Check to see what the tax effects will be before you make the change. Part of the series: Strategies to Get the Most Out of Your 401(k)

If you are considering leaving a job and have a 401(k) plan, you need to stay on top of the various rollover options for your workplace retirement account. One of those options is rolling over a traditional pretax 401(k) into a Roth individual retirement account (Roth IRA). This can be a very attractive option, especially if your future earnings will be high enough to knock into the ceiling placed on Roth account contributions by the Internal Revenue Service (IRS).

Regardless of the size of your earnings, you need to do the rollover strictly by the rules to avoid an unexpected tax burden. Since you haven’t paid income taxes on that money in your traditional pretax 401(k) account, you will owe taxes for the year when you roll it over into a Roth IRA. However, once youve paid the taxes and your money is in the Roth IRA, you wont pay taxes on it again at withdrawal time.

Can you actually convert your 401(k) to a Roth IRA after you’ve already retired? Absolutely!

Despite what many folks believe there’s no age limit for converting your traditional 401(k) into a Roth IRA. In fact retirement might actually be the perfect time to make this financial move. I’ve worked with many clients who’ve successfully done this well into their golden years.

Let’s dive into everything you need to know about post-retirement 401(k) to Roth IRA conversions – the benefits potential pitfalls and some strategies to make it work for you.

Why Convert Your 401(k) to a Roth IRA After Retirement?

You may be wondering, “Why would I want to mess with my retirement accounts now that I’m retired?” That’s a good question! But there are several strong reasons

1. Tax-Free Growth and Withdrawals

Once your money is in a Roth IRA, it grows completely tax-free. And when you withdraw that money (following the rules), you don’t pay a single penny in taxes. That’s right – zero taxes on qualified withdrawals!

2. No Required Minimum Distributions (RMDs)

Unlike traditional 401(k)s and IRAs, Roth IRAs don’t have Required Minimum Distributions at age 73. This means you’re not forced to withdraw money you don’t need, giving you more control over your retirement funds.

3. Better Estate Planning

Roth IRAs have a lot of benefits if you care about leaving money to your heirs. If the account rules are followed, your beneficiaries won’t have to pay income tax on withdrawals from a Roth IRA you leave them. This is not the case with traditional retirement accounts.

4. Protection for Your Surviving Spouse

This is a big one that people often overlook. When one spouse dies, the other spouse no longer files taxes with their partner but as a single person. They may have to pay more in taxes now, even if they make less money. Switching to a Roth can lower your spouse’s tax bill.

5. Keeping Medicare Premiums Lower

Your taxable income affects your Medicare premiums through something called IRMAA (Income-Related Monthly Adjustment Amount). In 2024, if your income exceeds $103,000 for single filers or $206,000 for couples, your Medicare premiums go up. Roth withdrawals don’t count toward this threshold!

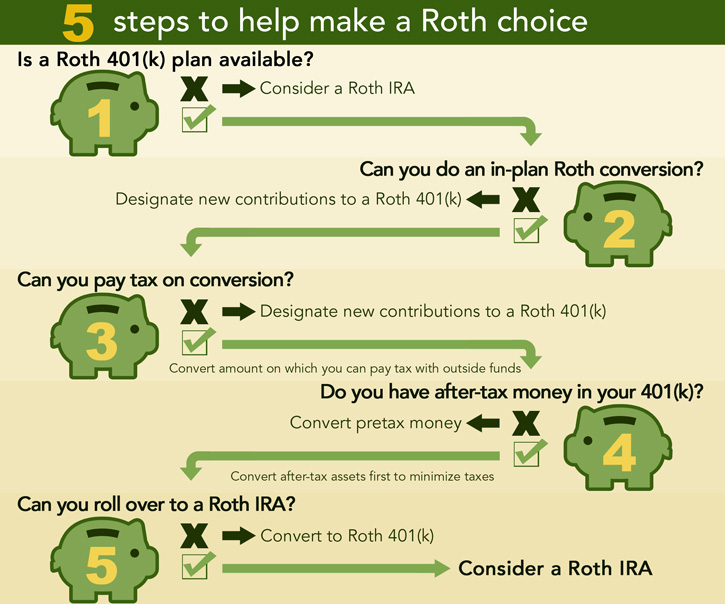

The Three Key Tests Before Converting

Before you rush to convert your 401(k), there are three important tests to consider, as outlined by financial experts:

Test 1: How Will You Pay the Tax?

When you convert pre-tax retirement funds to a Roth, you gotta pay income tax on the amount converted. Ideally, you’d pay this tax using money from outside your retirement accounts.

What’s the reason? If you use your retirement funds to pay the tax, your new Roth account will have less money growing tax-free. You might also have to pay an extra 10% penalty on the part that was used for taxes if you are under 20% of the tax threshold.

Test 2: How Do Your Current Tax Rates Compare to Future Rates?

The ideal time to convert is when your current tax rate is lower than what you expect in the future. Many retirees find themselves in a “trough” period – after retirement but before Social Security benefits and RMDs kick in – when their income and tax rates are temporarily lower.

Test 3: When Do You Plan to Use the Money?

This is super important! The longer you can leave the money in the Roth IRA after conversion, the more time it has to grow tax-free and overcome the upfront tax cost.

If you’re gonna need the money within a year or two, a conversion might not make sense. But if it’ll sit there growing for 5, 10, or even 20+ years, the math starts looking a lot better.

How to Actually Do the Conversion

The mechanics aren’t overly complicated, but you need to follow the rules carefully:

-

Contact your 401(k) plan administrator and explain that you want to roll over your 401(k) to a Roth IRA.

-

Open a Roth IRA if you don’t already have one. You can do this through most banks, brokerages, or online investment platforms.

