The average retirement age in the U.S. is 62 — a figure that’s been rising since the 1990s.

The products shown on this page are mostly or entirely from our advertising partners. They pay us when you click on one of their links and then do something on our site. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

The average retirement age in the United States is 62, according to a 2024 MassMutual survey. In 1991, it was 57; in 2002, it was 59, according to a 2022 Gallup poll.

When deciding on retirement, people consider various factors, such as how old they must be to enroll in Medicare, claim Social Security benefits, or take penalty-free distributions from their retirement accounts. Many consider several other factors, too, including anticipated lifestyle and expenses, health, qualification requirements for certain retirement benefits and how old theyll be when they feel prepared to retire.

Since 2012, the average retirement age in the U. S. has stayed relatively consistent, according to data from Gallup and MassMutual*Gallup . More in U. S. Retiring, or Planning to Retire, Later. Accessed Mar 17, 2023. View all sources.

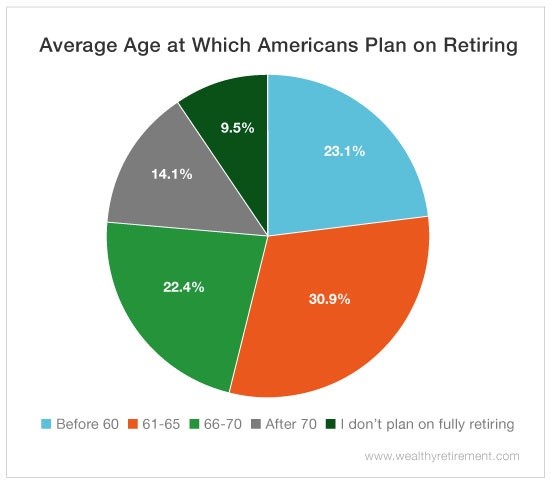

Ever wonder when most folks finally call it quits on the 9-to-5 grind? If you’re planning your golden years or just curious about what’s “normal” these days, you’re in the right place. Let’s dive into the real numbers behind retirement age in America and what they mean for you

The Short Answer: 62 is the Magic Number (But There’s More to the Story)

A survey done by Mass Mutual in 2024 found that the average age of retirement in the US is 62. It’s interesting that most retirees and people who are about to retire think that 63 is the best age to retire.

But here’s where things get interesting – what people plan and what actually happens can be two different stories. About 11,200 Americans exit the workforce every single day, and many end up retiring earlier than they expected.

Retirement Age is Creeping Up

Our parents and grandparents might have retired earlier than we will. Check out these trends:

- In 1991, the average retirement age was just 57

- By 2021, it had increased to 65 for men and 62 for women

- Early retirement (ages 50-54) has dropped from 9% to 6%

- Early retirement (ages 55-59) has decreased from 19% to 11%

This ain’t your grandpa’s retirement timeline! People are working longer these days, and there are some pretty clear reasons why.

Men vs. Women: The Retirement Gender Gap

Turns out, there’s a gender gap in retirement timing too. See how the age of retirement has changed through the years:

| Year | Average Retirement Age for Men | Average Retirement Age for Women |

|---|---|---|

| 1992 | 62 | 59 |

| 2001 | 63 | 60 |

| 2010 | 64 | 62 |

| 2016 | 65 | 63 |

| 2021 | 65 | 62 |

Women typically retire earlier than men, though both genders are working longer than they used to.

Education Makes a Big Difference

Your diploma might be deciding when you retire. Research from the Center for Retirement Research shows:

- Male college graduates retire at around 65.7 years old

- Male high school graduates retire earlier at about 62.8

- Similar patterns exist for women

Why the difference? White-collar jobs (typically filled by college grads) are less physically demanding, allowing people to work longer. Meanwhile, those with less education often work in more physically demanding jobs and may have worse health, pushing them into earlier retirement.

Geography Matters Too

Where you live can significantly impact when you retire. Some states have significantly different average retirement ages:

- Washington D.C.: 67 (highest)

- Massachusetts, Hawaii, South Dakota: 66

- Iowa, Kansas, Maryland, Vermont, Texas (and others): 65

- Arizona, Missouri, Nevada (and others): 63

- Alaska, West Virginia, Michigan: 61-62 (lowest)

Southern states generally have lower average retirement ages compared to Northeastern states.

