If you’ve spent years in a permanent job, you can get very used to a regular income. And if you haven’t always been in paid work, the thought of guaranteed payments dropping into your bank account in a nice, predictable way can be very appealing indeed.

That can be one of the advantages of retirement. You can combine the State Pension and your own retirement savings to create a regular guaranteed monthly income for yourself. And buying an annuity is one of the most reliable ways of doing that. But how much does an annuity cost?.

Barry: Hi, John. Great to see you again. Ive been thinking. All my life Ive been working, and Ive been used to getting a salary every month. A fixed amount I know is going to come in that I feel comfortable about. And then Im going to retire. Whats going to happen then?.

John: The good thing about an annuity is it can replicate that. People who have been getting a salary or who haven’t are pretty familiar with the idea of having a steady income. Annuity gives you that, it will pay out the amount of money you expect. The money will be sent to you on the date you expect, and at the rate you expect. And that could be monthly. It could be half-yearly. It could be yearly. You make the choice because, as we’ve already talked about, the annuity is designed to fit your needs.

Barry: Well thats fantastic because its a bit like working, getting that income without all the hard work of actually going to work. I like that, that sounds fantastic. Reassuring. Thats reassuring to me. Like it would be to a lot of employed people, I suspect. How much does it cost?

John: How much an annuity costs depends on what income you want. So, if youre trying to achieve a certain amount of income that will have a specific cost to it. The minimum you can usually buy an annuity for is £5,000. Okay. But theres no upper limit. So, you can invest as much as you want to purchase that annuity. There are some things that will affect the level of income that you can get though, from that. So if you choose certain features on your annuity it can work by reducing your initial income that you receive.

John: So for example, if you were to include a loved one on your annuity so that it pays money to them after you die, then there is a cost to that. So the income that you receive will reduce slightly. Thats the result. Its also worth bearing in mind, Barry, that just like a salary, the income will be taxed as income. Okay. So as youre used to unfortunately paying those taxes, youre still going to have to do that with your retirement income. And all the costs and charges are taken into consideration for the product when you get your annuity rate and when you income, theres no further costs and charges to pay there. One thing to bear in mind, though, is if you do use a financial advisor to help you, there could be charges that they make for the for the advice that they give you.

Barry: Thanks, John. So how do I calculate how much I want to spend on my annuity?

John: A good place to start would be L&Gs annuity calculator. That can give you a good idea about the income that you can achieve for varying amounts of investment. There are also other calculators that you can use from providers. And even the Money and Pension Service have their calculators as well that you can use.

John: Yeah, of course. Lets say Im 65, I remain in perfect health. I dont want to add any options, any loved ones, anything like that to it. And Ive built up a pension pot of, just say for arguments sake, a nice round figure of £100,000.

John: Well, the first thing youll get is 25% of it as a tax-free lump sum. So a quarter of your money, £25,000 youll get tax-free from the off. Yeah, its a good perk. And then with the remainder of the money, you would buy your income. Based on those figures, youre probably looking at about £4,700 a year as an income.

Barry: Thats really helpful. But what if I built up a bigger pot of money, what if I had say for instance, £500,000 pounds?

John: Well congratulations on saving that much, Barry, youve done well. The good news is your tax-free sum increases quite a bit. So youre now up to £125,000 pounds as tax-free cash that you can take from that. And then the income that you could achieve from purchasing that annuity with the rest of it is £23,400 a year.

Barry: Right, so starting to get interesting. Im starting to get more tax-free cash, which sounds really appealing as well. Not that I want to necessarily work for longer, but lets just say I hold off a bit and I decide to not take my annuity until a little bit later in life. Will that make a big difference?

John: Yes it does. So your annuity rate that weve discussed previously, one of the things it looks at is how long your life expectancy is. So as you get older, obviously that shortens. So you can look to get a higher income as a result. So your annuity rate will increase and the amount of income that you get will increase. So its worth remembering, apart from the tax-free cash amounts Ive said that all the income is going to be liable to income tax when you receive it.

