Are you confused about whether to put your hard-earned money in a CD or an IRA? You’re not alone! As someone who’s spent years navigating the sometimes murky waters of personal finance. I’ve had many friends ask me “What is the difference between CDs and IRAs?”

The short answer is that they are two completely different types of financial tools that are used for different things. A Certificate of Deposit (CD) is a way to save money with guaranteed returns. An Individual Retirement Account (IRA) is an investment account with tax breaks designed for retirement.

But there’s so much more to know! Let’s dive into the nitty-gritty details so you can make the best choice for your financial future.

CD vs IRA: The Basics

Before we get into the complex stuff let’s break down what these financial products actually are

Certificate of Deposit (CD):

- A type of savings account offered by banks and credit unions

- You deposit money for a specific time period (the “term”)

- The bank pays you a fixed interest rate

- Your money is locked away until the CD matures

Individual Retirement Account (IRA):

- A tax-advantaged investment account designed for retirement savings

- Can hold various investments (stocks, bonds, ETFs, and even CDs!)

- Offers tax benefits to incentivize long-term retirement savings

- Has rules about contributions and withdrawals

Key Differences Between CDs and IRAs at a Glance

| Feature | Certificates of Deposit (CDs) | Individual Retirement Accounts (IRAs) |

|---|---|---|

| Account Type | Savings product | Investment account |

| Purpose | Short to medium-term savings | Long-term retirement savings |

| Returns | Guaranteed, relatively low | Not guaranteed, variable (depends on investments) |

| Risk Level | Low risk | Varies based on investment choices |

| Term Length | 1 month to 10 years | Until age 59½ or later |

| Tax Benefits | No special tax advantages | Yes (varies by IRA type) |

| Early Withdrawal | Penalty fees apply | Penalties for withdrawals before age 59½ (with some exceptions) |

| Insurance | FDIC/NCUA insured up to $250,000 | Only deposit accounts in IRA are insured; securities are not |

| Contribution Limits | Varies by institution | Set by IRS ($7,000 in 2025 for under 50, $8,000 for 50+) |

Deep Dive into CDs

How CDs Work

When you open a CD, you’re essentially making a deal with the bank: “I’ll give you my money for X amount of time, and you’ll pay me a guaranteed interest rate.” The bank benefits by having your money to use for loans, and you benefit from a higher interest rate than you’d typically get with a regular savings account.

There are terms for CDs that range from one month to ten years. Most of the time, the longer the term, the more interest you’ll earn. But keep in mind that your money will be locked up during that time.

Types of CDs

There are several types of CDs you might encounter:

- Standard CD: The most common type with fixed rate and term

- No-penalty CD: Allows withdrawals without penalty (but typically has lower rates)

- Bump-up CD: Lets you request a rate increase if rates go up during your term

- IRA CD: A CD held within an IRA (more on this later!)

- Jumbo CD: Requires a large minimum deposit (usually $100,000+)

Pros of CDs

- Guaranteed returns: You know exactly what you’ll earn

- Safety: CDs at FDIC-insured banks or NCUA-insured credit unions are protected up to $250,000

- Higher rates than savings accounts: CDs typically offer better rates than regular savings accounts

- Can be opened jointly: You can share a CD with another person like your spouse or child

Cons of CDs

- Limited liquidity: Your money is locked away until maturity

- Early withdrawal penalties: You’ll pay fees if you need your money before the term ends

- Lower returns: CDs generally don’t earn as much as investments in the stock market over time

- No tax advantages: CD interest is taxable in the year it’s earned

Deep Dive into IRAs

How IRAs Work

An IRA isn’t an investment itself – it’s a tax-advantaged container that holds investments. Think of it like a special box where you can put various investments (stocks, bonds, mutual funds, ETFs, and even CDs), and that box comes with tax benefits.

You open an IRA at a financial institution (bank, credit union, or brokerage), fund it, and then decide how to invest that money.

Types of IRAs

The two most common types are:

-

Traditional IRA: You contribute pre-tax dollars, which might make you eligible for tax deductions now. You’ll pay taxes when you withdraw money in retirement.