Race and Retirement: An Unequal Picture

There are noticeable differences in retirement patterns across racial and ethnic groups:

- 65% of Hispanic people retire at age 61 or earlier

- 56% of Black people retire at age 61 or earlier

- 48% of white people retire at age 61 or earlier

Minority groups often have less retirement savings, even though they retire earlier on average. Only 2035 percent of Hispanic families and 2041 percent of Black families have retirement savings in 401(k) or IRA accounts, while 2068 percent of white families do.

Common reasons for earlier retirement among minority groups include health problems, family caregiving responsibilities, and lack of available work.

Why Are We Working Longer?

Several factors are pushing retirement ages higher:

- Social Security Changes – The full retirement age has gradually increased from 65 to 67 (for those born in 1960 or later)

- Longer Life Expectancy – People are living longer, meaning more years in retirement that need to be funded

- Economic Uncertainty – The Great Recession of 2008, COVID crisis, and recent inflation have eaten into many people’s savings

- Inadequate Savings – Only 68% of workers and 74% of retirees feel confident they’ll have enough money for a comfortable retirement

Planned vs. Actual: The Retirement Reality Gap

Here’s something interesting: there’s often a gap between when people plan to retire and when they actually retire. In 2022:

- Non-retirees expected to work until age 66

- Retirees reported an actual average retirement age of 61

This five-year gap isn’t always good news – it often reflects unexpected circumstances rather than early financial freedom:

- 31% retire early due to health problems or disability

- 32% retire early because of changes at their company (layoffs, downsizing, etc.)

When Should YOU Retire?

The “right” retirement age is super personal. Here are some key things to consider:

Financial Readiness

- Do you have enough savings to support your desired lifestyle?

- Will your Social Security and pension (if you have one) cover your basic needs?

- Have you paid off major debts?

Social Security Timing

Starting Social Security at different ages affects your benefits:

| Age | Benefit Reduction | Monthly Benefit (Based on $2,000 at age 67) |

|---|---|---|

| 62 | 30% | $1,400 |

| 63 | 25% | $1,500 |

| 64 | 20% | $1,600 |

| 65 | 13.3% | $1,733 |

| 66 | 6.7% | $1,867 |

| 67 | 0% | $2,000 |

Remember: Medicare doesn’t kick in until 65, even if you retire earlier!

Health Status

- Are you physically able to continue working?

- How’s your family health history? (Affects life expectancy)

- Would your job negatively impact your health if you continue?

Personal Goals and Lifestyle

- What do you want your retirement to look like?

- Are there things you want to do while you’re still young and healthy?

- Does your partner’s retirement timeline align with yours?

Early Retirement: Dream or Disaster?

Retiring early (before 62) is totally possible, but it’s becoming less common. Only 11% of Americans now retire between ages 55-59, down from 15% previously.

Early retirement challenges:

- Can’t claim Social Security until 62

- Penalties for withdrawing from retirement accounts before 59½

- Need health insurance to bridge the gap until Medicare at 65

- More years of retirement to fund

- Potential boredom or loss of purpose

Early retirement benefits:

- More healthy years to enjoy retirement

- Time to pursue passions, travel, and hobbies

- Reduced stress and better quality of life

- Opportunity for part-time work or new ventures

Are You on Track? Quick Retirement Readiness Check

We all wanna know if we’re on the right track. Here’s a quick way to check:

- Estimate your annual retirement expenses (including healthcare!)

- Multiply by expected years in retirement (25-30 is a good starting point)

- Subtract expected Social Security and pension income

- Compare with your current retirement savings

If there’s a gap, don’t panic! You’ve got options:

- Increase your savings rate

- Work a few more years

- Adjust your retirement lifestyle expectations

- Consider a part-time job in retirement

- Look into catch-up contributions (available after age 50)

The Bottom Line

The average American retires at 62, but that number is rising and varies widely based on gender, education, location, and individual circumstances. Your personal retirement age should be based on financial readiness, health, goals, and what makes sense for your unique situation.

