Workplace retirement plans like 401(k)s offer tax benefits for your retirement savings. The tax benefit you receive depends on the type of contributions you make. Its important to understand the way your distributions are taxed so you can make informed decisions about what to do with your money.

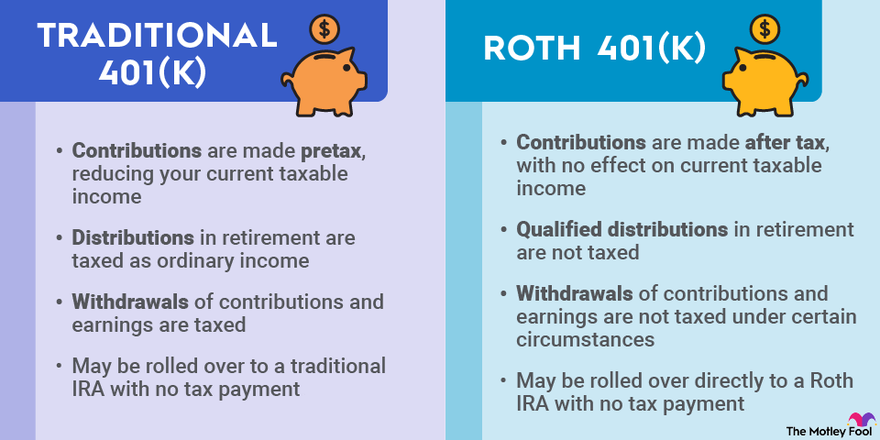

There are 3 types of contributions a participant may be able to make to a workplace retirement plan: pre-tax contributions, Roth contributions, and after-tax contributions.

Are you considering changing jobs or getting ready for retirement? You might be wondering what to do with your Roth 401(k) funds One popular option is rolling them over to a Roth IRA But can you rollover a Roth 401(k) to a Roth IRA? The short answer is yes – and it might be a smart financial move depending on your situation.

In this comprehensive guide, I’ll walk you through everything you need to know about Roth 401(k) to Roth IRA rollovers, including the benefits, potential pitfalls, and step-by-step process to make it happen.

What Are Roth 401(k) and Roth IRA Accounts?

Before diving into rollovers, let’s quickly review what these accounts are:

Roth 401(k):

- Employer-sponsored retirement plan

- Funded with after-tax dollars

- Contributions grow tax-free

- Withdrawals in retirement are tax-free (if qualified)

- Subject to required minimum distributions (RMDs) in some cases

- Contribution limit of $23,500 in 2025 ($7,500 additional catch-up if 50+)

Roth IRA:

- Individual retirement account

- Also funded with after-tax dollars

- Tax-free growth and withdrawals (if qualified)

- No required minimum distributions during your lifetime

- More flexible withdrawal options

- Subject to income limits for direct contributions

Can You Rollover a Roth 401(k) to a Roth IRA?

You can move your Roth 401(k) to a Roth IRA, that’s for sure. In fact, this is one of the most common rollovers people do when they retire or change jobs.

According to Dave Lowell, a Certified Financial Planner™ based near Salt Lake City, “You contact your employer’s 401(k) provider and request a rollover. They will then specify how much of the funds are pre-tax and how much are Roth contributions. You then direct them to make the funds transfer payable to the company where you hold your Roth IRA.”

Benefits of Rolling Your Roth 401(k) to a Roth IRA

There are several advantages to moving your money from a Roth 401(k) to a Roth IRA:

-

More Investment Options: Roth IRAs typically offer a wider range of investment choices compared to employer-sponsored Roth 401(k)s, which are limited to the plan’s offerings.

-

Account Consolidation: Moving multiple retirement accounts into a single Roth IRA makes it easier to track investments, manage contributions, and plan withdrawals.

-

No Required Minimum Distributions: You don’t have to take money out of a Roth IRA at any point in your life. This means that your money can grow tax-free for as long as you want.

-

Greater Withdrawal Flexibility Roth IRAs offer more flexibility for withdrawals before retirement including penalty-free withdrawals for first-time home purchases or qualified education expenses.

-

Estate planning benefits: You can leave Roth IRA funds indefinitely, which could be good if you want your beneficiaries to have as much money as possible.

The Rollover Process: Step by Step

Rolling over your Roth 401(k) to a Roth IRA isn’t complicated, but you need to follow the proper steps:

Step 1: Decide Where to Open Your Roth IRA

You’ll need to open a Roth IRA if you don’t already have one. These accounts can be opened at a lot of places, like traditional brokerages, banks, and online platforms.

