRA

- Include a special code on Form 1099-R to indicate it’s a recharacterization (not taxable)

You may also need to file Form 8606 with your tax return for partial recharacterizations.

Impact on Your Tax Return

A recharacterization can affect:

- Your adjusted gross income (AGI)

- Eligibility for certain tax credits and deductions

- Medical expense deductions (which are only allowed above a certain percentage of AGI)

- Child Tax Credit and Earned Income Tax Credit eligibility

As AccountingInsights points out, “Consider how the recharacterization affects your taxable income and eligibility for deductions or credits. A lower adjusted gross income (AGI) could improve your ability to claim deductions.”

Common Scenarios for Recharacterization

Let’s look at some real-world situations where recharacterizing might make sense:

Scenario 1: Income Exceeds Roth Limits

Jack contributes $6,000 to a Roth IRA in January. By December, he gets an unexpected bonus that pushes his income above the Roth IRA eligibility limits. To avoid penalties, he recharacterizes his contribution to a traditional IRA before filing taxes.

Scenario 2: Seeking Tax Deduction

Sarah makes a $7,000 contribution to a Roth IRA. Later, she realizes she could really use the tax deduction from a traditional IRA contribution. Since she’s eligible for the deduction, she recharacterizes her contribution before the tax filing deadline.

Scenario 3: Changed Retirement Strategy

Michael contributes to a traditional IRA, but after consultation with his financial advisor, decides a Roth IRA better suits his long-term retirement goals. He recharacterizes his contribution to take advantage of tax-free growth.

Alternatives to Recharacterization for Roth Conversions

Since we can’t recharacterize Roth conversions anymore, what options do we have?

1. Plan Your Conversions Carefully

- Convert smaller amounts gradually over several years

- Convert in years when your income is lower

- Work with a tax professional to estimate the tax impact before converting

2. Consider a “Backdoor Roth”

If your income is too high for direct Roth contributions, you might consider:

- Making a non-deductible contribution to a traditional IRA

- Converting that contribution to a Roth IRA

- Being mindful of the “pro-rata” rule if you have other traditional IRA assets

3. Utilize Tax-Loss Harvesting

If you’re facing a large tax bill from a Roth conversion, consider:

- Selling investments with losses in taxable accounts

- Using those losses to offset some of the taxable income from the conversion

- Staying mindful of wash-sale rules

Key Takeaways About Roth Conversion Recharacterization

To wrap things up, here are the most important points to remember:

- Roth conversions can no longer be recharacterized (reversed) since 2018

- IRA contributions can still be recharacterized from traditional to Roth or vice versa

- The deadline for recharacterizing contributions is the tax filing deadline plus extensions

- When recharacterizing, you must transfer both the contribution and any related earnings/losses

- Proper documentation and tax reporting are essential for recharacterizations

Final Thoughts

The elimination of Roth conversion recharacterization means we need to be more careful when planning conversions. What used to be a reversible decision is now permanent, so thorough planning is essential.

I always tell my clients to consult with a qualified tax professional before making significant retirement account moves. The rules are complex, and the tax implications can be significant.

Have you had experience with recharacterizing IRA contributions? Or perhaps you’ve had to adapt your retirement strategy since the recharacterization rules changed? I’d love to hear about your experiences in the comments!

Remember, while we can’t undo Roth conversions anymore, thoughtful planning can still help you optimize your retirement savings and minimize your tax burden.

How Recharacterization Works

A recharacterization lets you treat a regular contribution that you made to a Roth IRA or a traditional IRA as one that you made to another type of IRA.

You could recharacterize a $7,000 contribution to your Roth IRA (the first IRA) as a $7,000 contribution to your traditional IRA (the second IRA). Note that $7,000 is the contribution limit to an IRA for 2024 ($6,500 for 2023).

Recharacterizing a contribution from one type of IRA to another gives you the opportunity to change your mind or correct a mistake—say, you contributed to a Roth even though your income was too high.

You have until the due date for your federal income tax return (including any extensions) for the year when you made the first contribution to recharacterize your contribution. As long as you recharacterize your contribution by this deadline, you can treat the contribution as made to the second IRA for that year. This means that you can effectively ignore the contribution you made to the first IRA.

You can use the year you made the first contribution as your tax year, not necessarily the year you made the contribution itself. Remember that you generally have until April 15 to make a prior-year contribution.

