What Exactly Is a Pension Refund?

A pension refund is simply getting back the money you’ve contributed to your retirement plan when you leave your job before retirement. Instead of waiting until retirement age to access these funds, you’re essentially cashing out early.

This choice has caused a lot of people to get lost, so let me explain it in simple terms. When you work for a company with a pension plan, like the government, you usually put some of your pay into that plan every pay period. What if you decide to quit that job? You might be able to get those contributions back.

But here’s the thing – a pension refund isn’t just a straightforward transaction. It comes with significant consequences for your long-term financial health.

Who Can Get a Pension Refund?

Not everyone can or should get a pension refund. Your eligibility typically depends on:

- Length of service: Many plans allow refunds if you leave before a certain number of years of service

- Type of plan: Government pension plans (like FERS for federal employees or state plans like OPERS) have their own specific rules

- Vesting status: Whether you’ve worked long enough to be entitled to employer contributions

For example, if you’re a federal worker who quits, you must have been out of work for at least 31 days in a row before you can get your money back. You also can’t be eligible for an immediate annuity and can’t be stopped by a court order.

How a Pension Refund Works

When you request a refund, you’ll typically receive:

- 100% of your eligible employee contributions

- Any interest those contributions have earned

- Possibly an additional percentage based on your years of service

Take OPERS’s (Ohio Public Employees Retirement System) Traditional Pension Plan as an example. The extra amount varies:

| Years of Qualified Service Credit | Additional Amount |

|---|---|

| Less than 5 years | 0% |

| 5-10 years | 33% |

| More than 10 years | 67% |

The process usually involves:

- Confirming your eligibility

- Contacting your pension provider

- Completing necessary paperwork

- Waiting for processing

- Receiving your payment (usually direct deposit)

The Tax Consequences You Can’t Ignore

A lot of people don’t think about the tax effects of getting a pension refund. The following things will happen if you don’t move the money to another retirement account:

- Income tax: The refund will be taxed as ordinary income

- Early withdrawal penalty: If you’re under 59½, you might pay an additional 10% penalty

- Tax withholding: Your plan might automatically withhold 20% for federal taxes

In some countries like the UK. pension refunds face even steeper taxation

- First £20,000 of contributions: Taxed at 20%

- Contributions above £20,000: Taxed at 50%

These tax hits can significantly reduce the amount you actually receive I’ve seen people shocked when their expected refund was much smaller than anticipated because they didn’t account for taxes,

The Pros of Taking a Pension Refund

While I’m generally not a huge fan of pension refunds, there are some situations where they might make sense:

-

Short service period: If you have less than five years of civilian service and don’t plan to return to that employer, a refund might be reasonable since you might not qualify for an annuity anyway.

-

Immediate financial need: Sometimes life throws curveballs, and you need access to funds for emergencies.

-

Better investment opportunities: If you’re confident you can invest the money and earn a higher return than the pension would provide (this is risky and requires investment knowledge).

-

Simple consolidation: It can simplify your financial picture if you have multiple small pension accounts.

The (Mostly) Cons of Taking a Pension Refund

Now here’s where I need to be brutally honest – in most cases, taking a pension refund is NOT in your best financial interest. Here’s why:

-

Loss of future benefits: You’re giving up a guaranteed income stream in retirement.

-

Surrender of employer contributions: In many cases, you only get YOUR contributions back, not what your employer put in.

-

Missing out on survivor benefits: Your spouse may lose potential survivor benefits if you pass away.

-

Healthcare implications: Some pension plans provide access to healthcare benefits in retirement – you could lose these.

-

Costly to rejoin: If you return to that employer later, you’ll usually have to repay the refund PLUS interest to restore your service credit.

-

Tax consequences: As mentioned above, the tax hit can be substantial.

For federal employees specifically, taking a refund voids any retirement options, including survivor benefits. This ineligibility for a survivor benefit generally means ineligibility for continued Federal Employees Health Benefits coverage for your survivor after your death.