-

Roth IRA: You contribute after-tax dollars (no immediate tax benefit), but qualified withdrawals in retirement are completely tax-free!

Other types include SEP IRAs (for self-employed), SIMPLE IRAs (for small businesses), and self-directed IRAs (for alternative investments).

Pros of IRAs

- Tax advantages: Either tax-deferred growth (Traditional) or tax-free withdrawals (Roth)

- Investment flexibility: You can invest in a wide range of assets

- Higher potential returns: Historically, stock market investments have outperformed CDs over the long term

- Designed for retirement: Structured to help you save for your future

Cons of IRAs

- Investment risk: Unlike CDs, investments in IRAs can lose value

- Early withdrawal penalties: Usually 10% penalty plus taxes for withdrawals before age 59½

- Contribution limits: The IRS limits how much you can contribute each year

- Income limits for some IRAs: For example, Roth IRAs have income eligibility restrictions

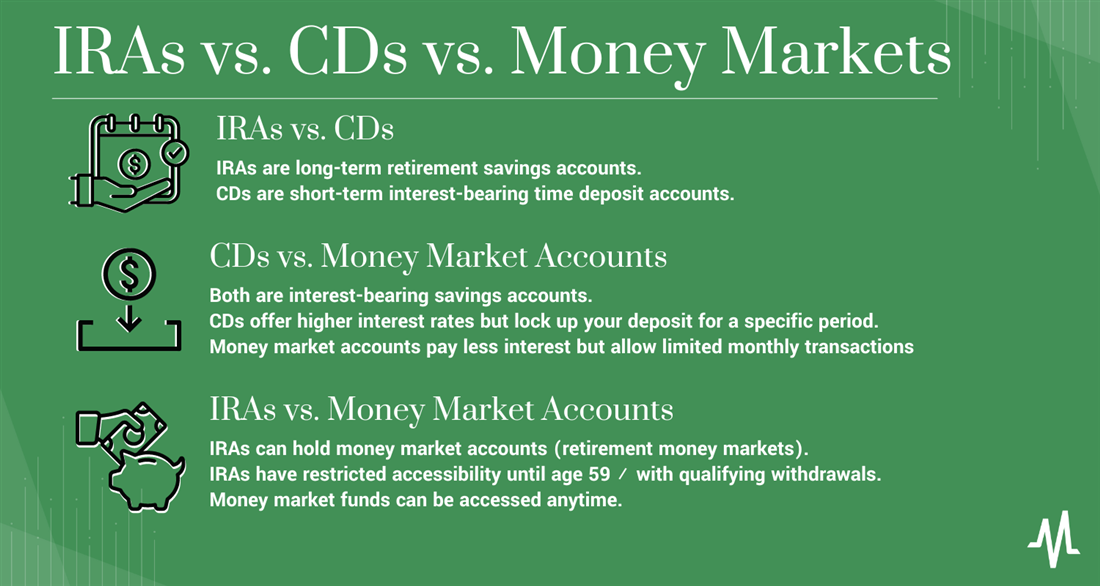

Can You Combine CDs and IRAs?

Yes! This is where things get interesting. You can actually hold a CD within an IRA – this is called an IRA CD.

An IRA CD gives you the safety and guaranteed returns of a CD with the tax advantages of an IRA. It’s basically a CD that’s held inside an IRA container. This can be a good option for conservative investors or those nearing retirement who want to reduce risk while maintaining tax benefits.

Which Should You Choose: CD or IRA?

The truth is, it’s not always an either/or decision. Many people benefit from having both in their financial strategy. Here is a quick list of times when each might be better:

Consider a CD if:

- You’re saving for a specific short-term goal (1-5 years away)

- You need a guaranteed return without risk

- You value safety over higher potential returns

- You already have retirement accounts established

Consider an IRA if:

- You’re saving for retirement

- You want tax advantages for long-term savings

- You’re comfortable with some level of investment risk

- You want the potential for higher returns over time

My Personal Experience

In my financial journey, I’ve used both CDs and IRAs, but they were used for different things. A few years ago, when I was saving for my wedding, I put my money in a 2-year CD because I knew exactly when I would need the money and didn’t want any risk. In the meantime, I’ve been putting regular money into my Roth IRA to save for retirement. I’ve invested in a mix of index funds that have gone up and down but have gained a lot over time.

