Traditional individual retirement accounts (IRAs) and Roth IRAs are both widely used investment vehicles for workers trying to accumulate long-term assets. However, the way these two accounts work is different, with each having its own advantages and disadvantages. While they each offer tax benefits, there are limits to how much you can contribute, and these limits can change every year.

Are you thinking about opening an IRA for retirement savings? While IRAs offer excellent tax advantages, they’re not perfect for everyone Before jumping in, you should understand both sides of the coin

I’ve spent years studying retirement plans and want to talk about the bad things that can happen that financial advisors usually don’t talk about. These disadvantages might significantly impact your financial future if ignored.

The Major Disadvantages of IRAs You Need to Know

1. Strict Contribution Limits Hinder Wealth Building

One of the biggest drawbacks of IRAs is their low annual contribution limits. For 2025, you can only contribute

- $7,000 per year to a traditional or Roth IRA

- $8,000 if you’re age 50 or older (catch-up contribution)

401(k) plans, on the other hand, let you put up to $23,500 ($30,500 if you’re 50) into them each year. Because of this big difference, IRAs might not be enough to build up a lot of money for retirement.

As Financial Samurai points out, “What will $7,000 do for your retirement? A max contribution of $7,000 a year isn’t going to get you to the promised land.”

2. Early Withdrawal Penalties Can Be Costly

Need access to your IRA funds before retirement? Be prepared to pay up:

- Traditional IRA: 10% penalty plus income tax on early withdrawals before age 59½

- Roth IRA: 10% penalty plus income tax on withdrawn earnings (not contributions) before age 59½

While there are some exceptions to these penalties (first-time home purchase, qualified education expenses, etc.), the restrictions can be problematic if you face financial emergencies.

According to Investopedia, “With the traditional IRA, you face a 10% penalty on top of the taxes owed for any withdrawals before age 59½.”

3. Required Minimum Distributions (RMDs) Force Your Hand

Traditional IRAs come with mandatory withdrawals starting at age 73. These required minimum distributions (RMDs) mean:

- You must withdraw a minimum amount annually whether you need the money or not

- You’ll pay income tax on these forced withdrawals

- Your tax bracket might increase due to these mandatory distributions

This lack of control over your money can throw off your well-thought-out plans for retirement. One benefit of Roth IRAs over traditional IRAs is that the original owner doesn’t have to make RMDs while they are still alive.

4. Income Limitations Restrict Who Can Contribute

Not everyone qualifies to contribute to an IRA, particularly Roth IRAs:

2025 Roth IRA Income Limits:

| Filing Status | Full Contribution Below | Partial Contribution | No Contribution Above |

|---|---|---|---|

| Single | $150,000 | $150,000-$165,000 | $165,000 |

| Married Filing Jointly | $236,000 | $236,000-$246,000 | $246,000 |

Traditional IRAs have income limitations too—not for contributing, but for getting the tax deduction:

2025 Traditional IRA Deduction Limits (if covered by workplace retirement plan):

| Filing Status | Full Deduction Below | Partial Deduction | No Deduction Above |

|---|---|---|---|

| Single | $79,000 | $79,000-$89,000 | $89,000 |

| Married Filing Jointly | $126,000 | $126,000-$146,000 | $146,000 |

This bias based on income seems unfair, and it can make planning for retirement harder for people who make more money.

5. Up-Front Taxes on Roth IRAs Can Be a Bad Bet

With Roth IRAs, you pay taxes now for tax-free withdrawals later. But this strategy can backfire:

- You’re giving the government money earlier, losing potential growth on those tax dollars

- You’re betting your tax rate in retirement will be higher than it is now

- If you die before retirement, you’ll have paid taxes without ever receiving the benefit

As Financial Samurai bluntly states: “You allow the government to take more of your money sooner rather than later. The government is inefficient with your money.”

6. Traditional IRAs Tax Your Future Success

The traditional IRA effectively “punishes” successful investors by:

- Taxing all your investment growth at ordinary income rates, not lower capital gains rates

- Creating potentially higher tax brackets in retirement if your investments perform well

- Forcing you to pay taxes on money that could have continued growing tax-deferred

This means your success as an investor actually creates a larger tax burden down the road.

7. Complexity in Planning and Rules

IRAs come with complex rules that can trip up even financially savvy individuals:

- Contribution deadlines and methods

- Conversion strategies (like backdoor Roth)

- Understanding tax implications of various actions

- Keeping track of basis in non-deductible IRAs

Navigating these complexities often requires professional help, adding to the effective cost of maintaining these accounts.

8. Limited Investment Options Compared to Taxable Accounts

While IRAs offer more investment choices than 401(k)s, they still have restrictions:

- No life insurance

- No collectibles (art, antiques, stamps, etc.)

- Limitations on certain types of alternative investments

- Prohibited transactions that can disqualify your entire IRA

Taxable brokerage accounts don’t have these restrictions, giving you more freedom to invest as you choose.