Alternatives to Consider Before Taking a Refund

Before you pull the trigger on a pension refund, consider these alternatives:

1. Leave Your Money in the Plan

Leaving your account on deposit with your pension system often has significant benefits:

- No penalties or fees

- Continued interest accrual

- Potential eligibility for retirement benefits later

- Preservation of survivor benefits

- Possible disability benefits protection

For example, with OPERS, if you have five or more years of service credit, you may qualify for retirement benefits later depending on your age and retirement group. With at least 18 months of contributing service credit, you’ve earned survivor benefits for your loved ones.

2. Transfer Your Pension

You might be able to transfer your pension to a different scheme that offers better benefits or investment options.

3. Roll Over to an IRA

Rolling your pension into an Individual Retirement Account preserves the tax-advantaged status and gives you more investment control.

4. Consider a Phased Retirement

Some plans allow for a phased retirement where you gradually reduce your working hours while drawing on your pension.

Real-World Example: Federal Employee Considerations

Let’s consider a specific scenario for federal employees. If you separate from federal employment and are considering a refund, here’s what you should know:

A refund might make sense if:

- You have less than five years of civilian service and don’t plan to return to federal employment

- You have five+ years of service, don’t plan to return, AND believe you can invest the funds to exceed the value of the deferred annuity (a big gamble)

A refund might NOT make sense if:

- You might be re-employed by the federal government (you’ll need to make a redeposit with interest)

- You have at least five years of service and your potential deferred annuity exceeds the refund value

Making Your Decision: Questions to Ask Yourself

Before requesting a refund, ask yourself:

- How many years of service do I have?

- What’s the value of my potential future pension?

- Do I expect to return to this employer?

- Do I have other retirement savings?

- How will I handle the tax implications?

- What’s my current financial situation?

- What would happen to my spouse/dependents if I died?

The Bottom Line: Think Long-Term

Look, I get it. When you leave a job, that lump sum refund can look mighty tempting. It’s YOURS, after all! But I’ve seen too many people regret this decision when they reach retirement age.

Remember – pensions are increasingly rare. They provide guaranteed income for life, which is an incredible benefit in an uncertain world. Trading that security for a one-time payout often doesn’t make financial sense in the long run.

My advice? Unless you have a compelling reason and have done the math carefully, consider leaving your pension intact. Your future self will probably thank you.

If you’re still unsure, talk to a financial advisor who specializes in retirement planning. They can help you understand the specific implications for your situation and calculate whether a refund truly makes sense for you.

Have you considered a pension refund? What factors influenced your decision? I’d love to hear your experiences in the comments!

Have you left your job and need to know your options for your account balance?

When a member loses their job, they have three choices about their retirement account: (1) retire if they are eligible, (2) leave their contributions in the account until they are eligible to retire, or (3) get their account balance back.

If a Tier 1 member wants to get their account balance back, they will get their individual retirement contributions back along with any interest that has built up. However, they will not get their employer contributions back.

Refunds may be paid directly to the member or can be rolled over to another qualified retirement plan or Individual Retirement Account (IRA). If a member elects to receive a direct payment, KPPA is required to withhold 20% for federal income taxes. The amount that was taken out is not a penalty tax; it will be used to pay federal taxes for the year that the refund is given. Additional taxes due to age or other factors may also apply if a member chooses to receive a direct payment.

By taking a refund, members forfeit eligibility for future benefits including health insurance and the $5,000 death benefit.

In order to process a refund of their accumulated account balance, members must complete a Form 4525, Application for Refund of Member Contributions and Direct Rollover/Direct Payment Selection. The members employer is also required to report the termination date on the monthly report to KPPA. A refund cannot be issued until all information is received. A refund cannot be processed until at least 45 days following the termination date, provided all required information has been submitted by the member and their employer. Members interested in taking a refund of their account balance may download Form 4525 here or call our office to request a copy.