For my emergency fund, I’ve used a ladder of short-term CDs to earn a bit more interest than a savings account while still maintaining some liquidity. And yes, for a portion of my IRA that I want to be super-safe, I’ve even used an IRA CD!

How to Get Started

Opening a CD:

- Research financial institutions for the best rates

- Decide on your term length and CD type

- Complete the application (online or in-person)

- Fund your CD with an initial deposit

- Make note of the maturity date

Opening an IRA:

- Choose the type of IRA that suits your situation (Traditional or Roth)

- Select a provider (bank, brokerage, robo-advisor)

- Complete the application process

- Make your initial contribution

- Select your investments

Final Thoughts

The main thing to remember is that CDs and IRAs serve different purposes in your financial life. CDs are savings vehicles best used for short to medium-term goals, while IRAs are investment accounts specifically designed for retirement with tax advantages to match.

Many successful financial plans include both! You might have an IRA to build your retirement nest egg, while also using CDs for your emergency fund or for saving toward specific goals like a home down payment or a dream vacation.

The right choice depends on your unique financial situation, goals, timeline, and risk tolerance. And remember – your strategy can (and should) evolve over time as your needs change!

What financial tools are you currently using? Have you had experience with CDs or IRAs? I’d love to hear about your experiences in the comments below!

Disclaimer: This article is for informational purposes only and is not financial advice. Always consult with a qualified financial professional before making important financial decisions.

What is an IRA?

It is possible for people with taxable income to open an IRA, which is a tax-advantaged investment account. IRAs are like 401(k) plans in that you can invest money into different assets such as stocks, bonds or mutual funds but unlike most 401(k)s, IRAs can be opened by an individual instead of an employer.

You can put money into a traditional IRA before taxes are taken out, so you won’t have to pay taxes on the money you put in until you take it out in retirement. Roth IRAs involve contributing after-tax dollars, allowing you to make tax-free withdrawals later in life.

IRAs also have limits on how much you can put in each year, and the IRS says you have to wait until you’re 59 ½ years old to start taking money out of them without being charged a penalty. In addition, you must meet certain income qualifications to contribute to a Roth IRA — if you earn too much money, you might not be able to fund one.

If you want to open an IRA, go through a reputable broker you can trust. Fidelity Investments and Vanguard both offer commission-free trading on various securities, such as stock and ETF trades, and zero or low-expense ratio index funds, making it relatively affordable to invest. Both also offer robo-advisor options for beginner investors new to the stock market.

- Minimum deposit and balance: The investment vehicle you choose may have different minimum deposit and balance requirements. Opening a Fidelity Go® account doesn’t cost anything, but you need to have at least $10 in it depending on the investment strategy you choose.

- FeesFees may vary depending on the investment vehicle selected. No fees to trade stocks, ETFs, options, or some mutual funds; over 3,400 mutual funds have no transaction fees; 65 per options contract. If you have less than $25,000 in Fidelity Go®, there are no advisory fees. 35% per year for balances of $25,000 or more, and this includes unlimited one-on-one coaching calls from a Fidelity advisor.

-

Bonus

Find special offers here

- Investment vehicles: Fidelity Go® IRA: Traditional, Roth, and Rollover IRAs; Fidelity Investments Trading; Fidelity Investments 529 College Savings; Fidelity HSA®; Fidelity Investments Other;

- Stocks, bonds, ETFs, mutual funds, CDs, options, and fractional shares are all ways to invest.

- Educational resources: Over 20 independent providers offer a wide range of tools and the most in-depth, industry-leading research.

- Minimum deposit and balance: The investment vehicle you choose may have different minimum deposit and balance requirements. There is no minimum to open a Vanguard account, but many retirement plans require a $1,000 deposit. To sign up for the robo-advisor Vanguard Digital Advisor®, you must deposit at least $100.