Step 2: Request the Rollover

Contact your employer’s 401(k) provider and request a rollover distribution. You have three options for this transfer:

- Direct rollover: Your plan custodian cuts a check made out to the new account, which you deliver to the new custodian.

- Trustee-to-trustee transfer: The old and new custodians handle the transfer for you directly.

- 60-day rollover: You receive the funds as a distribution and must deposit them in the new account within 60 days to avoid taxes and penalties.

Step 3: Provide Instructions for the Rollover

Specify that you want to roll your Roth 401(k) into a Roth IRA. Be clear that you’re moving Roth money to a Roth account.

Step 4: Complete the Rollover

Follow through with any paperwork required by both the old plan administrator and your new Roth IRA custodian.

Step 5: Verify the Transfer

Once the rollover is complete, verify that all funds have been properly transferred to your Roth IRA.

Pro tip: The direct rollover or trustee-to-trustee transfer methods are generally safest, as they prevent you from accidentally missing the 60-day deadline or having taxes withheld.

Understanding the Five-Year Rule

One of the most confusing aspects of Roth account rollovers is the “five-year rule.” This rule affects when you can take tax-free withdrawals from your retirement accounts.

For Roth 401(k)s:

The five-year period starts when you first contribute to your Roth 401(k).

For Roth IRAs:

The five-year period starts when you make your first contribution to ANY Roth IRA.

When you rollover a Roth 401(k) to a Roth IRA, the rules get a bit more nuanced:

-

If you’re rolling funds into an existing Roth IRA that you’ve had for more than five years, you inherit that account’s five-year clock. This means you can take qualified distributions immediately (assuming you’re also 59½ or older).

-

If you’re rolling funds into a new Roth IRA, you’ll need to start a new five-year clock for that money.

As Lowell explains, “If you have an existing Roth IRA that is older than five years, then you can roll over the Roth 401(k) and take a distribution with no problem, assuming you’re 59½ or older. If you open a Roth IRA for the first time in order to receive Roth 401(k) rollover funds, then you must wait five years to take a distribution penalty-free.”

Potential Tax Implications

In general, rolling over a Roth 401(k) to a Roth IRA is not a taxable event since both accounts are funded with after-tax dollars. However, there are some nuances to be aware of:

Earnings on After-Tax Contributions

While your original Roth 401(k) contributions were made with after-tax dollars, any earnings on those contributions are considered pre-tax money. This means:

- If you do a direct rollover from the Roth 401(k) to the Roth IRA, there’s no tax due on the earnings.

- If you take a distribution from your Roth 401(k) and don’t roll it over, the earnings portion would be taxable if you haven’t met the requirements for a qualified distribution.

Partial Rollovers

If you’re doing a partial rollover of your Roth 401(k), be aware that the IRS has rules about how the money is allocated. In most cases, you must roll over a proportional amount of both contributions and earnings.

A Real-World Example

Let’s look at a hypothetical example of a Roth 401(k) rollover:

Andrew is 60 years old, retired, and has $1 million in his 401(k):

- $800,000 (80%) is pre-tax

- $200,000 (20%) is after-tax contributions

- $100,000 of the pre-tax portion represents earnings on his after-tax contributions

Andrew wants to rollover just his after-tax money to a Roth IRA. If his plan allows for source-specific withdrawals, he could withdraw from his after-tax source balance only. With that after-tax balance totaling $300,000 ($200,000 in contributions and $100,000 in earnings), two-thirds would be after-tax, and one-third would be pre-tax earnings.

This means Andrew could roll the $200,000 in after-tax contributions to his Roth IRA and the $100,000 in earnings to a traditional IRA, avoiding taxes on the transaction.

When to Consider Other Options

While rolling over to a Roth IRA has many advantages, it’s not always the best choice. Here are some situations where you might consider alternatives:

Leaving Money in Your 401(k)

Some potential benefits include:

- 401(k)s offer institutional pricing not available in IRAs

- Better protection from creditors under federal law

- Potential loan options

Rolling to Another Roth 401(k)

If you’re starting a new job with a good Roth 401(k) plan, rolling your old Roth 401(k) into the new employer’s plan might make sense, especially if:

- You want to consolidate accounts

- The new plan offers attractive investment options

- You want the stronger creditor protections of a 401(k)

Who Can Contribute to a Roth IRA?

