Contributions to a traditional individual retirement account (IRA), Roth IRA, 401(k), and other retirement savings plans are limited by law so that highly paid employees don’t benefit more than the average worker from the tax advantages that they provide. Contribution limits vary by the type of plan, the age of the plan participant, and, in some instances, how much the person earns.

Have you ever looked at your Roth IRA contribution limits and thought “Seriously? That’s it?” You’re not alone. Many investors find themselves puzzled and frustrated by the seemingly low Roth IRA contribution limits compared to other retirement accounts like 401(k)s. In 2024 most individuals can only contribute $7,000 to their Roth IRA (or $8,000 if you’re 50 or older), while 401(k) contribution limits sit at a much more generous $23,000 ($30,500 with catch-up contributions).

So why is there such a big difference? Is there a reason for all this chaos? Let’s look at the reasons behind these strict limits and what they mean for your planning for retirement.

The Current State of Roth IRA Limits

Let’s be clear about the “what” before we get into the “why.” How low are these limits?

2024 Retirement Account Contribution Limits:

- Roth IRA: $7,000 ($8,000 if age 50+)

- Traditional IRA: $7,000 ($8,000 if age 50+)

- 401(k): $23,000 ($30,500 if age 50+)

That means 401(k) contribution limits are more than three times higher than Roth IRA limits! And to make matters worse, high-income earners face additional restrictions:

2024 Roth IRA Income Phase-Out Ranges:

- Single filers: $146,000-$161,000

- Married filing jointly: $230,000-$240,000

Once your income exceeds these thresholds you can’t contribute directly to a Roth IRA at all. Ouch!

Why Are Roth IRA Limits So Low? The Real Reasons

1. Tax Revenue Concerns

The easiest way to explain it is through taxes, or more specifically, tax revenue. Keep in mind that Roth IRA contributions are made with money that has already been taxed, but qualified withdrawals are tax-free. This means the government never gets to tax that growth.

When Congress established IRAs in the 1970s (and later Roth IRAs in the 1990s), they had to balance retirement policy with fiscal responsibility. Higher contribution limits would mean potentially billions in lost future tax revenue.

2. Targeting Middle-Income Savers

IRAs were first made so that regular workers could save for retirement, not so that rich people could avoid paying taxes. The relatively low contribution limits were chosen so that average Americans could save a reasonable amount of money and high-income people couldn’t hide huge amounts of money from taxes.

As Christine Benz, director of personal finance at Morningstar, points out: “The IRA was designed to be supplemental for people who had workplace retirement plans and primary for those who didn’t.”

3. Balancing With Employer Plans

The government has historically given preference to employer-sponsored retirement plans like 401(k)s. The thinking goes: since 401(k)s encourage broader retirement plan participation (through employer matches, automatic enrollment, etc.), they deserve higher contribution limits.

IRAs, being individual accounts without these broader benefits, get lower limits. It’s the government’s way of nudging people toward workplace retirement plans when possible.

4. The Nondiscrimination Testing Factor

For 401(k) plans, there are built-in safeguards called “nondiscrimination testing” that prevent highly-compensated employees from benefiting disproportionately. These tests ensure that retirement benefits are distributed somewhat evenly across income levels within a company.

IRAs don’t have such protections, so lower contribution limits serve as a crude alternative to prevent abuse.

The Income Limits: Adding Insult to Injury?

As if the contribution limits weren’t restrictive enough, Roth IRAs also come with income limits that can prevent higher earners from contributing at all. But why?

The income limits further reinforce the original intent of IRAs: to help middle-class workers save for retirement, not to provide additional tax advantages to those already financially well-off.

For high earners in 2024:

- If you’re single with a Modified Adjusted Gross Income (MAGI) above $161,000, you can’t contribute directly to a Roth IRA

- If you’re married filing jointly with MAGI above $240,000, you’re also completely phased out

These income restrictions don’t exist for traditional 401(k) contributions, though Roth 401(k) contributions are permitted regardless of income level.

The Backdoor Solution (For Now)

While direct Roth IRA contributions may be limited, savvy investors have found a workaround: the backdoor Roth IRA. This two-step strategy involves:

- Contributing to a Traditional IRA (which has no income limits for contributions, though deductibility may be limited)

- Converting that Traditional IRA to a Roth IRA

This perfectly legal strategy allows high-income earners to effectively contribute to a Roth IRA despite being above the income limits. It’s worth noting that there have been legislative efforts to eliminate this strategy, though none have succeeded so far.

Historical Context: Have Roth IRA Limits Always Been This Low?

Actually, yes – relatively speaking. When Roth IRAs were first introduced in 1998, the contribution limit was a mere $2,000. While this limit has increased over time with inflation adjustments, it’s never been anywhere close to 401(k) limits.

