Self-employment offers amazing freedom, but let’s be honest—retirement planning gets a bit tricky when you’re your own boss. Without that corporate 401(k) plan and employer match, you might be wondering what retirement savings options you have available. Well, I’ve got great news! As a self-employed person, you absolutely can open a Roth IRA, and it might be one of the smartest financial moves you’ll make.

The Quick Answer

Yes, self-employed individuals can definitely open and contribute to a Roth IRA! In fact, it’s one of the most crucial retirement savings tools you should have in your financial arsenal. The only limitations are based on your income level, not your employment status.

Why a Roth IRA Makes Sense for the Self-Employed

When you’re self-employed, retirement planning falls entirely on your shoulders. A Roth IRA offers several compelling advantages that make it particularly attractive for independent contractors, freelancers, and small business owners

- Tax-Free Growth: Your money grows completely tax-free

- Tax-Free Withdrawals in Retirement: You won’t owe taxes when you withdraw money in retirement

- No Required Minimum Distributions (RMDs): Unlike traditional IRAs, you’re not forced to take money out at age 72

- More Flexibility for Emergencies: You can withdraw your contributions (but not earnings) without penalty if needed

- Potential Estate Tax Advantages: Your beneficiaries can receive the funds tax-free

For me, the best thing about it is that I can take money out tax-free when I retire. A big tax bill is the last thing I want when I’m old and living on a fixed income!

Roth IRA Eligibility and Contribution Limits (2025)

The good news is that having a Roth IRA doesn’t depend on whether you work for yourself or not. The main restriction is your income level:

2025 Roth IRA Income Limits

- Single filers: Phase-out begins at $146,000 and you become ineligible at $161,000

- Married filing jointly: Phase-out begins at $230,000 and you become ineligible at $240,000

2025 Contribution Limits

- $7,000 for those under 50

- $8,000 for those 50 and older (includes $1,000 catch-up contribution)

Don’t worry if your income is higher than these limits. There are ways to get around them, such as the “backdoor Roth IRA” strategy, which involves putting money into a traditional IRA that isn’t tax-deductible and then changing it into a Roth IRA.

Derek Munchow, a certified financial planner, points out that “Many self-employed individuals can reduce their adjusted gross income through business deductions and Solo 401(k) contributions to remain eligible for Roth contributions.”

How to Open a Roth IRA When Self-Employed

Opening a Roth IRA is surprisingly simple:

- Choose a financial institution – Popular options include Vanguard, Fidelity, Charles Schwab, Merrill Lynch, and E-Trade

- Complete the application – You’ll need your Social Security number and bank information

- Fund your account – Transfer money from your bank account

- Select your investments – Choose from options like index funds, ETFs, or target-date funds

Pro tip: Look for a brokerage with no account fees and low expense ratios on their funds. Those small fees can really add up over decades!

Smart Investment Strategies for Your Roth IRA

When investing your Roth IRA funds, keep it simple and focus on low-cost options:

- Target-date funds: These automatically adjust your investment mix as you age

- Index funds: Provide broad market exposure with minimal fees

- ETFs: Similar to index funds but trade like stocks

The most important factor? Fees! Look for expense ratios under 0.25% annually. Since your gains grow tax-free in a Roth IRA, keeping costs low maximizes your long-term growth.

Roth IRA vs. Other Self-Employed Retirement Options

While a Roth IRA is fantastic, it shouldn’t necessarily be your only retirement account. Here’s how it compares to other options:

| Plan Type | 2025 Contribution Limit | Tax Treatment | Best For |

|---|---|---|---|

| Roth IRA | $7,000 ($8,000 if 50+) | After-tax contributions, tax-free withdrawals | Tax diversification |

| SEP IRA | Up to 25% of net earnings (max $70,000) | Pre-tax contributions, taxable withdrawals | High-earning self-employed |

| Solo 401(k) | $23,000 employee + 25% of net earnings (up to $70,000 total) | Pre-tax or Roth options | Maximizing contributions |

| SIMPLE IRA | $16,000 ($19,500 if 50+) | Pre-tax contributions, taxable withdrawals | Small businesses with employees |

I like having a Roth IRA along with a SEP IRA or Solo 401(k). This gives me tax-free and tax-deferred money in retirement, which is a good balance.

5 Common Misconceptions About Roth IRAs for Self-Employed

Let me clear up some confusion:

-

Myth: You need an employer to open a Roth IRA

Reality: Nope! Anyone with earned income under the limits can open one -

Myth: You can’t have a Roth IRA and other retirement accounts

Reality: You can contribute to both a Roth IRA and SEP IRA/Solo 401(k) in the same year -

Myth: You need consistent income to contribute

Reality: You can contribute whenever you have earned income, even if it’s irregular -

Myth: You need a lot of money to get started

Reality: Many brokerages have no minimum to open an account -

Myth: It’s too complicated for self-employed folks

Reality: It’s actually one of the simplest retirement accounts to set up!