9. State Tax Complications

If you live in a high-tax state during your working years and plan to move to a no-income-tax state for retirement, a traditional IRA could be disadvantageous:

- You pay high state taxes on contributions if they’re not deductible at the state level

- You lose the opportunity to avoid state taxes by moving before withdrawing funds

As Financial Samurai notes, “You eliminate the benefits of moving to a lower-cost state to save on taxes” when using a Roth IRA.

10. Estate Planning Complications

IRAs can create challenges for estate planning:

- Traditional IRAs pass income tax liability to your heirs

- Complex rules for inherited IRAs, particularly for non-spouse beneficiaries

- Potential double taxation with estate taxes and income taxes

- The SECURE Act eliminated the “stretch IRA” strategy for most non-spouse beneficiaries

Who Should Reconsider IRAs?

Based on these disadvantages, IRAs may not be ideal for:

- High-income earners who won’t get tax deductions or direct Roth contributions

- Young investors who might need access to funds before retirement

- Self-employed individuals (who might be better served by SEP IRAs or Solo 401(k)s)

- Those in high tax brackets now who expect lower rates in retirement

- Individuals with unpredictable income who can’t reliably contribute

Alternatives to Consider

If these IRA disadvantages concern you, consider these alternatives:

- 401(k)/403(b) – Higher contribution limits and possible employer match

- HSA accounts – Triple tax advantage if used for healthcare

- Taxable brokerage accounts – No contribution limits or withdrawal penalties

- Real estate investments – Tax advantages through depreciation and 1031 exchanges

- Whole life insurance – Tax-free death benefit and potential cash value growth

The Bottom Line: Balance is Key

I’m not saying IRAs are bad—they have significant advantages too. But understanding the disadvantages helps you make a more informed decision. The best retirement strategy often involves diversifying across different account types to maximize advantages and minimize disadvantages.

For most people, maxing out employer-sponsored retirement plans like 401(k)s before considering IRAs makes the most sense. And if you do choose an IRA, be strategic about whether traditional or Roth works better for your specific situation.

The key is balance and understanding how these accounts fit into your overall financial picture. Don’t let the tax advantages blind you to the potential drawbacks that could impact your financial freedom down the road.

Have you experienced any of these IRA disadvantages firsthand? I’d love to hear your thoughts and experiences in the comments below!

Benefits of Traditional and Roth IRAs

IRAs offer several distinct advantages, including the following:

Penalties

Since the IRA is intended for retirement, there are often certain penalties if you take out your money before retirement age. With the traditional IRA, you face a 10% penalty on top of the taxes owed for any withdrawals before age 59½. Anyone can take out the same amount of money they put into a Roth IRA at any time without having to pay taxes on it.

You can only take out your earnings without being charged a fee, though, if you’ve had the account for five years and are over 55.

There are a few exceptions to these early withdrawal rules. Early distributions of earnings for these reasons are considered exceptions: taxable as income but not subject to the 10% penalty. The most popular include:

- You can take out up to $10,000 to help pay for your first home, the home of your spouse, your children, or your grandchildren.

- Withdrawals to pay for college expenses

- Taking out up to $5,000 in the first year after giving birth or adopting a child

- Not getting paid for medical bills that are higher than 10% of your adjusted gross income for the year or health insurance premiums while you’re unemployed may be given to you.

IRA Explained In Less Than 5 Minutes | Simply Explained

FAQ

Is there a downside to opening an IRA?

Yes, there are downsides to opening an IRA, including early withdrawal penalties for both Traditional IRAs and Roth IRAs, required minimum distributions (RMDs) for Traditional IRAs, potential loss of investment value, and income-based eligibility limits for Roth IRAs.

How much tax on an $50,000 IRA withdrawal?

What are the tax consequences of taking money out of an IRA? RateSingleHeadofHousehold10%$0%20%E2%80%93%$11,925$0%20%E2%80%93%$17,00012%$11,925%20%E2%80%93%$48,475$17,000%20%E2%80%93%$64,85022%$48,475%20%E2%80%93%$103,350$64,850%20%E2%80%93%20$103,35024%$103,350%20%E2%80%93%20$197,300

Can I lose my IRA if the market crashes?

During a market crash, you can lose money in an IRA because investments like stocks and bonds can lose value. But you probably won’t lose the whole amount, and the fact that market downturns are only temporary gives you a chance to get back on track in the long run.

Do I have to pay taxes on my IRA after age 65?

Withdrawals between the ages of 59½

What are the pros and cons of an IRA?

While the pros of IRAs generally outweigh the cons, there are a few drawbacks to be aware of. IRAs have strict contribution limitations. To contribute to an IRA, you or your spouse need earned income. For 2024 and 2025, the maximum contribution amount per person is $7,000, and those aged 50 and older can make a $1,000 catch-up contribution.