Here’s how the limits have evolved:

| Year | Roth IRA Limit | 401(k) Limit |

|---|---|---|

| 1998 | $2,000 | $10,000 |

| 2005 | $4,000 | $14,000 |

| 2015 | $5,500 | $18,000 |

| 2024 | $7,000 | $23,000 |

The gap has remained significant throughout history, reflecting the consistent policy approach.

Are There Any Benefits to These Limits?

While the limits may seem frustratingly low, they do serve some positive purposes:

Encouraging Diverse Savings Strategies

The limits force investors to diversify their retirement savings across multiple account types, which can create tax diversification in retirement. By having some money in tax-deferred accounts (traditional 401(k)/IRA), some in tax-free accounts (Roth), and some in taxable accounts, retirees gain flexibility in managing their tax situation.

Forcing Better Planning

Lower limits mean investors need to be more strategic about their contributions and overall retirement planning. This often leads to more thoughtful decisions about which accounts to prioritize and how to maximize tax advantages.

What Can You Do About Low Roth IRA Limits?

So the limits are low, and we now understand why. But what can you actually do about it as an investor? Here are some practical strategies:

1. Max Out Your Workplace Plan First

If your employer offers a 401(k) with a match, that should typically be your first priority before worrying about an IRA. The match is free money, and the higher contribution limits are beneficial.

2. Consider a Roth 401(k) If Available

Many employers now offer Roth 401(k) options, which combine the higher contribution limits of a 401(k) with the tax-free growth of a Roth. Even better, there are no income restrictions on Roth 401(k) contributions!

3. Use the Backdoor Roth Strategy

If you’re above the income limits, the backdoor Roth conversion strategy remains viable. Just be aware of the pro-rata rule if you have existing traditional IRA balances.

4. Supplement With Taxable Investments

Once you’ve maxed out your available retirement accounts, don’t forget that taxable investment accounts can still be tax-efficient, especially if you focus on tax-efficient ETFs, index funds, and qualified dividends.

5. Consider HSAs (The “Stealth” Retirement Account)

Health Savings Accounts offer triple tax benefits and can effectively serve as another retirement account once you reach age 65.

Will Roth IRA Limits Ever Increase Substantially?

While contribution limits do increase gradually with inflation, it’s unlikely we’ll see Roth IRA limits suddenly jump to match 401(k) levels without major tax code reform. The fundamental reasons for the lower limits – tax revenue concerns and the focus on middle-income savers – remain unchanged.

However, retirement policy does evolve over time. Recent legislation like the SECURE Act and SECURE 2.0 have made significant changes to retirement planning rules, though they didn’t dramatically increase IRA contribution limits.

My Take on Roth IRA Limits

I’ve always found it frustrating that Roth IRA limits are so low. The account offers incredible benefits – tax-free growth and withdrawals, no RMDs, and flexible inheritance rules – yet the government severely restricts how much we can contribute.

On the other hand, I understand the reasoning. If there were no limits, wealthy individuals could shelter millions from taxation, and the government would lose substantial revenue. The system isn’t perfect, but it does attempt to balance encouraging retirement savings with fiscal considerations.

For us regular folks trying to save for retirement, the best approach is to understand the limits, plan accordingly, and use all the tools available – even if some of those tools are more restricted than we’d like.

Final Thoughts

The low Roth IRA contribution limits exist for specific policy reasons – primarily to target benefits toward middle-income Americans while preserving tax revenue. While these limits can be frustrating, understanding them helps us develop better retirement planning strategies.

By combining different account types, taking advantage of workplace plans, and using strategies like backdoor Roth conversions when appropriate, you can still build a robust retirement plan despite the limitations.

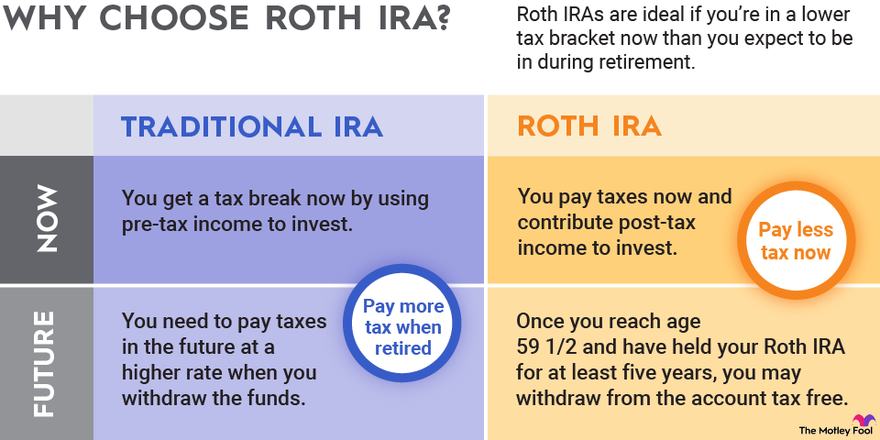

Roth IRA Contribution Rules

Unlike traditional IRAs, Roth IRAs do have income limits on whether a taxpayer is eligible to contribute. This has led to a two-step plan called a “backdoor Roth IRA.” This is when wealthy taxpayers put money into a traditional IRA and then change it into a Roth IRA. ).