-

Request a direct rollover (also called a trustee-to-trustee transfer). This is the safest way to move the money without triggering unwanted penalties.

-

Be prepared for the tax bill. The amount you convert will be added to your taxable income for the year.

-

Consider a partial conversion rather than moving all your money at once, which could push you into a higher tax bracket.

Converting Even If You’ve Started RMDs

Many people wonder if they can still convert to a Roth after they’ve begun taking Required Minimum Distributions (RMDs). The answer is YES – but there’s a catch.

You must first take your RMD for the year before doing the conversion. The RMD itself cannot be converted to a Roth IRA. However, after satisfying your RMD requirement, you can convert any additional amount from your traditional IRA or 401(k) to a Roth.

Should YOU Convert? Real-world Considerations

Is a Roth conversion right for you? Here are some situations where it might make sense:

Good Candidates for Conversion:

- You expect to be in a higher tax bracket in the future

- You have cash outside retirement accounts to pay the conversion tax

- You want to leave tax-free money to your heirs

- You’re concerned about your spouse’s tax situation after you’re gone

- You don’t need the money for 5+ years

- You’re in a temporarily lower tax bracket (like between retirement and starting Social Security)

Maybe Not the Best Idea If:

- You’re already in a high tax bracket (32% or above)

- You’ll need the money soon

- You don’t have outside funds to pay the conversion tax

- You expect to be in a much lower tax bracket in retirement

- Your primary goal is maximizing income rather than legacy planning

Strategic Approaches to Conversion

Rather than converting your entire 401(k) at once, consider these approaches:

Partial Conversions

Convert just enough each year to “fill up” your current tax bracket without bumping into the next one. This strategy, sometimes called “bracket filling,” can minimize your overall tax burden.

Timing Your Conversion

The “trough years” between retirement and age 73 (when RMDs begin) often represent your lowest income years and can be ideal for conversion.

Special Considerations for After-Tax Contributions

If you made after-tax contributions to your 401(k), you may be able to allocate those funds directly to a Roth IRA without paying additional taxes. This can be complicated, so consult with a tax professional.

Common Questions About 401(k) to Roth Conversions

Can I still convert if I’m already taking RMDs?

Yes! Just make sure you take your required minimum distribution for the year first.

Is there an age limit for Roth conversions?

Nope! You can convert at any age, even well into retirement.

Will a conversion affect my Medicare premiums?

Possibly. Since the conversion amount counts as income in the year you convert, it could temporarily increase your Medicare premiums through IRMAA. However, future withdrawals from the Roth won’t affect your premiums.

Can I convert just a portion of my 401(k)?

Absolutely. In fact, partial conversions spread over multiple years are often the most tax-efficient approach.

What about the five-year rule?

Roth IRAs have a five-year rule that applies to both contributions and conversions. For conversions, you must wait five years or until age 59½ (whichever comes later) to withdraw the converted amounts without penalty. However, this rule applies separately to each conversion.

Real Example: How Mary Saved Thousands in Retirement

Let me share a quick story about my client Mary (name changed for privacy). She retired at 68 with a substantial 401(k). After analyzing her situation, we realized that converting $50,000 per year for five years would keep her in the 22% tax bracket while significantly reducing her future RMDs.

The result? Mary will save an estimated $87,000 in lifetime taxes, her Medicare premiums won’t increase dramatically when RMDs kick in, and she’s set up her children to receive tax-free inheritances.

Final Thoughts

Converting your 401(k) to a Roth IRA after retirement can be a smart financial move for many retirees, but it’s not a one-size-fits-all solution. The key is careful planning and understanding your specific situation.

I always recommend working with a qualified financial advisor who understands tax strategies and retirement planning. They can help you run the numbers and determine if a conversion makes sense for your unique circumstances.

Remember, retirement planning doesn’t stop when you retire – it’s an ongoing process of optimization, and Roth conversions are just one powerful tool in your financial toolkit.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Always consult with a qualified financial professional before making significant changes to your retirement accounts.

When the Five-Year Rule Applies

When funds are rolled over from a Roth 401(k) to an existing Roth IRA, the rolled-over funds inherit the exact timing as the Roth IRA. We can say that the holding period for the IRA includes all the money in it, even the money that was rolled over from the Roth 401(k).

If you do not have an existing Roth IRA and need to establish one for the rollover, the five-year period begins the year the new Roth IRA is opened, regardless of how long you have been contributing to the Roth 401(k).

If you roll a traditional 401(k) over to a Roth IRA, the clock starts ticking from the date when those funds hit the Roth. Withdrawing earnings early, typically before age 59½, could incur taxes and a 10% penalty. Withdrawing converted funds early could incur a 10% penalty.

The rules governing the early withdrawal of funds in a converted Roth IRA can be confusing. There are some exceptions to the tax and penalty rules that depend on whether you are taking out earnings or your original after-tax contributions. There are also certain qualifying life events, notably a job loss, that can change the picture. Check the rules before withdrawing funds early.

Rolling over your 401(k) to a new Roth IRA is not a good choice if you anticipate having to withdraw money in the near future—more specifically, within five years of opening the new account.

Avoid Cashing Out

Cashing out your account, in whole or in part—whether the account is traditional or Roth—is usually a mistake.

- If you have a traditional 401(k) plan, you will have to pay taxes on all of your contributions, plus the 2010% penalty for taking money out early if you are under age 509.

- Regarding a Roth 401(k), you will have to pay taxes on any earnings you take out, and you may be charged a penalty for taking money out too early if you are under the age of 59 and have not had the account for five years.

401(k) funds are not the only company retirement plan assets eligible for rollover. The 403(b) and 457(b) plans for public-sector and nonprofit employees can be converted into Roth IRAs as well.