Barry: Right, okay. Really helpful. So weve looked at these almost mythical amounts, 100,000 500,000. But when I get to retirement with my specific figure, how do I work out whats good for me?

John: The Retirement Living Standards website might be a really good place to start, Barry. It allows you to set out some of the things that you want to achieve in your retirement. Be that holidays, cars, you know, general, looking after yourself and itll help you come up with a total sum and show you how on track you are for meeting that. Its a really, really useful website. I recommend you use that one.

Barry: Really practical. I really like this. Im starting to think about figures, amounts and more importantly, over all of this is what I might actually want and what I might actually need, and what I want my retirement to look like and then see how I can fund it. John, youve been magnificent again, thanks very much.

John: Oh, youre really welcome, Barry. Thank you. To find out how much you can get in your retirement, try our annuity calculator. And also if you liked the video, remember to like, share and subscribe.

Want that magical £1 million pension pot? You’re not the only one. Many of us wonder if reaching that seven-figure mark will really give us the life we want in retirement. Today, a £1 million pension annuity might pay you around £100,000 a year. Let’s look at that amount and see if it’s enough for the dream retirement you wish for.

The Quick Answer (For Those in a Hurry!)

If you purchase an annuity with your £1 million pension pot, you could receive

- Around £35,000 annually if you buy at age 55

- Approximately £45,000 annually if you buy at age 65

- Between £38,711 and £64,461 annually depending on the type of annuity and your circumstances

But there’s more to the story than just these numbers.

What Exactly is an Annuity, Anyway?

Before we get too deep, let’s clarify what we’re talking about. An annuity is essentially an insurance product that converts your pension pot into a guaranteed income for life. You hand over your pension savings to an insurance company, and in return, they promise to pay you a regular income until you die – regardless of how long you live.

It’s kind of like selling your pension pot in exchange for a salary that never ends. Sounds great, right? Well, as with most financial products, there’s pros and cons that we’ll explore together.

Current Annuity Rates for a £1 Million Pension (December 2024)

The most recent information from Fidelity International shows that a £1 million pension fund could give you the following in term of annuity income:

| Type of Annuity | Annual Income |

|---|---|

| Single life annuity with no annual increases | £64,461 |

| Single life annuity increasing with RPI inflation | £40,655 |

| Joint life 50% annuity with no annual increases | £60,896 |

| Joint life 50% annuity increasing with RPI | £38,711 |

Based on a healthy 60-year-old male living in London with pension savings of £1m (as of December 2024)

As you can see, the type of annuity you choose makes a HUGE difference to your retirement income!

How Age Affects Your Annuity Income

The amount of money you’ll get from an annuity depends a lot on how old you are when you buy it. Here’s the general pattern:

- At age 55: Approximately £35,000 per year

- At age 66: Around £45,000 per year

- At age 68: Could reach £50,000 per year

The simple reason for this difference is that the insurance company expects to pay you less over the next few years if you buy an older annuity. This means they can offer you a higher yearly return on the £1 million you put in.

Factors That Determine Your Annuity Rate

When you’re shopping for annuities, several factors will influence the income you’re offered:

- Your age – as discussed above, older = higher income

- Your health status – if you have health conditions, you might qualify for an “enhanced annuity” with higher rates

- Whether income increases with inflation – choosing an inflation-linked annuity means starting with a lower income

- Single vs joint life – covering your spouse/partner reduces your initial income

- Guarantee periods – ensuring payments continue for a minimum period after your death affects rates

- Current interest rates – when interest rates are higher, annuity rates tend to be better

The Pros and Cons of Annuities

Pros

- Guaranteed income for life – you can never outlive your money

- Simplicity and predictability – you know exactly what you’ll get each month

- Peace of mind – no investment decisions or market worries

- Potential for enhanced rates if you have health conditions

Cons

- Inflexibility – once set up, you can’t change the income amount

- No inflation protection by default – your income will buy less over time

- Death benefits are limited – typically, when you die, the income stops and the insurance company keeps the remaining money

- No chance to benefit from future investment growth

- No ability to withdraw lump sums for unexpected expenses

One of our clients, Margaret, told me: “I thought an annuity was the safe option, but I didn’t realize how rigid it would be. I wish I’d understood that I couldn’t increase my income when my circumstances changed.”