If a member returns to employment with the same employer in any capacity, or a different employer that participates in the same retirement system for which the member has applied for the refund, within 45 days of terminating the employment, the member will become ineligible to receive the refund and will be required to pay back the refund if payment has been issued.

If a member goes to work for a participating employer at a later date, the member may be eligible to purchase their refunded service. The purchase will not reestablish the members original participation date which determines the benefit tier they are in. Tier 1 members will only receive credit for the months of service hey purchase.

Members interested in taking a refund should contact KPPA for more information at 502-696-8800, Toll-Free at 800-928-4646, or complete the request below to obtain a form via mail.

Please do not include any sensitive information, such as your Social Security Number (SSN), in any email correspondence. If your request requires that you give us confidential information, call our office.

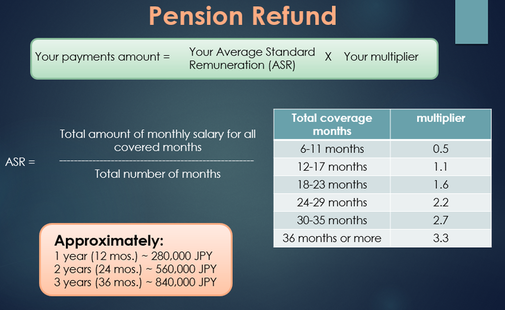

Why Getting Your FERS Pension Refund Makes Sense

FAQ

How does a pension refund work?

You can get your money back if you’ve paid into the scheme for at least three months but less than two years since you joined or were automatically enrolled. You also have the option of transferring your benefits to another pension scheme instead of getting a refund.

What is a pension refund beneficiary?

The refund beneficiary designation is very important if you have not vested. If you die before you are vested and your death is not duty-related, your employee contributions plus interest are paid in a lump sum to your designated refund beneficiary.

How much pension refund will I get?

The refund will be less than the pension contributions you have paid. By law, we may have to take two things away: one to pay for putting you back into the State Second Pension Scheme (if you have paid contracted out rate contributions), and the other to cover your income tax.

Do you get pension money back if you quit?

What Happens to Your Pension When You Leave a Job? Exiting a job ushers in two primary possibilities for your pension: Receiving a lump-sum payout or keeping the money in the current plan. Keep in mind that you may not have an option depending on the terms of your plan.

Can I get a refund of my pension contributions?

Usually, your pension contributions will remain in the pot until you’re eligible to access them, often around the pension age. However, in some cases, you may be able to request a refund of the contributions you’ve paid.

Can I get a pension refund if I leave a company?

A pension refund is a repayment of the pension contributions you’ve made to a given pension fund. If I leave a company, can I get my pension contributions back? Those who have chosen to leave their workplace pension scheme within 2 years of joining are entitled to a refund of the pension contributions paid over that time period.

How does a UK pension refund work?

The pension refund is sent to the person’s bank account or payment order after it has been processed. It may have National Insurance and income tax taken out before it gets sent. When a UK pension refund is given depends on the pension plan and how quickly the employer or pension provider responds.

How do I get my pension refunded?

If you set up the pension yourself, your provider might also hold some money back to cover their investment costs. If you’d like your pension contributions refunded, ask your pension provider what information they need. This often means completing a form. Your provider will check you’re eligible and arrange for any payment to be made.

What if I receive a refund of my FERS retirement contributions?

You can ask that your retirement contributions be returned to you in a lump sum payment, or you can wait until you are retirement age to apply for monthly retirement benefit payments. Receiving a refund of your FERS retirement deductions will eliminate your rights to an annuity for the period of service that the refund covers.

When should I get a UK pension refund?

The timing of a UK pension refund depends on the pension scheme and the employer or pension provider’s responsiveness. Refunds may affect future retirement benefits; therefore, individuals should also consider transferring pension rights or connecting membership before seeking a refund.