As a strategic partner who helps clients navigate and grow in changing circumstances, Tina is responsible for the direct management of the Citizens Wealth Management financial planning and estate planning team, including a team of CERTIFIED FINANCIAL PLANNERS™, estate and tax planners, and trust officers.

Most people look forward to their retirement, dreaming of a lifestyle in which they have the freedom to spend their days as they wish and answer to no one. But how much do you need to retire? Figuring out when to retire requires a careful look at your current salary, investments, how you plan to live in retirement, and other things.

In the ever-changing landscape of retirement planning, many of us are asking one crucial question “How much money do I actually need when I hit 70?” With rising inflation, unpredictable healthcare costs, and longer lifespans, this question has never been more important Whether you’re already in your golden years or planning ahead, understanding the financial realities of retirement at 70 can help ensure you’re prepared for what’s ahead

The Reality of Retirement Savings at 70

New data from Empower Personal DashboardTM shows that the average American has saved $491,022 for retirement. What about people in their 70s, though? The numbers tell an interesting story:

- Americans in their 70s have an average retirement balance of $994,140

- The median retirement balance for 70-somethings is $432,043

- Many 70-year-olds actually fall into the “retirement millionaire” category

But here’s the thing – averages can be misleading. These numbers are driven up by high-net-worth individuals, which is why the median figure (the middle point where half have more and half have less) gives us a more accurate picture of what most 70-year-olds actually have saved.

SmartAsset’s research backs up these results, showing that the average person aged 65 to 74 has just over $609,000 saved in retirement accounts like 401(k)s and IRAs. Additionally, the typical 70-year-old has .

- $100,250 in transaction accounts (checking and savings)

- $138,440 in certificate of deposit (CD) accounts

- $39,310 in savings bonds

- $55,530 in cash value life insurance

Monthly Expenses at 70: Where Does the Money Go?

To understand how much you need for retirement, we gotta look at what you’ll actually be spending According to recent data from the Federal Reserve Economic Data (FRED), the average 70-year-old spends about $5,429 per month, or $65,149 annually.

Here’s a breakdown of where that money typically goes:

| Expense Category | Monthly Cost | Percentage of Budget |

|---|---|---|

| Housing | $1,851 | 34% |

| Transportation | $908 | 17% |

| Food | $714 | 13% |

| Healthcare | $662 | 12% |

| Cash contributions | $230 | 4% |

| Other expenses | $1,064 | 20% |

For people 70 and older, housing costs the most, as they do for most age groups. A lot of financial experts say that downsizing is a good way to cut down on this big cost in retirement.

How Much Should You Have Saved by 70?

Most financial experts say that you should save between $1 million and $2 million for retirement. There seems to be a big difference between this and the average savings of $609,000 for people aged 65 to 74.

So, how much is enough? The answer varies based on several factors:

- Your desired lifestyle: Do you want to travel extensively or live modestly?

- Your Social Security benefits: When did you start taking them?

- Other income sources: Do you have pensions, annuities, or rental income?

- Your health: Do you anticipate high medical expenses?

- Your expected longevity: How long might you live in retirement?

