Ever stared at your bank account wondering if you’ve saved enough? You’re definitely not alone. Whether you’re just starting your savings journey or looking to beef up your financial cushion, figuring out the “right” amount to have in savings can feel overwhelming.

Let me break it down for you in a way that actually makes sense. As someone who’s spent years helping folks navigate their financial journeys, I can tell you there’s no magic number—but there are some solid guidelines that can help you sleep better at night.

The Emergency Fund: Your Financial Safety Net

The most basic savings goal everyone should have is an emergency fund. Financial experts typically recommend having 3 to 6 months of living expenses saved up for those unexpected life curveballs.

Why this range? Well, it’s enough to cover you if you:

- Lose your job

- Face unexpected medical bills

- Need major car repairs

- Have a surprise home maintenance issue

Let’s say your monthly expenses (rent/mortgage, utilities, groceries, insurance, etc.) total $5,000. Your emergency fund target would be between $15,000 and $30,000.

But don’t panic if that seems impossible right now! The important thing is to start somewhere

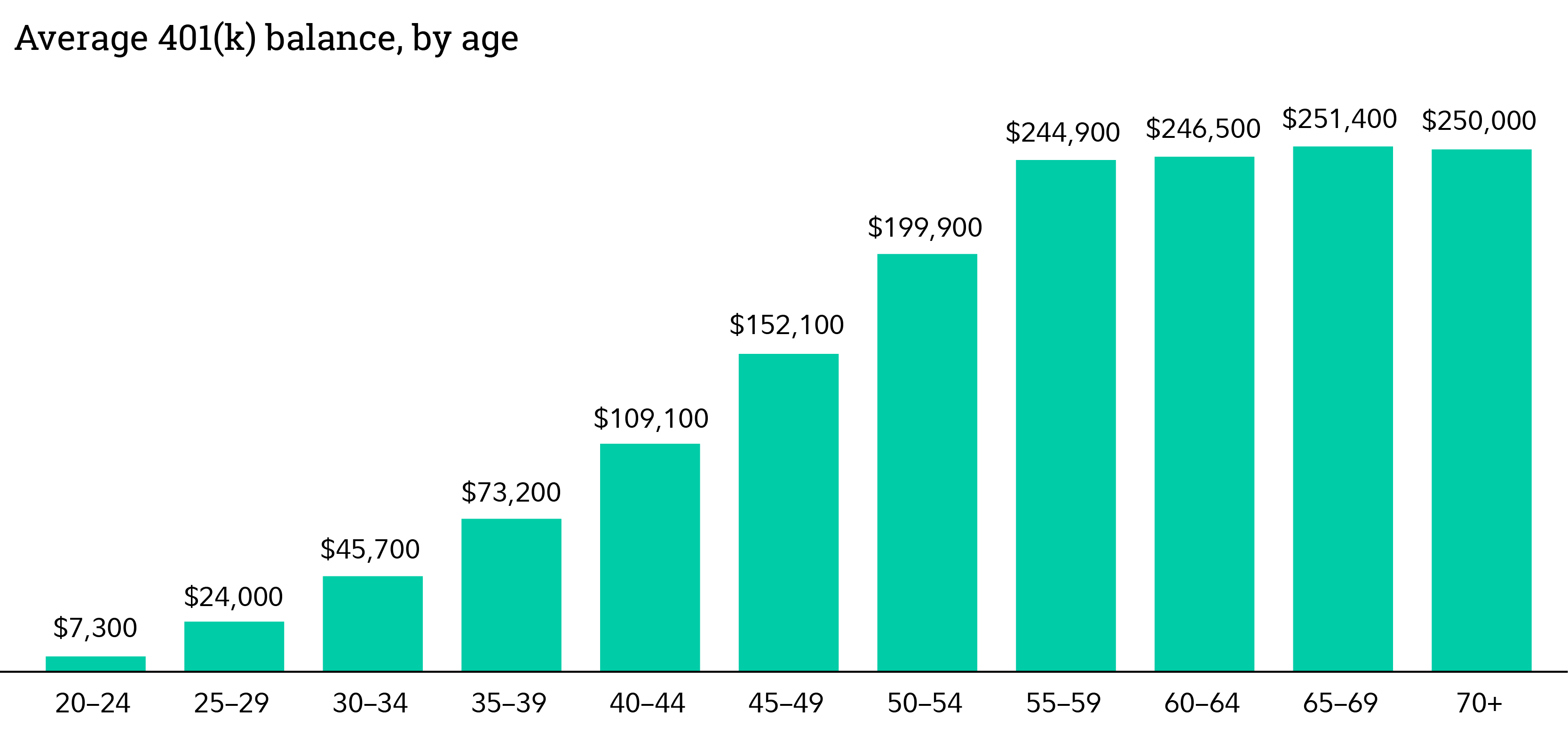

Breaking Down Savings by Age Group

The average American has about $62,410 in savings, according to the Federal Reserve Board’s 2022 Survey of Consumer Finances. But when you look at the breakdowns by age, things get interesting:

| Age Group | Average Savings |

|---|---|

| Under 35 | $20,540 |

| 35-44 | $41,540 |

| 45-54 | $71,130 |

| 55-64 | $72,520 |

| 65-74 | $100,250 |

| 75+ | $82,800 |

These numbers show a clear pattern: savings tend to increase with age, which makes sense as people progress in their careers and have more time to accumulate wealth.

The 50/30/20 Rule: A Simple Way to Budget

The 50/30/20 rule is a common way to figure out how much you should save. After taxes, your income should ideally be divided like this .

- 50% for needs (housing, food, utilities)

- 30% for wants (entertainment, dining out)

- 20% for savings and debt repayment

Based on the median salary by age, this is what your monthly savings might look like if you use this formula:

| Age Group | Median Monthly Salary | 20% for Savings |

|---|---|---|

| 20-24 | $3,136 | $627 |

| 25-34 | $4,544 | $909 |

| 35-44 | $5,424 | $1,085 |

| 45-54 | $5,344 | $1,069 |

| 55-64 | $5,072 | $1,014 |

| 65+ | $4,636 | $927 |

Savings Goals by Life Stage

In Your 20s

Your 20s are all about establishing good financial habits Focus on

- Building that emergency fund

- Starting retirement savings (even small amounts benefit from compound interest)

- Saving for big purchases like a car or home down payment

Aim to save around $500+ monthly if possible. Even if you can’t hit that, start with what you can—consistency is key!

In Your 30s

As your income grows, so should your savings. In this decade, you might be:

- Starting a family

- Buying a house

- Advancing in your career

Try to save at least $800 monthly and increase your retirement contributions.

In Your 40s

By now, you should be hitting your stride financially. Your goals might include:

- College funds for kids

- Increasing retirement savings

- Possibly saving for a career change

Aim to save nearly $1,000 or more each month.

In Your 50s and Beyond

With retirement on the horizon, saving becomes more crucial than ever. Your focus should be:

- Maximizing retirement contributions

- Healthcare planning

- Legacy planning

Strive to maintain that 20% savings rate, which should be about $1,000 monthly or more.

Retirement Savings Benchmarks

Here’s a simple way to gauge if you’re on track for retirement. By these ages, you should aim to have saved:

| Age | Savings Target |

|---|---|

| 30 | 1x your annual income |

| 40 | 3x your annual income |

| 50 | 5x your annual income |

| 60 | 7x your annual income |

Say you make $75,000 a year. You should have about $225,000 saved for retirement by the time you are 40.

The Magical Power of Compound Interest

Here’s where things get exciting. The earlier you start saving, the less you actually need to save each month thanks to compound interest.

Check out the difference in your total savings by age 65% based on when you start saving (assuming a 6% annual return and based on the U S. median household annual income of $74,580):

| Starting Age | 5% Annual Savings Rate | 10% Annual Savings Rate | 15% Annual Savings Rate |

|---|---|---|---|

| 25 | $575,714 | $1,153,286 | $1,730,857 |

| 35 | $294,096 | $589,141 | $884,187 |

| 45 | $136,842 | $274,126 | $411,410 |

The difference between starting at 25 vs. 45 is MASSIVE! This is why we always say start early, even if it’s just a little bit.

Emergency Fund Targets by Age

Your emergency fund should cover 3-6 months of expenses. Here’s what that looks like for different age groups based on average monthly expenses:

| Age Group | Average Monthly Expenses | 3 Months of Savings | 6 Months of Savings |

|---|---|---|---|

| Under 25 | $4,130 | $12,390 | $24,780 |

| 25-34 | $5,989 | $17,967 | $35,934 |

| 35-44 | $7,578 | $22,734 | $45,468 |

| 45-54 | $8,110 | $24,330 | $48,660 |

| 55-64 | $6,948 | $20,844 | $41,688 |

| 65+ | $5,007 | $15,021 | $30,042 |

Where Should You Keep Your Savings?

Not all savings accounts are created equal! For your emergency fund, consider:

-

High-yield savings accounts: These offer much better interest rates than traditional savings accounts—sometimes 10x the national average rate (around 5.25% APY compared to much lower rates at traditional banks).