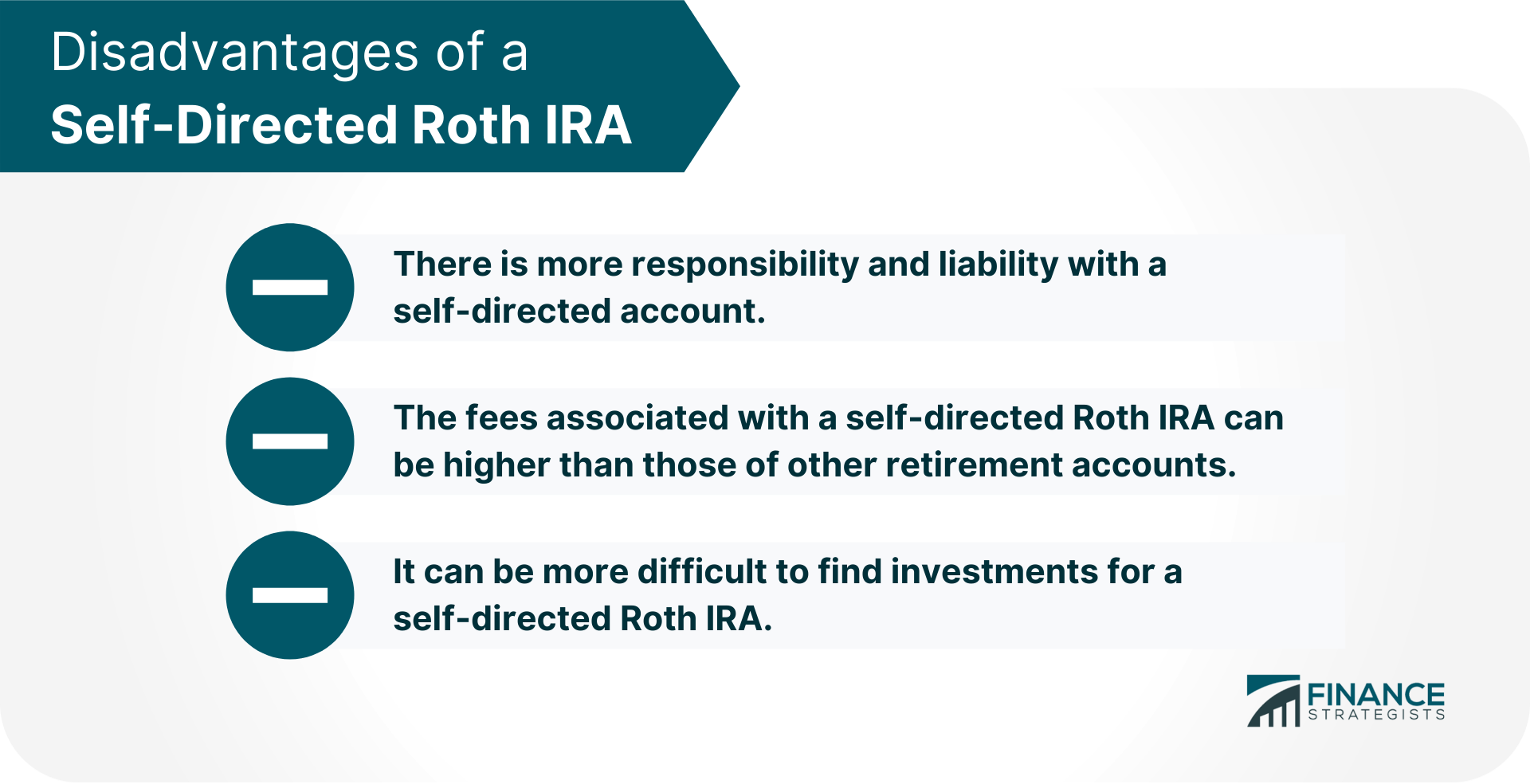

What are the disadvantages of a Roth IRA?

Here are all the disadvantages of the Roth IRA. For those of you who are in the higher federal income tax bracket, be especially wary of contributing to a Roth IRA. For 2025, the maximum Roth IRA contribution, if you are eligible, is still $7,000. 1) The government is inefficient. I’m all for patriotism.

Are Roth IRAs tax-advantaged?

That isn’t the case with traditional IRAs. In a nutshell, Roth IRAs are tax-advantaged retirement accounts that allow you to pay your tax bill upfront and then sit back, relax, and enjoy tax-free growth and withdrawals. That sounds appealing, right? Well, don’t forget that every silver lining has a cloud. Roth IRAs are no exception.

What happens if you leave a Roth IRA?

For example, if you contribute $10,000 to your Roth IRA and it grows to $15,000. There is a 10% penalty on the $5,000 + your normal tax rate. Just don’t be naive to put it past the government to one day tax your after-tax Roth IRA contributions again upon exit. Look at Social Security, for example.

Are Wealthfront IRAS tax-advantaged?

Wealthfront’s IRAs are fully automated to make retirement saving simple. Open a Wealthfront IRA Perhaps IRAs’ best known benefit is their tax-advantaged status—this benefit is designed to encourage you to put money away for later. The tax advantages of traditional IRAs and Roth IRAs are slightly different.

Are Roth IRAs a good investment?

That said, everything has a downside, and Roth IRAs have their fair share. Weighing the Roth IRA’s benefits and drawbacks could help you decide if and how to incorporate one into your retirement planning. Tax-free growth and withdrawals in retirement. No tax deduction for contributing.