To change the type of IRA a contribution goes into, you must ask the financial institution that holds your IRA to move the amount—including the contribution and any earnings—to a different type of IRA. The recharacterization can occur either within the same institution (if you use one custodian for both IRAs) or via a trustee-to-trustee transfer if different providers maintain the IRAs.

What Is Recharacterization?

Recharacterization refers to two separate individual retirement account (IRA) strategies:

- It is possible to change the name of a contribution to an IRA to a contribution to a different IRA. Right now, this strategy is legal, and you can change the type of contribution you make from a Roth IRA to a traditional IRA or the other way around, but there are deadlines you need to meet.

- Before, a conversion from a Roth IRA to a traditional IRA could be changed or undone. But because of the Tax Cuts and Jobs Act, this plan is no longer legal. If you convert your IRA to a Roth IRA today, you can’t take it back.

- A contribution to one individual retirement account (IRA) can be reclassified as a contribution to another IRA, but there are deadlines that must be met.

- Prior to the Tax Cuts and Jobs Act, you could change the type of account from a Roth IRA to a traditional IRA.

- Roth IRA conversions are now irrevocable. Once you convert to a Roth, there’s no turning back.

Can I Recharacterize A Roth Conversion? – Elder Care Support Network

FAQ

Can I recharacterize a Roth conversion?

No. 115-97), a conversion from a traditional IRA, SEP or SIMPLE to a Roth IRA cannot be recharacterized. The new law also says that money rolled over from other retirement plans, like 401(k) or 403(b) plans, cannot be changed into a different type of account.

Can a Roth conversion be reversed?

To reverse a conversion by recharacterizing an account back to traditional IRA status you must submit the required form to your Roth IRA trustee or custodian …Aug 2, 2025.

Is a backdoor Roth considered a recharacterization?

No, a backdoor Roth IRA is a conversion, not a recharacterization, and they are distinct processes. A recharacterization is the process of changing an IRA contribution from one type to another, while a backdoor Roth is the process of converting funds from a traditional IRA to a Roth IRA.

What is the loophole for Roth IRA conversion?

Some people with high incomes use a “backdoor Roth IRA” to put money into an IRA even though they aren’t allowed to because of their income. Rather than contributing directly to a Roth, the backdoor strategy calls for contributing to a traditional IRA and then converting it to a Roth.

Can a Roth IRA conversion be recharacterized?

However, the Tax Cuts and Jobs Act (TCJA) of 2017 banned recharacterizing the account balance of a Roth conversion back to a traditional IRA. 9 10 Roth IRA conversions are now irrevocable.

What is a recharacterization of a Roth IRA?

Recharacterizations of traditional or Roth IRAs allow you to easily reverse a conversion from a Roth IRA to a traditional IRA. You can also use a recharacterization to switch the type of IRA after contributing. If you contribute to a Roth IRA and change your mind, you can recharacterize your contribution to a traditional IRA.

Can I recharacterize a Roth IRA conversion in 2023?

If an individual during 2023 converted a traditional IRA (including an SEP-IRA or a SIMPLE-IRA) to Roth IRA then the individual will not be able to recharacterize or undo the conversion. Recharacterization of a Roth IRA conversion was permitted prior to the passage of the Tax Cuts and Jobs Act of 2017 (TCJA), which became effective January 1, 2018.

How do I recharacterize a Roth IRA contribution?

To change the type of contribution made to a Roth IRA, the contribution must be moved from the Roth IRA to a traditional IRA that is not tax-deductible. This is called a “trustee-to-trustee” transfer. The deadline to transfer the Roth IRA to the nondeductible traditional IRA is April 15, 2024.

Can I recharacterize a Roth conversion after 2017?

Here’s what you need to know. The Tax Cuts and Jobs Act of 2017 eliminated the option to recharacterize Roth conversions after 2017. If you converted funds in 2017 or earlier, you might have been eligible to recharacterize under the old rules. For conversions made in 2018 and beyond, recharacterization is no longer available.

What is a backdoor Roth recharacterization vs a conversion?

You might wonder about the difference between a Backdoor Roth recharacterization vs a conversion. Since the Tax Cuts and Jobs Act of 2017, Roth IRA conversions are not reversible. Once you convert funds from a Traditional IRA to a Roth IRA, the decision is final. You’ll owe taxes on the converted amount.