For most people, the answer is yes. These strategies could help minimize the hit on this retirement income source.

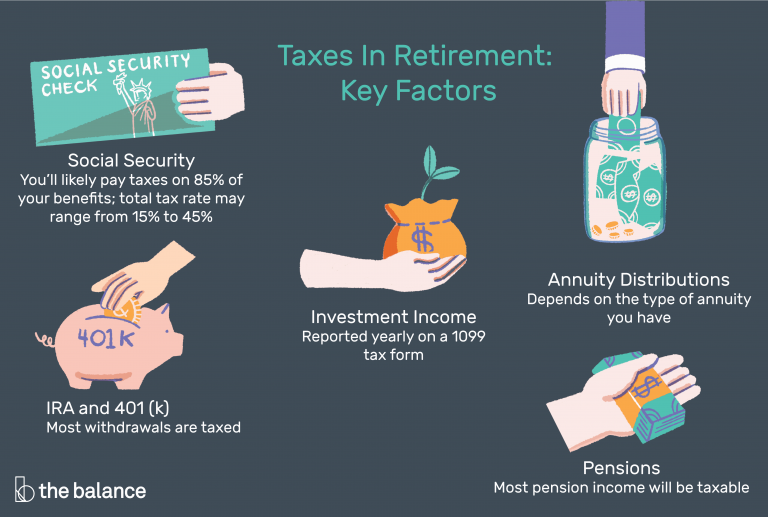

Social Security was never meant to be the sole source of income for retirees. Still, with a maximum benefit of more than $45,000 a year if you file at full retirement age, it can be a big, steady boost. To get the most out of your benefit, you need to carefully plan, but keep in mind that you could have to pay income taxes on up to 85% of your Social Security Income.

You can count on getting a certain amount of Social Security as part of your retirement income by doing two main things:

Though benefits are largely based on your earnings history â the more you earn the more you get, up to the maximum benefit â on average, after taxes and adjustments, theyâre likely to replace only around 39% of the past earnings of a 65-year-old who retires in 2024.3 Many investors miss this important detail. âThat can be a real shock when people begin collecting benefits,â says Ben Storey, director, Retirement Research & Insights, Bank of America. A little upfront planning may help avoid the shock of a hefty tax bill and maximize your Social Security benefits over the long haul.

Social Security benefit taxes are based on what the Social Security Administration (SSA) refers to as your âcombinedâ income. That consists of your adjusted gross income, plus any nontaxable interest you earned (and certain other items) and half of your Social Security income. The thresholds for when your benefits will be taxable vary based on your filing status as shown in the chart below.

It should be fun to relax and enjoy the fruits of your labor when you retire, but taxes don’t go away when you do. A question that retirees often ask me is if they need to pay taxes on their Social Security benefits if they also get a pension. It’s a real worry that millions of Americans have, and the answer isn’t always clear.

The Short Answer: Yes, You Might

If you receive both Social Security benefits and pension income, you may indeed have to pay federal income taxes on a portion of your Social Security benefits However, this depends on your total “combined income” and filing status Let’s break down exactly how this works and what you need to know.

How Social Security Benefits Are Taxed

The IRS has specific rules about when Social Security benefits become taxable. According to the IRS, the key factor is your “combined income,” which includes:

- Your adjusted gross income

- Tax-exempt interest income

- Half of your Social Security benefits

Based on this combined income, here’s how taxation works:

For Individual Filers:

- If your combined income is between $25,000 and $34,000, up to 50% of your benefits may be taxable

- If your combined income exceeds $34,000, up to 85% of your benefits may be taxable

For Married Filing Jointly:

- If your combined income is between $32,000 and $44,000, up to 50% of your benefits may be taxable

- If your combined income exceeds $44,000, up to 85% of your benefits may be taxable

For Married Filing Separately:

- If you lived apart from your spouse all year and have combined income between $25,000 and $34,000, up to 50% may be taxable

- If you lived apart and have income above $34,000, up to 85% may be taxable

- If you lived with your spouse at any time during the year, up to 85% of your benefits may be taxable regardless of income

How Pensions Affect Your Social Security Taxation

Here’s where things get interesting Your pension absolutely counts toward your combined income for determining whether your Social Security benefits are taxable This is a critical point many retirees miss.

While the Social Security Administration notes that “pension payments, annuities, and the interest or dividends from your savings and investments are not earnings for Social Security purposes” (meaning you don’t pay Social Security taxes on this income), these sources still count as income when determining if your Social Security benefits are taxable.

Let me give you an example

John is single and receives $15,000 in Social Security benefits and $20,000 from his pension annually. To determine if his benefits are taxable, he would:

- Take half his Social Security benefits: $15,000 ÷ 2 = $7,500

- Add this to his pension income: $7,500 + $20,000 = $27,500

Some of John’s Social Security benefits would be taxed because $27,500 is more than the $25,000 limit for single filers.

State Taxes Are Another Story

While we’ve been talking about federal taxes, don’t forget that state taxes can also come into play. The good news is that many states don’t tax Social Security benefits at all. Others follow the federal rules, and some have their own exemptions and rules.

If you live in a state that taxes retirement income, you might face state taxes on your pension and potentially on your Social Security benefits too. I recommend checking with your state’s tax authority for specific information.

The Pension-Social Security Double-Whammy

When you have both pension and Social Security income, you’re essentially dealing with two types of taxation:

- Your pension is generally taxed as ordinary income at your regular tax rate

- A portion of your Social Security benefits may be taxable based on your combined income

This creates what I call the “retirement tax double-whammy” that catches many retirees by surprise.

