Professional mountain climbers often say that going up the mountain is hard, but coming down is what really tests their strength.

In a way, your career and retirement follow a similar trajectory. As you work, you slowly climb the mountain (your pension), and when you get to the top, you start to go down (or rather, decumulate). Both journeys come with their own hardships, but you could find that the decumulation phase is surprisingly challenging.

You can start getting money from your private pension(s) when you turn 55 years old, starting with the 2025–26 tax year. This is known as “normal minimum pension age” (NMPA), and it will rise to 57 in 2028.

If you are standing on top of your retirement mountain – in other words, you have reached 55 and can start taking your pension now – should you sit back and enjoy the view, or start making your way down straight away?

Reaching your mid-50s doesn’t mean you’ve missed the retirement boat – here’s why

Are you approaching 55 and panicking about not having a pension plan? Maybe you’ve been putting it off, or perhaps life’s other financial demands have taken priority. The good news? It’s definitely not too late to start a pension at 55. While starting earlier would have given you more time to build your nest egg, there’s still plenty you can do to secure a comfortable retirement even with a later start.

The Reality of Starting a Pension at 55

Let’s be honest – starting a pension at 55 means you have a shorter timeline to accumulate wealth. With the average UK State Pension age now at 67, you’re looking at roughly 12 years to build your retirement fund. That’s not insignificant but it does require strategic planning and potentially larger contributions than if you’d started in your 30s or 40s.

As one financial expert puts it: “Starting a workplace pension at 55 and retiring at 67 only gives your cash 12 years to grow, so you could expect a final pot of around £31,732. Over a 20-year retirement that’s an income of just under £1,600 a year.”

It may look like a bad sign, but remember that this is only one part of your retirement puzzle.

Why It’s Never Too Late to Start

Despite the shorter timeline there are several compelling reasons why starting a pension at 55 is absolutely worthwhile

- Tax advantages are significant – You’ll still benefit from tax relief on your contributions, which effectively gives your pension an immediate boost

- Compound interest still works – Even over 12 years, your investments can grow substantially

- Catch-up provisions exist – If you’re over 50, you can make additional “catch-up contributions” to accelerate your savings

- You may work longer than expected – Many people now work beyond the traditional retirement age, giving your pension more time to grow

- It’s better than doing nothing – Even a modest pension is better than relying solely on the State Pension

Key Strategies When Starting a Pension at 55

If you’re 55 years old and starting to save for retirement, these tips can help you get the most out of your money:

1. Maximize Your Contributions

Aim to contribute as much as you can afford to your pension. The current annual allowance for pension contributions is £40,000 or 100% of your earnings, whichever is lower. With tax relief, every £100 you contribute effectively costs you only £80 (or less if you’re a higher-rate taxpayer).

2. Take Advantage of Catch-Up Contributions

If you’re 50 or older, you can make catch-up contributions to your retirement accounts. This allows you to put away an additional £1,000 per year beyond the standard limits.

3. Consider Working Longer

Working a few years past the normal retirement age can make your pension much bigger in three ways:

- More time for contributions

- More time for your investments to grow

- Higher Social Security/State Pension benefits when you do claim them

4. Look Into a SIPP (Self-Invested Personal Pension)

A SIPP gives you more control over your pension investments. It works like a workplace pension in that it will pay out when you retire, but you can pick your own investments and how the money is invested.

As one expert notes: “Given the level of investment knowledge needed, this is probably best suited for individuals who have done a great deal of research. If you prefer something more straightforward, there are private pensions where the investment manager will inquire about your tolerance for risk before making your selections.”

5. Consider a Pension Rollover or GLWB Annuity

If you have existing pension funds or are offered a lump sum option, rolling these into a Fixed Indexed Annuity with a Guaranteed Lifetime Withdrawal Benefit (GLWB) might provide better income security.

According to retirement specialists: “GLWB annuities offer lifetime payouts at age 55+ that can be 5%–7% of the protected value annually — and the income can never decrease, even if the market crashes.”

Is Your Pension Sustainable? 10 Questions to Ask

Before making decisions about starting or taking your pension at 55, ask yourself these important questions:

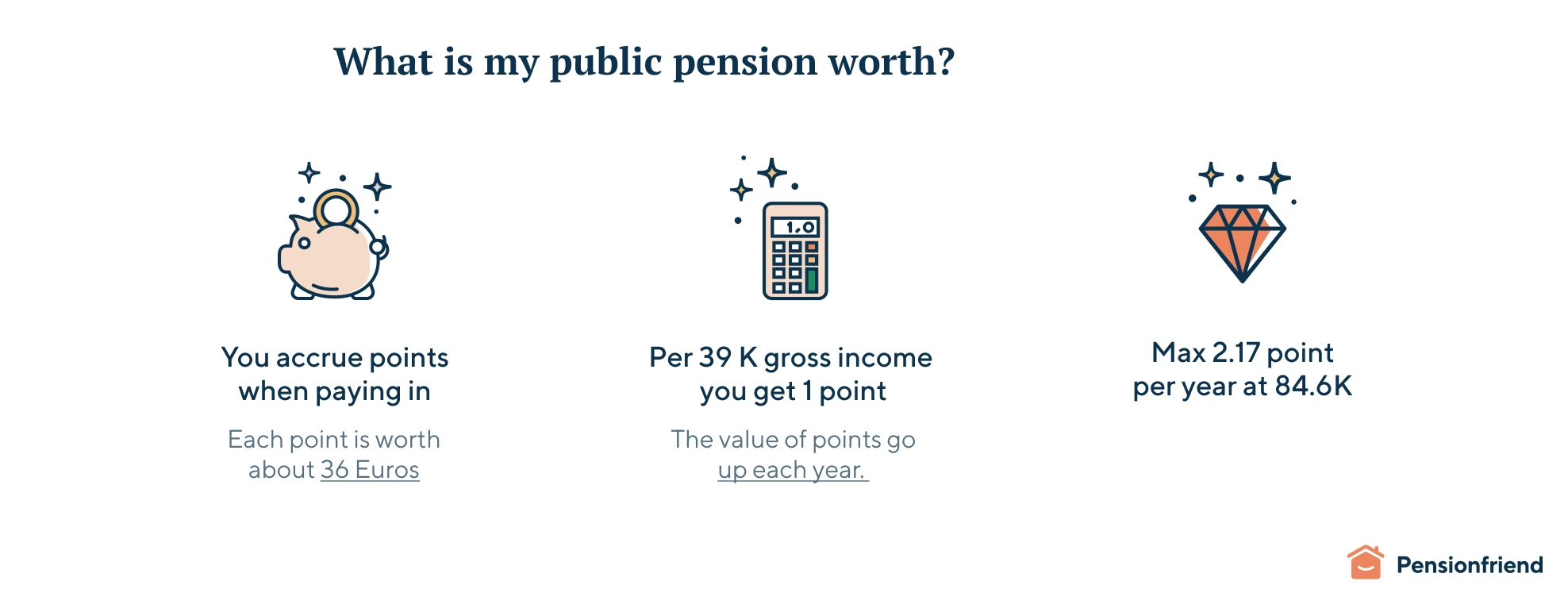

- What is my pension worth today?

- What is my desired annual retirement income?

- If I began drawing my pension today, could I sustain my lifestyle?

- How much could my pension grow if I continue working longer?

- How will inflation affect my pension’s value during retirement?

- What investment risks is my pension currently taking?

- Can I afford to support family members with my pension if needed?

- How much tax will I pay when drawing my pension?

- What fees am I paying, and are they reasonable?

- Do I understand the best timing and method for pension withdrawals?

Understanding Your Full Financial Picture

Your pension is just one part of your retirement strategy. Before making decisions, understand your entire wealth situation:

- State Pension – Check your forecast on the government website

- ISAs and other tax-advantaged accounts

- Cash savings

- Property or business income

- Potential inheritances

- Other investment accounts

According to Standard Life research, a staggering 79% of those aged 55-64 can’t put a number on what their pension is worth. Don’t be in this group – knowledge is power when it comes to retirement planning!

The Benefit of Professional Advice

Planning a pension at 55 can be complex. A financial planner can offer valuable tools like cashflow modeling that help you:

- Project how long your savings might last

- Account for inflation’s impact

- Model various market scenarios

- Plan for major life events and expenses

- Optimize tax efficiency

- Explore later-life care options

As one financial advisor puts it: “Many mountaineers attest that while the ascent is challenging, coming down from the mountain is the part that really tests their resilience. Your career and retirement follow a similar trajectory – you tirelessly climb (pay into a pension) while working, and once you reach the top, you begin to descend (decumulate). Both journeys have their hardships, but the decumulation phase can be surprisingly challenging.”

Common Misconceptions About Starting a Pension at 55

Let me clear up some myths about late-start pension planning:

Myth 1: “It’s pointless to start now”

Reality: Even with just 12 years until retirement age, your contributions can grow substantially, especially with tax advantages.

Myth 2: “I’ll need to work forever”

Reality: While you might need to work a bit longer than planned, a strategic approach can still provide a comfortable retirement.

Myth 3: “I can just rely on the State Pension”

Reality: The State Pension alone (currently around £10,600 per year) is unlikely to maintain your desired lifestyle.

Myth 4: “I can take my pension at 55 and be fine”

Reality: According to the Actuarial Post, 67% of over-55s underestimate their longevity and risk outliving their savings. The earlier you draw your pension, the longer it needs to last.

Final Thoughts: Is It Worth Starting a Pension at 55?

The answer is a resounding YES – with caveats.

Starting a pension at 55 is absolutely worthwhile, but requires careful planning, potentially larger contributions, and possibly working a few years longer than you might have hoped. The alternative – doing nothing – leaves you in a much more vulnerable position.

Remember, every pound you save now can make a difference to your future comfort and security. And with the right strategy, even a late-start pension can provide a meaningful boost to your retirement income.

Don’t let the perfect be the enemy of the good. The best time to start a pension was 30 years ago, but the second-best time is today – even at 55.

What Next?