-

Money market accounts: These typically offer competitive interest rates while maintaining the accessibility you need for emergency funds.

-

Certificates of deposit (CDs): For money you won’t need immediately, CDs can offer even higher interest rates, though your money will be tied up for a specific period.

Remember that your emergency fund should be easily accessible, so keep it in an account where you can withdraw without penalties.

Common Barriers to Saving (and How to Overcome Them)

According to recent surveys, these are the top reasons people struggle to save:

-

Rising living costs (66%): Try to renegotiate bills, find more affordable housing, or look for ways to reduce utility costs.

-

Debt repayment (31%): Consider consolidating high-interest debt or using the debt snowball/avalanche method to tackle it strategically.

Other strategies to boost your savings include:

- Automating your savings through direct deposit

- Using budgeting apps to track spending

- Finding a side hustle to increase income

- Cutting unnecessary subscriptions

When Is It Too Much Savings?

Yes, you can actually have too much in savings! If you have significantly more than 6 months of expenses in a regular savings account, you might be missing out on better growth opportunities.

Consider investing excess savings in:

- Stocks

- Bonds

- Real estate

- Retirement accounts

Remember, money in traditional savings accounts barely keeps pace with inflation, while invested money has the potential to grow substantially over time.

My Final Thoughts

There’s no one-size-fits-all answer to how much you should have in savings. Your personal situation, goals, and comfort level with risk all play important roles in determining the right amount for you.

But here’s my advice: start where you are. Even if you can only save $50 a month right now, that’s $600 more than you had last year! Build from there, and remember that consistent saving habits matter more than the actual amount when you’re just getting started.

I like to think of savings as buying peace of mind. Each dollar you put away is one more worry off your shoulders when life throws its inevitable curveballs.

What’s your biggest challenge when it comes to saving? Drop a comment below—I’d love to help you figure out a personalized savings plan that works for your situation!

I Don’t Know What to Do With My $100,000 in Savings

FAQ

Is $20,000 a good amount of savings?

20k is a good emergency fund. As long as it’s in a high-yield savings account earning at least 4%, it should just sit there until you need it.

Is $30,000 a good amount of savings?

For many, saving $30,000 can take years to achieve. In fact, the median bank account balance among U. S. adults was $8,000 in 2022, according to the Federal Reserve. 1 So if you have $30,000 in your bank account, you’re doing relatively well.

How much should a 30 year old have saved?

A good guideline is to have saved the equivalent of your annual salary by age 30, as recommended by financial institutions like Fidelity Investments and CNBC. For example, if you earn $60,000 per year, you should aim to have $60,000 saved for retirement.

Is having $50,000 in savings good?

50k is a good emergency savings that should give you peace of mind. Rates are good right now, I would park it in a money market fund. Emergency savings are not something you want to invest in risky assets.

How much should I spend on my savings?

Read more: Give your savings a boost with Ally Bank Savings Buckets. One way to hit your savings goal is to think of it as a portion of your income. The popular 50/30/20 budget framework dictates that after taxes, 20% of your income should go toward savings and debt repayment, while 50% should go to needs and 30% to wants.

How much money should you save a month?

If you’ve heard of the 50/30/20 rule for budgeting, it says you should stash 20% of your paycheck into savings every month always. But here’s the deal: Sticking to that 20% isn’t always doable—or advisable. Remember, if you’re in debt, getting those payments out of your life is your number one financial goal.

How much should I save for retirement?

Bankrate is always editorially independent. Finding out the exact amount you need to save for retirement can be hard, but here are some general rules based on age that can help you get started. Generally, experts recommend have one times your salary saved by age 30 and eight times saved by 60.

How much money can you save at 30?

By this logic, you should have at least $50,000 saved at 30. The Federal Reserve study found that people under the age of 35 had an average savings of $34,780. Since the data isn’t broken down any further, it is difficult to say how much more 30-year-olds have saved than 25-year-olds.

How much money should I set aside for a savings account?

A rule of thumb is to set aside 50% of your income for necessities, 30% for discretionary expenses and 20% for savings. Use this free savings calculator to project how your money can grow over time. Checking and savings accounts are both bank accounts that allow immediate access to funds.

How much money should you save in your 20s?

Your 20s is the time to set strong savings habits. Using the 50/30/20 model, you could aim to save upward of $500 every month (or as much as you can). Saving where and when you can and being strategic with windfalls (such as a bonus), and dedicating additional income (like an annual raise) can help you work toward this goal.