Such as, in 2023, a married person filing a joint tax return can put all of their income into a Roth IRA if their MAGI is less than $218,000 and only some of it if their MAGI is between $218,000 and $2228,000. Above $228,000, they are ineligible. The phase-out range is higher in 2024, ranging from $230,000 to $240,000.

Traditional IRA Contribution Rules

Anyone, regardless of their income, can contribute to a traditional IRA. But how much of a tax break they can get for their contributions depends on how much money they make and whether they (or their spouse) are covered by another retirement plan at work.

For example, imagine someone filing a joint return has another retirement plan. If this persons modified adjusted gross income (MAGI) is under $116,000 in 2023 or $123,000 in 2024, the person would be eligible for a full deduction for their contribution to a traditional IRA. If their MAGI was between $116,000 and $136,000 in 2023 or between $123,000 and $143,000 in 2024, they could take a partial deduction. Above that amount, they still could contribute to a traditional IRA but wouldn’t get any deduction.

If that same person did not have another retirement plan, they would be eligible for a full deduction if their income was less than $218,000 and a partial deduction with an income in the $218,000 to $228,000 range. This range is also higher for 2024, with the phase-out range for those not covered by a workplace retirement being between $230,000 and $240,000.

The $65,000 Roth IRA Mistake To Avoid

FAQ

Why can’t I put more than 7000 in my Roth IRA?

There are no age requirements for contributing to a Roth IRA, so individuals of any age with qualifying income can contribute. Whether or not you can make the maximum Roth IRA contribution (for 2025, $7,000 annually, or $8,000 if you’re age 50 or older) depends on your tax filing status and your MAGI.

Can I put $100,000 in a Roth IRA?

No, you cannot put $100,000 into a Roth IRA because annual contributions are limited to $7,000 for 2025 (or $8,000 if you are age 50 or older).

Why is there a $6000 limit on Roth IRA?

Because the Roth IRA reduces the amount of tax revenue the government receives in the future. Rich people would put a lot of money into it if there was no limit, which would mean less money for the government.

Can I have a Roth IRA if I make over 250k?

For single filers with an MAGI of $165,000 or more, or for joint filers with an MAGI of $246,000 or more, you can’t put money into a Roth IRA. Still, you can make contributions to a traditional IRA.

What if my income is less than my IRA contribution limit?

If your household income for the year is less than the contribution limit, then your personal IRA contribution may be limited by your earned household income. If you are married and file jointly, your limit may be limited by your spouse’s income if you have no income yourself and are contributing to a spousal IRA.

Does a Roth IRA have an individual contribution limit?

Like many other retirement accounts, a Roth IRA has an individual contribution limit each year. Because it is an individual contribution limit, it applies to your contributions to any IRA. That means that if you have both a traditional IRA and a Roth IRA that you contribute to, you’re unable to contribute more than the limit across both accounts.

What are the limitations of a Roth IRA?

The Roth IRA has a serious limitation. People with high incomes can’t put money directly into a Roth IRA because the contribution is phased out at high income levels. This means that, depending on a person’s earnings, contributions can go down a lot or even stop altogether.

Can a Roth IRA contribute more than a traditional IRA?

The contribution limits for IRAs apply to the combined limit for both traditional and Roth IRAs. While you can contribute to both types of IRA accounts, the total contributions cannot exceed the annual IRA contribution limit, or you may face tax penalties. Besides, Roth IRA contributions cannot exceed total earned household income for the year.

What is the Roth IRA contribution limit in 2025?

In 2025, the Roth IRA contribution limit is the same as for 2024 at $7,000 for those under 50, and $8,000 for those 50 and older. Your personal Roth IRA contribution limit, or eligibility to contribute at all, is dictated by your income level. A Roth IRA is a tax-advantaged way to save and invest for retirement.

What is the maximum Roth IRA contribution limit for 2024?

The maximum Roth IRA contribution limit for 2024 is $7,000 for those under 50, and an additional $1,000 in catch up contribution for those 50 and older. The Roth IRA contribution limit for 2025 is the same as for 2024.