If you’re considering opening a Roth IRA for your rollover, be aware that there are income limitations for making new contributions to Roth IRAs (though these don’t apply to rollovers):

For 2025:

- Single filers: Phase-out begins at $150,000 and ends at $165,000

- Married filing jointly: Phase-out begins at $236,000 and ends at $246,000

- Married filing separately: Phase-out between $0 and $10,000

The good news is that these income limits don’t apply to rollovers from Roth 401(k)s to Roth IRAs, so you can complete a rollover regardless of your income level!

Common Questions About Roth 401(k) to Roth IRA Rollovers

Can I roll my Roth 401(k) into an existing Roth IRA?

Yes, and this is often the best approach if you’ve had the Roth IRA for more than five years, as you’ll get credit for that five-year holding period.

Will I pay taxes when rolling over my Roth 401(k) to a Roth IRA?

Generally no. Since both accounts are funded with after-tax dollars, there’s typically no tax due on a direct rollover.

What happens if I miss the 60-day rollover window?

If you choose to receive the distribution yourself and don’t deposit it into a Roth IRA within 60 days, it may be treated as a distribution. The contribution portion would still be tax-free, but you may owe taxes and penalties on any earnings.

Can I roll over just a portion of my Roth 401(k)?

Yes, but be aware that for partial rollovers, you typically need to include a proportional amount of both contributions and earnings.

Final Thoughts

Rolling over your Roth 401(k) to a Roth IRA can be a smart financial move that gives you more control over your investments, eliminates required minimum distributions, and provides greater flexibility.

However, the rules can get complex, especially around the five-year rule and partial rollovers. Before making any decisions, I’d strongly recommend consulting with a financial advisor or tax professional who can help you navigate the process based on your specific situation.

Remember, the goal is to maximize your retirement savings while minimizing taxes – and a properly executed rollover can help you achieve both!

Taxes on earnings from after-tax contributions

After-tax contributions to a 401(k) or other workplace retirement plan get a different tax treatment than their earnings. Since youve already paid taxes on the contributions, those withdrawals are tax-free in retirement. But the IRS considers the earnings to be pre-tax—so they would be treated as pre-tax and you would owe income tax when you withdraw the earnings from the plan.

Money earned in a Roth IRA, on the other hand, is not taxed as long as only qualified withdrawals are made from the account. If you move after-tax contributions from a workplace plan to a Roth IRA, you might not have to pay taxes on any future earnings.

Rolling over after-tax money to a Roth IRA

If you have after-tax money in your traditional 401(k), 403(b), or other workplace retirement savings account, you can roll over the original contribution amounts to a Roth IRA without paying taxes, as long as certain rules are met. (Note: Your plans terms will determine when and how money is distributable. Please review your plan document or summary plan description for more information about disbursements from the plan. ).

The IRS says you can move money that has already been taxed to a traditional IRA2 and money that has already been taxed to a Roth IRA without making taxable income. When making a choice that could affect your taxes, you should always talk to a tax professional to make sure it’s the right choice for you. The IRS allows for a few different scenarios—but not all may be allowed by your plan.

In the most straightforward scenario, you would roll over the entire account balance out of the workplace plan and direct the after-tax contributions to a Roth IRA and pre-tax contributions and earnings to a traditional IRA.

The IRS treats plans that track separate source balances differently than plans that do not, allowing for withdrawals from a single source. Additionally, the IRS allows plan participants to take partial withdrawals. The catch is that your plan is not obligated to permit partial distributions or withdrawals of specific contribution types.

If the plan allows partial withdrawals and allows source-specific withdrawals, one could take a rollover of just the after-tax source balance, which includes both the after-tax contributions and all of the associated earnings. Again, the after-tax balance could go to a Roth IRA while earnings would go to a traditional IRA.

In that scenario, one could also choose to roll out only a portion of the after-tax balance. But, to roll over a partial amount of after-tax contributions, a proportional amount of associated earnings must also be rolled over.

Important note: Any partial withdrawals may affect eligibility for net unrealized appreciation treatment on appreciated employer stock held in the plan.

Read Viewpoints on Fidelity.com: Make the most of company stock in your 401(k)

Contributions made before 1987 are treated differently than those made after 1987. Pre-1987 employee contributions may be distributed without taking a taxable disbursement of the associated earnings. If you have contributions from 1986 or before, consult your tax advisor for more information.