The 5-Year Rule: Important to Understand

One important detail: the “5-year rule.” After making your first Roth IRA contribution, you must wait five years before withdrawing earnings tax-free (even if you’re over 59½). The five-year period begins on January 1 of the year you made your initial contribution.

This doesn’t affect your contributions—just the earnings. You can withdraw your contributions anytime without penalties or taxes.

Maximizing Your Roth IRA: Tips for Self-Employed Individuals

To get the most from your Roth IRA:

- Set up automatic contributions – Even small, regular deposits add up over time

- Contribute early in the year if possible to maximize tax-free growth

- Max out your contributions whenever you can

- Consider a spousal Roth IRA if you’re married and your spouse doesn’t work

- Look at your entire retirement portfolio to ensure proper diversification

Real-Life Example: How a Roth IRA Grows

Let’s say you’re 30 years old and contribute the maximum $7,000 annually until retirement at 65. Assuming an 8% average annual return:

After 35 years, your Roth IRA would be worth approximately $1,295,000!

And the best part? That entire amount would be 100% tax-free when you withdraw it in retirement.

Combining a Roth IRA with Other Self-Employed Retirement Accounts

For many self-employed people, a Roth IRA works best as part of a broader retirement strategy. Here’s a practical approach:

- First, max out your Roth IRA ($7,000 or $8,000 if over 50)

- Then contribute to a SEP IRA or Solo 401(k) to reduce current taxes and save more

- If you have extra cash, consider a taxable brokerage account for additional investments

This multi-account approach gives you both tax-free and tax-deferred money in retirement, providing flexibility with your tax situation.

Final Thoughts: Why Every Self-Employed Person Should Consider a Roth IRA

As someone who’s been self-employed for years, I can’t emphasize enough how valuable a Roth IRA has been for my retirement planning. The combination of tax-free growth, no required minimum distributions, and access to contributions if needed provides both security and flexibility—two things every self-employed person appreciates!

The ability to build a tax-free retirement nest egg is particularly valuable for self-employed individuals who often have fluctuating incomes and lack employer-sponsored retirement benefits. By starting a Roth IRA today, you’re giving your future self the gift of tax-free income.

FAQ: Roth IRAs for Self-Employed Individuals

Q: Do I need earned income to contribute to a Roth IRA?

A: Yes, you must have earned income to contribute, but self-employment income definitely counts!

Q: Can I contribute to both a SEP IRA and a Roth IRA in the same year?

A: Absolutely! Your SEP IRA contributions don’t affect your Roth IRA contribution limit.

Q: What if my income varies year to year?

A: That’s fine! You can contribute different amounts each year, up to the annual limit, based on what you can afford.

Q: What investments should I choose in my Roth IRA?

A: Low-cost index funds or target-date funds are popular choices for their simplicity and low fees.

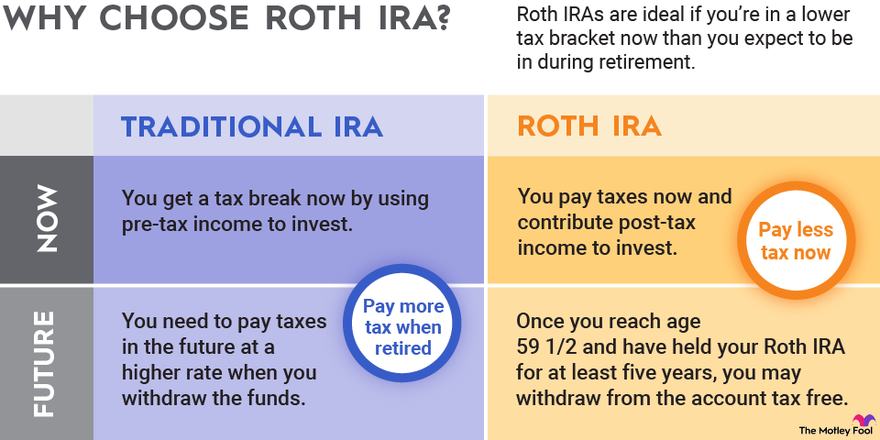

Q: How do I know if a Roth IRA is better for me than a traditional IRA?

A: If you expect to be in a higher tax bracket in retirement, a Roth IRA is generally better. Also, the flexibility of no RMDs makes Roth IRAs attractive for estate planning.

Remember, while being self-employed comes with its challenges, it also gives you the freedom to craft a retirement strategy that perfectly fits your unique situation. A Roth IRA should definitely be a consideration in that strategy!