Whatever age you choose to retire, the most important thing is to start planning early. The sooner you start saving and planning, the more options you’ll have when it comes time to decide whether to keep working or start that next exciting chapter of life.

P.S. – I’m not a financial advisor, just a fellow retirement planner trying to navigate these waters too! Be sure to consult with a professional for personalized advice.

Full retirement age for Social Security

|

Year you were born |

Full retirement age |

If you start receiving benefits at 62, your retirement benefit is reduced by… |

|---|---|---|

|

1943 through 1954 |

66. |

25%. |

|

1955 |

66 and 2 months. |

25.83%. |

|

1956 |

66 and 4 months. |

26.67%. |

|

1957 |

66 and 6 months. |

27.5%. |

|

1958 |

66 and 8 months. |

28.33%. |

|

1959 |

66 and 10 months. |

29.17%. |

|

1960 and later |

67. |

30%. |

Social Security

Most people can begin taking Social Security retirement benefits at 62. However, claiming Social Security at 62 means receiving significantly reduced benefits.

Different people have different full retirement ages. Your full retirement age is the age at which you are entitled to 100% of your Social Security retirement benefit. So waiting until after your full retirement age to claim Social Security retirement benefits could net you an even bigger check.

Did you know that Medicare Part B premiums are usually automatically deducted from your Social Security checks? Learn more about how much Medicare actually costs.

How Much Does the Average Single American Need for Retirement?

FAQ

What is the most common age to retire?

The median retirement age in the United States is 62, with a significant portion of workers retiring earlier than planned due to health or job loss, even though many expect to work longer. Key ages like 62 for Social Security eligibility and 65 for Medicare often influence the decision to stop working, though the ideal age varies based on personal circumstances.

Is $600,000 enough to retire at 70?

And you can increase your benefits if you’re able to delay claiming until age 70. It’s also important to consider overall health and how that can impact your retirement plans. If you stay healthy and don’t need long-term care, $600,000 might be enough to live on in retirement.

Can I retire at 62 with $400,000 in 401k?

Can You Retire at 62 With $400,000 in a 401(k)? You can retire early with $400,000, but it won’t be easy. If you have the option of working and saving for a few more years, it will likely give you a significantly more comfortable retirement.

Is $80,000 a year enough to retire?

Whether $80,000 per year is enough for retirement depends on individual expenses and lifestyle, but it’s a strong starting point, often aligning with the 80% rule where retirees aim to replace 70-80% of their pre-retirement income. To determine your specific needs, calculate your estimated retirement expenses, consider sources of income like Social Security, and factor in inflation.

What is the average retirement age in the United States?

The average retirement age in U. S. is 62 years old, with the average retirement age across all states spanning from 61 to 66 years old. The Social Security Act says that you have to be 65 years old to retire and get full retirement benefits. However, this age will keep going up.

What is a good retirement age?

The full retirement age is 66 if you were born from 1943 to 1954, and it increases gradually if you were born between 1955 and 1960 until it reaches 67. Among workers planning for retirement, 69% expect that the official retirement age will be higher by the time they are ready to retire, according to data from Talker Research.

What is the minimum age to retire?

The Social Security Act sets the minimum age to retire at 65 to receive full retirement benefits, although the minimum retirement age will continue to rise. Some choose to retire at 65 as this is when Medicaid becomes available, and there’s no longer a need to receive health insurance through employment.

What is the expected retirement length in the United States?

The expected retirement length in the U.S. is 18.6 years for men and 21.3 years for women. Retirement, and the average retirement age, is a hot topic. There’s been talk of pushing the full retirement age for Social Security from 67 to 69, which would cut benefits for a significant number of Americans.

What is my full retirement age?

Your full retirement age depends on when you were born. If you were born before 1960, your full retirement age is 66, while if you were born in 1960 or later, your full retirement age is 67. No additional income is derived by waiting until after age 70 to start claiming Social Security benefits. 2

Will retirement age be higher?

Among workers planning for retirement, 69% expect that the official retirement age will be higher by the time they are ready to retire, according to data from Talker Research. What Is the Average Retirement Savings Balance by Age?