- FeesFees may vary depending on the investment vehicle selected. Zero transaction fees for over 3,000 mutual funds and no commission fees for trading stocks and ETFs. IRAs and brokerage accounts have a $20 annual service fee unless you choose paperless statements. The robo-advisor Vanguard Digital Advisor® charges up to $0 20% in advisory fees (after 90 days).

-

Bonus

None

- Vanguard Classic, Roth, Rollover, Spousal, and SEP IRAs are available, as well as Vanguard Digital Advisor® robo-advisors. Vanguard Trading handles brokerage and trading, and Vanguard 529 Plans are available as well.

-

Investment options

Stocks, bonds, mutual funds, CDs, ETFs and options

-

Educational resources

Retirement planning tools

Pros and cons of CDs

While CDs help set aside your funds for a certain period, they do come with some caveats that are important to consider.

- Rate of return that is guaranteed: When you buy a CD, you agree to deposit your money for a certain amount of time at a fixed interest rate. This makes sure that you always get a return on your investment.

- Higher yield than savings accounts—because you can’t take your money out as often, CDs usually have a higher yield than savings accounts, even some high-yield savings accounts.

- You won’t be able to get to your CD money before the end of the term without being charged a fee.

- Early withdrawal penalty—Depending on your bank and the length of your CD’s term, the penalty fees can be different. However, they are usually based on the interest earned or the interest you would have earned over a certain number of days or months.

What Is the Difference Between an IRA & CD?

FAQ

Is a CD better than an IRA?

If you have short-term savings goals, like to help pay for your wedding, a CD is likely the better fit. If you are saving for retirement, an IRA can offer better returns over the long run.

What is the average IRA balance for a 70 year old?

The average IRA balance for a 70-year-old is not directly provided in recent data, but the average retirement savings for a household aged 65-74 is approximately $609,000, according to SmartAsset.

Are CDs the same as IRAs?

No, a Certificate of Deposit (CD) is not an IRA; they are different financial tools, but a CD can be held within an IRA account, creating what’s known as an IRA CD.

What is the biggest negative of putting your money in a CD?

The biggest negative of putting your money in a Certificate of Deposit (CD) is the lack of liquidity and flexibility, as you cannot easily access your funds without incurring a penalty.

What is the difference between an IRA and a CD?

While IRAs and CDs are both tools for saving, but there are key differences between the two. An IRA is a retirement investing account that offers tax advantages. You can hold a range of investments in an IRA, including a CD. By putting money into a CD account for a certain amount of time, you can be sure of a certain rate of return.

Should I use a CD or an IRA?

Consider a certificate of deposit (CD) and/or an individual retirement account (IRA). But they work in very different ways, and there are times when you might want to use one over the other. Both can be part of a diversified investment strategy. While IRAs and CDs are both tools for saving, but there are key differences between the two.

What is an IRA CD & IRA savings account?

Simply put, an IRA is a tax-advantaged account designed to help you save for retirement. You have the freedom to customize your IRA holdings according to your individual needs. With an IRA CD or savings account, you can get the tax benefits of an IRA and the safety of steady returns.

Are CDs better than IRAS?

Both certificates of deposit (CDs) and individual retirement accounts (IRAs) can play a valuable role in your savings and investment strategy. But depending on your goals, one might serve you better than the other. It’s also possible that both CDs and IRAs have a place in your financial strategy.

Are IRA CDs the same as IRA share certificates?

However, you may not be as familiar with an IRA certificate of deposit (CD) and their credit union counterparts, IRA share certificates. An IRA CD works just like a regular CD: It’s a fixed-term savings account that offers a guaranteed rate of return. So in the simplest terms, IRA CDs are CDs can be opened inside of an IRA.

What is the difference between a CD and an Individual Retirement Account?

CDs are generally considered best for short- to medium-term needs, such as saving for a vacation or a large purchase, since they mature within months or years. An individual retirement account is a type of investment account that helps you save for retirement.