Is an Annuity Better Than Pension Drawdown?

Since pension freedom changes in 2015, many people now prefer pension drawdown over annuities. With drawdown, your pension stays invested and you take income as and when you need it.

For a £1 million pension pot in drawdown, you might take around £40,000+ per year (using the 4% rule) while keeping your money invested for potential growth.

The main differences are:

Pension Drawdown:

- Flexibility to vary income

- Potential for continued investment growth

- Death benefits – remaining pension can be passed to beneficiaries

- Risk of running out of money if you withdraw too much or investments perform poorly

Annuity:

- Guaranteed income for life

- No investment risk

- Simplicity – no ongoing management needed

- No flexibility to adjust income as needs change

Is £1 Million Really Enough for Retirement?

According to the Pensions and Lifetime Savings Association (PLSA), a “comfortable” retirement lifestyle costs around £43,100 a year for a single person or £59,000 for a couple.

Based on this, a £1 million pension pot converted to an annuity might provide a comfortable retirement for a single person if purchased later in life, but might fall short for a couple.

Remember, tho, your state pension will help supplement this income. For 2024/25, the full new state pension is £11,500 per year.

Could You Combine Approaches?

Many financial advisors suggest a blended approach might work best:

- Use a portion of your pension to buy an annuity that covers your essential expenses

- Keep the rest invested in drawdown for flexibility, growth potential and to leave to your family

What The Experts Recommend

I’ve talked with several retirement planning specialists about this topic, and there’s a consensus that there’s no one-size-fits-all solution.

As one advisor put it: “The right approach depends on your individual circumstances, risk tolerance, health status, and whether leaving an inheritance is important to you.”

The Bottom Line: What Should YOU Do?

If you’ve got a £1 million pension pot (or you’re working toward one), here’s what I’d suggest:

- Consider your retirement lifestyle – what annual income do you actually need?

- Think about your risk tolerance – could you handle investment fluctuations in retirement?

- Factor in your health – poorer health might mean enhanced annuity rates, but shorter retirement

- Consider your legacy wishes – is leaving money to family important?

- Get professional advice – the stakes are too high to go it alone

Remember that a £1 million pension pot is significant, but it might not provide the lavish retirement some people imagine – especially if you retire early or want inflation protection.

Final Thoughts

A £1 million annuity in the UK could pay you anywhere from around £35,000 to over £64,000 annually, depending on various factors like your age, health, and the type of annuity you choose.

Whether this is “enough” depends entirely on your personal circumstances and retirement goals. For many people, a combination of annuity and drawdown might provide the best balance of security and flexibility.

Whatever you decide, make sure you understand all your options before making what could be one of the biggest financial decisions of your life!

Have you been considering an annuity for your retirement? What factors are most important to you? We’d love to hear your thoughts in the comments below!

Disclaimer: This article provides general information only and does not constitute financial advice. Tax treatment depends on individual circumstances and all tax rules may change in the future. The figures quoted are examples only and actual annuity rates will vary.

What annuity could a smaller pension pot buy?

Your pension pot needs to have at least £5,000 in it, after you’ve taken your tax-free cash. So if you have a pension pot size of £7,000 (the minimum amount youll need to play around with our Annuity Calculator) you could take £1,750 of it as tax-free cash. This would leave you with £5,250 to spend on an annuity, giving you a guaranteed pre-tax income of around £270 a year for the rest of your life.

You can change your budget a lot when you think about the State Pension as your retirement income. Right now, you can start getting it when you turn 66. Between 2026 and 2028, the age will go up to 67, and after that, it will go up to 68. Your payments will reach you every four weeks.