If you’re 55 and pension-less, take these immediate steps:

- Calculate your current financial position – assets, debts, income, and expenses

- Determine your retirement goals – when you want to retire and your desired income

- Explore pension options – workplace schemes, SIPPs, or other retirement vehicles

- Seek professional advice – a financial advisor can help optimize your approach

- Start contributing immediately – even small amounts make a difference

The journey of a thousand miles begins with a single step – and your comfortable retirement journey can start today, even at 55.

Note: This article provides general information only and does not constitute advice. All information is correct at the time of writing and is subject to change in the future. Please do not act based on anything you might read in this article without seeking professional financial advice tailored to your specific circumstances.

Before taking your pension, you need to understand your wealth situation in full

This might sound like simplistic advice. But the truth is, according to an Standard Life study, 79% of those aged 55 – 64 can’t put a number on what their pension is worth.

If you are in this age group and want to start taking money out of your defined contribution (DC) pension pot, which could be a workplace pension, a self-invested personal pension, or something similar, you need to know how much it is worth.

Once you understand what your pension is worth, it helps to do the same for your other sources of retirement income.

These include:

- Your State Pension. Visit the government website to find out how much you can get from the State Pension when you reach State Pension Age, which is 66 in 2025/26 and will go up to 67 by 2028.

- Your Individual Savings Accounts (ISAs). There is no tax to pay when you take money out of an ISA, which makes it a great way to make money in retirement.

- Cash savings. Along with your pensions, savings, and investments, you may have a separate fund that you plan to use in a smart way.

- Property or business income. You could set up these assets so that they give you a steady stream of income after you retire.

Getting to grips with your wealth as a big picture, rather than solely focusing on your pension, could help you to determine whether taking your pension at 55 is a good idea.

The below tips may allow you to understand your situation even more clearly.

Is your pension sustainable? 10 questions to consider

Focusing back on your pension, there is one question you should try to answer before taking it: “Is my pension sustainable?”.

According to a report from the Actuarial Post, 67% of over-55s underestimate their longevity and are at risk of outliving their retirement savings. The earlier you draw the money, the longer you need to make it last.

These 10 questions could prompt you to look carefully at your pension wealth and discover whether it is sustainable.

- What is my pension worth today?

- What is my desired annual retirement income?

- Will I be able to live the way I want to live for the rest of my life if I start getting my pension today?

- If I keep working longer and leave my pension invested, how much could it grow?

- How much will inflation make my pension worth less when I retire?

- How much investment risk is my pension taking right now? How would a drop in the stock market affect my retirement?

- Could I afford to use my pension to help my family if we need it?

- How much tax will I have to pay when I take out my pension and add it to the other money I get in retirement?

- In relation to my pensions, what fees do I pay? Are these fees too high?

- Am I sure that I know when and how to get my pension the best?

Why Everything in Retirement Changes If You Have a Pension

FAQ

Is it worth starting a new pension at 55?

How much your pension is worth usually depends on what you contribute through your working life. It’s never too late to get started – here’s everything you need to know. Pensions are long-term investments. Your capital is not guaranteed, and fees may be added, so you may get back less than you put in.

How much pension should I have at 55?

If you want to retire at age 55 and keep living the way you want to, you’ll need between 50% and 2/3 of your yearly salary as retirement income. In that case, you’ll likely have paid off the mortgage, not have to pay for your commute, and the kids will hopefully be able to live on their own.

What is the rule of 55 for pensions?

The rule of 55, explained

The rule of 55 is an IRS provision that allows workers who leave their job for any reason to start taking penalty-free distributions from their current employer’s retirement plan in or after the year they reach age 55.

Can I start taking my pension at 55?

Should you start a pension at 50?

While it is always better to start as early as possible, you’re not running out of time in your 50s. Even if you start at 50, you still have 16 working years to save. The current state pension is 66, and there are plans for it to increase in the coming years. You have plenty of time to save a nice pension pot.

Is it too late to start a pension?

Many people who’ve reached the age of 50 and haven’t yet started a pension assume it’s too late to start one. But, if you can start putting away cash into a pension fund now, it can still be one of the best ways to invest for your retirement.

Should you invest in a pension at 55?

Say it’s 15,000 or more and you’re getting more than 20,000 take-home now. Pension investing at 55 can easily be a good idea in that case. Making more, perhaps paying higher rate tax? Even more incentive to use a pension. Want to live on under 10,000 a year? Making 1,000 or less now take-home? Then you probably need to see the numbers to decide.

Can a pension be accessed at 55?

It’s important to note that not all pensions can be accessed at 55. For instance, the State Pension age is currently 66, and some public sector pensions have protected pension ages. It’s always best to check with your pension provider about their specific terms and conditions. Your pension withdrawal options at 55

How old do you have to be for a good retirement?

If you’re between 55 and 64 years old, you still have time to set yourself up for a solid retirement. Whether you plan to retire early, late, or never, having an adequate amount of money saved can make all the difference. Your focus should be on building out—or catching up, if necessary.

What if I don’t have a pension at 50?

Even if you have no pension at 50, going by a typical State Pension age of 67, you still have 17 years left to invest. A lot can be done in that time. So, if you’re approaching retirement and haven’t done anything yet, act fast to give your investments the maximum opportunity to grow.