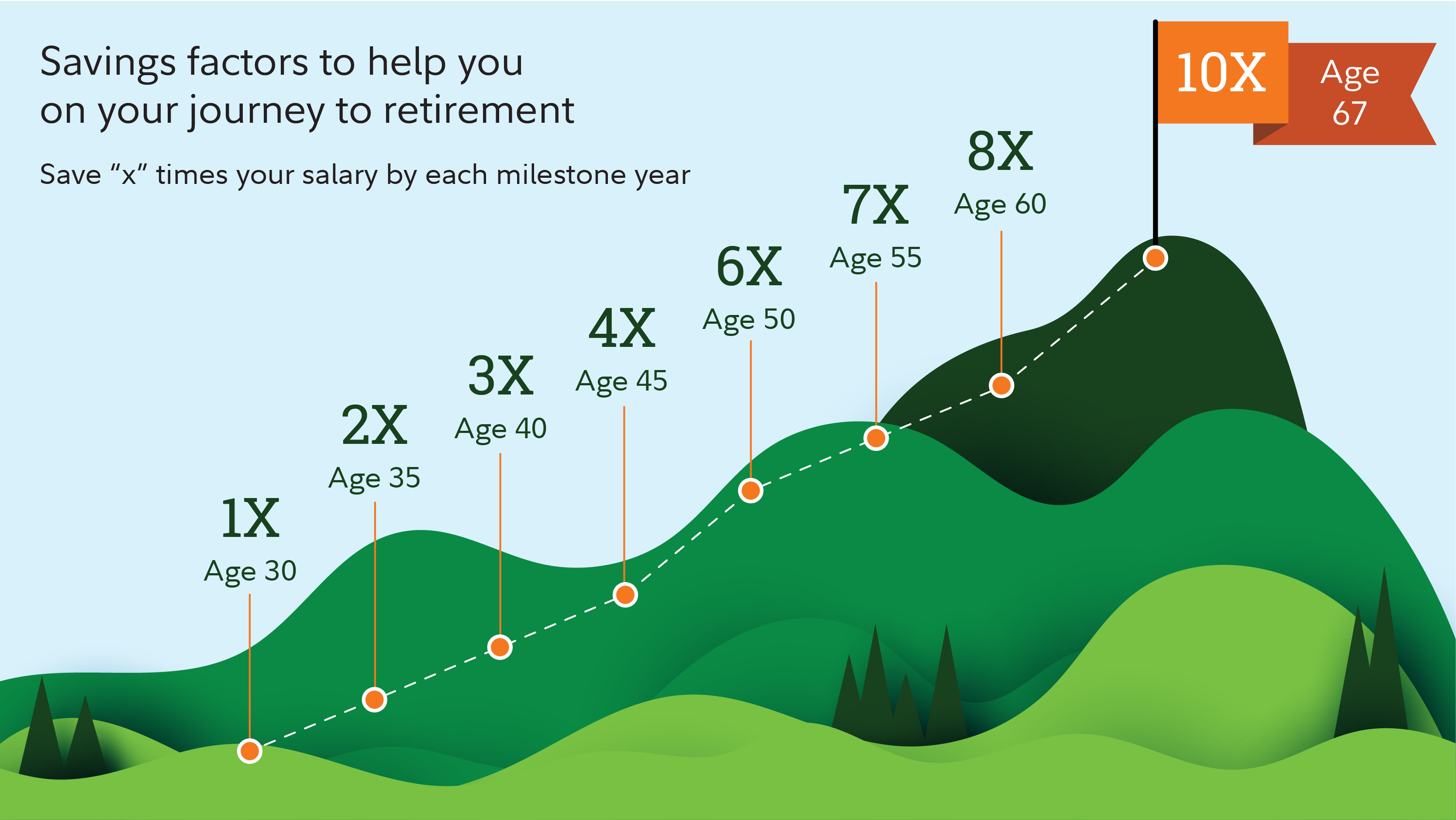

The Multiplier Approach

One common rule of thumb suggests having a net worth at 70 that’s 20 times your annual expenses. Using this formula:

- If you spend $100,000 annually, aim for $2 million in net worth

- If you spend $60,000 annually, aim for $1.2 million in net worth

- If you spend $40,000 annually, aim for $800,000 in net worth

The 4-5% Withdrawal Rule

Many financial advisors recommend withdrawing 4-5% of your savings in the first year of retirement, then adjusting that amount for inflation in subsequent years. This approach can help you determine how much you need to save:

- To generate $40,000 annually (using 4% rule): $1 million

- To generate $60,000 annually (using 4% rule): $1.5 million

- To generate $80,000 annually (using 4% rule): $2 million

The Role of Social Security in Your Retirement Budget

Social Security benefits form a crucial part of most retirees’ income, but they’re not designed to be your sole source of funds. By age 70, you’ll be eligible for maximum benefits if you’ve delayed claiming until this age.

If you wait until 70 to collect Social Security, you’ll receive 132% of your full benefit amount. This could significantly increase your monthly income without touching your savings as much.

Health Care Costs: The Wild Card in Retirement Planning

Health care is often the most unpredictable expense in retirement. At 70, Medicare will cover many of your basic medical needs, but there are still significant gaps:

- Medicare doesn’t cover long-term care

- Prescription drug costs can be substantial

- Dental, vision, and hearing services often require supplemental coverage

The average 70-year-old spends $662 per month on healthcare, but this can vary dramatically based on individual health conditions. It’s wise to budget for increasing healthcare costs as you age.

Why Some Experts Recommend Retiring at 70

There are several financial advantages to waiting until 70 to retire:

- Maximized Social Security benefits: As mentioned, you’ll get 132% of your full benefit amount

- More time to save: Extra working years mean more contributions to retirement accounts

- Delayed RMDs: You’ll have a two-year window before Required Minimum Distributions begin at age 72

- Potential Roth conversions: You can use this window to convert traditional IRAs to Roth accounts

- Shorter retirement to fund: With fewer years in retirement, your savings don’t need to stretch as far

Creating a Realistic Budget for Retirement at 70

To determine how much you personally need for retirement at 70, follow these steps:

-

Estimate your essential expenses:

- Housing (mortgage/rent, property taxes, insurance, utilities)

- Food and groceries

- Healthcare premiums and out-of-pocket costs

- Transportation

- Insurance

-

Add discretionary spending:

- Travel and entertainment

- Hobbies and recreation

- Gifts and charitable giving

- Dining out

-

Calculate your expected income:

- Social Security benefits

- Pension payments

- Annuity income

- Part-time work (if applicable)

-

Determine your withdrawal needs:

- Subtract your expected income from your estimated expenses

- The difference is what you’ll need to withdraw from savings annually

-

Apply the 4% rule:

- Multiply your annual withdrawal needs by 25 to estimate your required savings

Investment Strategies for 70-Year-Olds

At 70, your investment strategy should focus on preserving capital while still generating income. Consider:

- Shifting to more conservative investments: Increase bond allocations and reduce stock exposure

- Focusing on dividend-paying stocks: Generate income without selling assets

- Creating a bond ladder: Stagger bond maturities to provide regular income

- Considering annuities: Provide guaranteed income for life

Beyond the Numbers: Quality of Life in Retirement

While we’ve focused on the financial aspects of retirement, it’s important to remember that retirement success isn’t just about having enough money. Empower research shows that a “Return on Happiness” isn’t just about reaching big money milestones but is achieved through:

- Being able to pay bills on time (67%)

- Living debt-free (65%)

- Affording everyday luxuries without worry (54%)

- Spending on experiences with loved ones (53%)

- Retiring on your own terms (37%)

My Advice: 5 Steps to Take Now for Retirement Success

If you’re concerned about having enough for retirement at 70, here are five actionable steps I’d recommend:

-

Maximize retirement contributions: If you’re still working, contribute the maximum to your 401(k) and IRA, including catch-up contributions if you’re over 50.

-

Delay Social Security: If possible, wait until 70 to claim benefits to receive the maximum amount.

-

Reduce housing costs: Consider downsizing or relocating to a lower-cost area to decrease your largest expense.

-

Create a detailed budget: Know exactly what you’re spending and where you can cut back if needed.

-

Consider working part-time: Even a small income can significantly reduce the amount you need to withdraw from savings.

The Bottom Line

The average 70-year-old needs approximately $65,000 annually ($5,429 monthly) to maintain a comfortable lifestyle in retirement. To generate this income using the 4% rule, you’d need about $1.6 million in savings. However, with Social Security benefits potentially covering $20,000-$40,000 of those annual expenses, many retirees can manage with less in savings.

Everyone’s retirement journey is unique, and the “right” amount depends on your personal circumstances, goals, and lifestyle choices. While the numbers provided offer helpful benchmarks, they should serve as guidelines rather than strict rules.

The most important thing is to start planning early, save consistently, and regularly reassess your retirement strategy as you approach age 70. And remember – it’s never too late to improve your financial situation!

How much do you plan to spend in retirement?

Its important to determine your post-retirement spending based on your expected lifestyle. What will you do in retirement? For example, traveling the world would likely cost more than spending most of your time with your grandchildren. Some people retire from their primary careers and then embark on post-retirement careers to supplement their incomes.

Factors that affect how much you’ll need to retire

You will need to evaluate multiple different factors when estimating your income needs in retirement. Here are some things to consider that will help you answer the question, “How much do you need to retire?”.

Average Retirement Savings at Age 70

FAQ

How much should a 70-year-old have for retirement?

There is no single amount of money a 70-year-old needs to retire; it depends on individual annual expenses, but a common rule of thumb is to have 20 times your estimated annual retirement expenses saved, according to SmartAsset. com. For example, if you expect to spend $100,000 annually, you’d need $2 million saved.

How many Americans have $1,000,000 in retirement savings?

Approximately 2. 5% to 4. Seven percent of Americans have $1 million or more saved for retirement. Among retirees, that number is slightly higher (around 20 percent). 2%) and households with any retirement accounts.

Can you retire at 70 with $400,000?

It is 100% possible to retire with $400,000, provided you’re not looking to enjoy a particularly expensive retirement lifestyle or hoping to leave the workforce notably early.

Is $300,000 enough to retire at age 70?

You could retire at age 70 with $300,000. But it depends on how much you spend, how you live, and where you live. This means you’ll need to plan carefully and maybe stick to a small budget. Using the common 4% rule, $300,000 could provide an initial annual income of about $12,000, though you might consider a lower rate for greater stability.

How much money should a 70-year-old save?

According to the Federal Reserve, the average 70-year-old has just shy of $600,000 saved. This highlights the importance of starting retirement planning early and considering diverse investment strategies to ensure a comfortable retirement.

Should I retire at 70?

Whether it makes sense to retire at age 70 depends on how much money you have and how you want to spend your retirement. When choosing a retirement age, it’s helpful to consider: If you can delay taking Social Security benefits until age 70, that can boost your benefit amount.

How much savings should a 70 year old have?

By age 70, you should have at least 20X your annual expenses in savings or as reflected in your overall net worth. For example, if you spend $75,000 a year, you should have about $1,500,000 in savings or net worth to live a comfortable retirement.

How much money do you need to retire?

Based on the 80% principle, you can expect to need about $96,000 in annual income after you retire, which is $8,000 per month. What is a reasonable retirement budget?

How much money do you need to live a comfortable retirement?

The higher your expense coverage ratio by 70, the better. In other words, if you spend $75,000 a year, you should have about $1,500,000 in savings or net worth to live a comfortable retirement. How much money does the average couple retire with?

How much money can you make a year after retirement?

For example, if a person made roughly $100,000 a year on average during his working life, this person can have a similar standard of living with $70,000 – $80,000 a year of income after retirement. This 70% – 80% figure can vary greatly depending on how people envision their retirements.