In 2025/26, the full payment’s £230.25 a week. To get that, you’ll need to have paid National Insurance for at least 35 years. If you’ve paid it for less than that, you’ll get less. You can see what you’re in line for at the Government’s Check your State Pension forecast page.

How much annuity income does £50k buy?

If you’ve got £50,000 in your pension pot, you could take £12,500 of it as tax-free cash. Then you could spend £37,500 on an annuity, giving you a pre-tax income of about £2,540 a year for the rest of your life.

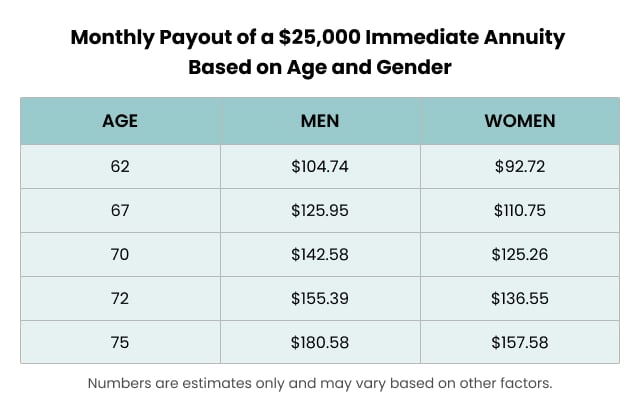

What Does A $1 Million Annuity Pay Per Month?

FAQ

Can I retire at 60 with 1 million pounds?

Depending on your retirement goals, a £1 million pension pot may be enough to sustain a comfortable lifestyle for an individual, but only with careful planning.

How much will a $1 million annuity pay per month?

The exact amount you get depends on your age, gender, the type of annuity you have, and any extra features like death or survivor benefits. As the quotes show, a $1 million annuity can provide anywhere from $4,736 to over $14,000 per month, depending on the contract structure.

Can I live off the interest of 1 million pounds?

With the way the economy is right now, you probably won’t be able to live off the interest on a £1 million savings account. But this depends on a lot of things, like where you live. While interest rates are high for the moment, that won’t always be the case.

How much will a 1 million pound annuity pay?

If you purchase an annuity, a £1m pension pot will provide an income of £35,000 per year. This assumes that you purchase an annuity at age 55 and are in good health. If you wait until you’re 68, a £1m pension pot will provide an income of £50,000 per year.

What is a 1 million annuity?

A $1 million annuity can provide a steady stream of income in retirement, which could give people who are worried about running out of money peace of mind. The amount you’ll receive from a $1 million annuity can vary based on the type of annuity, purchaser’s age, interest rates and whether the payments begin immediately or are deferred.

How much income do annuities make a year?

The income you get depends on the rate you’re offered by the annuity provider and the amount you’re converting into an annuity. For example, if you have £100,000 in your pension pot and are offered an annuity rate of 7%, you’ll get an annual income of around £7,000 a year.

How much money can a lifetime annuity make?

Lifetime annuities pay a guaranteed income regardless of how long you live for. Currently, someone who buys an annuity at age 66 could expect gross annual retirement income of up to £67,000 a year from a £1m pension fund 3. Is my pension big enough?

What is an annuity payout?

An annuity payout provides regular income from an initial investment. It can be an important part of retirement planning, offering stable income for a specific period or for life. Period Certain: Guarantees payments for a specific time period, regardless of how long you live.

Is a £1m pension enough?

A word of warning. No two retirements are the same. How much you need for retirement will depend on how much you plan to spend – and how long you plan on living for! Whilst £1m will be enough for some, it will not be enough for others. How much income would a £1m pension generate if you purchase an annuity?

Should you buy an annuity if you have a pension pot?

People just don’t seem to use them very often, instead preferring to flexibly drawdown their income (more on this later). If you purchase an annuity, a £1m pension pot will provide an income of £35,000 per year. This assumes that you purchase an annuity at age 55 and are in good health.