Tax Rates That May Apply to Your Retirement Income

For 2024, these are the federal tax brackets that would apply to your taxable income, including taxable portions of your pension and Social Security:

| Tax rate | Single filers | Married filing jointly | Head of household |

|---|---|---|---|

| 10% | $0 to $11,600 | $0 to $23,200 | $0 to $16,550 |

| 12% | $11,600 to $47,150 | $23,200 to $94,300 | $16,550 to $63,100 |

| 22% | $47,150 to $100,525 | $94,300 to $201,050 | $63,100 to $100,500 |

| 24% | $100,525 to $191,950 | $201,050 to $383,900 | $100,500 to $191,950 |

| 32% | $191,950 to $243,725 | $383,900 to $487,450 | $191,950 to $243,700 |

| 35% | $243,725 to $609,350 | $487,450 to $731,200 | $243,700 to $609,350 |

| 37% | $609,350 or more | $731,200 or more | $609,350 or more |

Strategies to Reduce Taxes on Retirement Income

Now that I’ve delivered the not-so-great news, let’s talk about ways you might be able to reduce your tax burden:

1. Roth Conversions Before Retirement

Converting traditional IRA or 401(k) funds to Roth accounts before retirement can provide tax-free income later. Yes, you’ll pay taxes on the conversion, but future withdrawals won’t count toward your combined income for Social Security taxation.

2. Manage Your Withdrawals

In some years, planning ahead for when and how much to take out of different accounts can help you keep your total income below the tax thresholds.

3. Qualified Charitable Distributions (QCDs)

If you are 70½ or older, you can give money directly from your IRA to charities that qualify, and the money won’t be taxed.

4. Municipal Bonds

Interest from municipal bonds is typically exempt from federal taxes and sometimes state taxes as well. This could provide income that doesn’t trigger Social Security taxation.

5. Health Savings Accounts (HSAs)

If you have an HSA, distributions used for qualified medical expenses are tax-free and don’t count toward your combined income.

A Real-World Example

Let’s look at a more detailed example to see how this works:

Maria and Robert are married and file jointly. In 2024, they receive:

- $30,000 in Social Security benefits

- $40,000 from Robert’s pension

- $5,000 in interest income

Their combined income calculation:

- Half of Social Security: $30,000 ÷ 2 = $15,000

- Pension income: $40,000

- Interest income: $5,000

- Total combined income: $15,000 + $40,000 + $5,000 = $60,000

Since their combined income of $60,000 exceeds the $44,000 threshold for married couples filing jointly, up to 85% of their Social Security benefits (or $25,500) may be subject to federal income tax.

Their total potentially taxable income would be:

- Up to $25,500 from Social Security

- $40,000 from the pension

- $5,000 from interest

- Total: Up to $70,500

This would likely put them in the 12% tax bracket for 2024, based on the table above.

Common Questions About Social Security and Pension Taxation

Does pension count as income for taxing Social Security?

Yes, pension income is included in your combined income calculation that determines whether your Social Security benefits are taxable.

Can you collect a pension and Social Security at the same time?

Absolutely! You can receive both benefits simultaneously. However, if your pension is from a job where you didn’t pay Social Security taxes (like some government jobs), your Social Security benefits might be reduced under the Windfall Elimination Provision or Government Pension Offset.

How much will my Social Security be reduced if I have a government pension?

If you receive a pension from work not covered by Social Security, your benefits might be reduced by two-thirds of your government pension amount under the Government Pension Offset.

Do you pay Medicare and Social Security tax on a pension?

No, you don’t pay Medicare or FICA taxes on pension income, Social Security benefits, or retirement account withdrawals. However, these sources may still be subject to income tax.

Final Thoughts

Navigating taxes in retirement can be complicated, especially when you have multiple income sources like Social Security and pensions. While I’ve provided an overview of the rules, everyone’s situation is unique. Tax laws also change regularly.

For these reasons, I strongly recommend consulting with a tax professional who specializes in retirement income. They can help you develop a personalized tax strategy that minimizes your tax burden while ensuring you’re compliant with all applicable laws.

Remember, proper tax planning isn’t just about this year—it’s about maximizing your retirement income for the long haul. A little planning now can save you thousands in taxes throughout your retirement years.

Have you been surprised by taxes on your retirement income? I’d love to hear about your experiences and any strategies you’ve found helpful for managing retirement taxes!

Look past the current year

âWhen you plan for retirement,â says Vinay Navani, a shareholder with WilkinGuttenplan, an accounting and consulting firm in East Brunswick, New Jersey, âyou need to think in terms of multiyear projections. If you’re planning a big one-time event, like selling a business, you might be better off setting up the sale as an installment sale that is paid off over a few years instead of an all-cash deal. This can help evenly distribute your overall income and possibly keep you in a lower tax bracket, which could help reduce the portion of your Social Security benefits that is subject to federal income tax.

Caution: An unexpected financial windfall could put you in a higher tax bracket, resulting in a bigger tax bill.

Caution: An unexpected financial windfall could put you in a higher tax bracket, resulting in a bigger tax bill.

Determine when working makes sense

Those hoping to work in retirement need to be especially careful if theyâre planning to claim Social Security benefits early.

For most baby boomers, full retirement age is between 66 and 67 years old. If you start taking your benefits before that age, the SSA limits how much you can earn before your benefits are cut. For every $2 you earn over the limit, your Social Security benefits are reduced by $1. Once you reach the year in which youll turn your full retirement age, the earned income cap goes up, and for every $3 you go over, your benefits are reduced by $1. Starting with the month you reach full retirement age, there is no limit to what you can earn and receive all of your benefits.

Even if youâre just working part time, itâs important to consider how that continuing income will affect your benefits as shown by the graphic below.