Yes, you can do it even if you don’t have a regular job. This is part of a series called Roth IRAs: Dos and Donts for Investing and Trading.

The IRS does not allow contributions to a Roth IRA without what it calls earned income. That usually means that you need a paying job—working for either someone else or your own business—to make Roth IRA contributions. But what if you don’t have one—a job, that is—and you still want a Roth?.

Even if you don’t have a conventional job, you still may be able to contribute to a Roth IRA.

Are you wondering if you can stash away some cash in a Roth IRA even though you don’t have traditional income? I’ve been there, and the confusion around retirement accounts when you’re not earning a regular paycheck can be overwhelming! Let’s clear things up about contributing to a Roth IRA without income

The Short Answer: You Need Earned Income (Usually)

Unfortunately, the IRS is pretty clear on this one – to contribute to a Roth IRA, you generally need what they call “earned income.” But don’t close this tab just yet! There are some surprising exceptions and workarounds that might apply to your situation.

What Qualifies as “Earned Income”?

Before we dive into the exceptions, let’s clarify what the IRS considers earned income:

- Wages, salaries, and tips

- Commissions and bonuses

- Self-employment income and freelance earnings

- Taxable non-tuition fellowship and stipend payments

- Nontaxable combat pay

What’s NOT considered earned income:

- Interest and dividends

- Rental income

- Pension or annuity payments

- Social Security benefits

- Unemployment benefits

5 Ways You Can Contribute to a Roth IRA Without a Traditional Job

1. Spousal Roth IRA: The Marriage Advantage

If you’re married to someone with earned income, you’re in luck! Even if you personally have zero income, you can open what’s known as a “spousal IRA”

Here’s how it works:

- Your spouse’s earnings qualify both of you for IRA contributions

- You must file taxes as “married filing jointly”

- Your spouse must earn enough to cover both your contributions

- For 2025, you can contribute up to $7,000 each ($8,000 if you’re 50+)

- That means couples can contribute a total of $14,000-$16,000 annually

The spousal IRA functions exactly like a regular Roth IRA – the only difference is where the money comes from And if you return to work later? No problem! Your account continues as normal.

2. Income from Exercised Stock Options

Did you exercise non-qualified stock options this year? The difference between the grant price and the exercise price is generally taxable income – and yep, you can use this to justify a Roth IRA contribution!

3. Taxable Scholarships and Fellowships

Students, pay attention! Most of the time, tuition scholarships aren’t thought of as earned income, but some parts of scholarships and fellowships might be. Publication 970 of the IRS says that if your scholarship or fellowship pays for:

- Room and board

- Teaching responsibilities

- Research duties

- Living expense stipends

These portions are usually taxable – and therefore count as earned income for Roth IRA purposes. This is a huge opportunity for students to start building retirement savings early!

4. Nontaxable Combat Pay

Military personnel receive a special exception. Even though combat pay is nontaxable, it still qualifies as earned income for Roth IRA contribution purposes. You’ll find this reported in Box 12 of your W-2 form.

5. Alimony (In Some Cases)

For divorce or separation agreements signed before December 31, 2018, alimony and separate maintenance payments that are taxed can be used as earned income for IRA contributions.

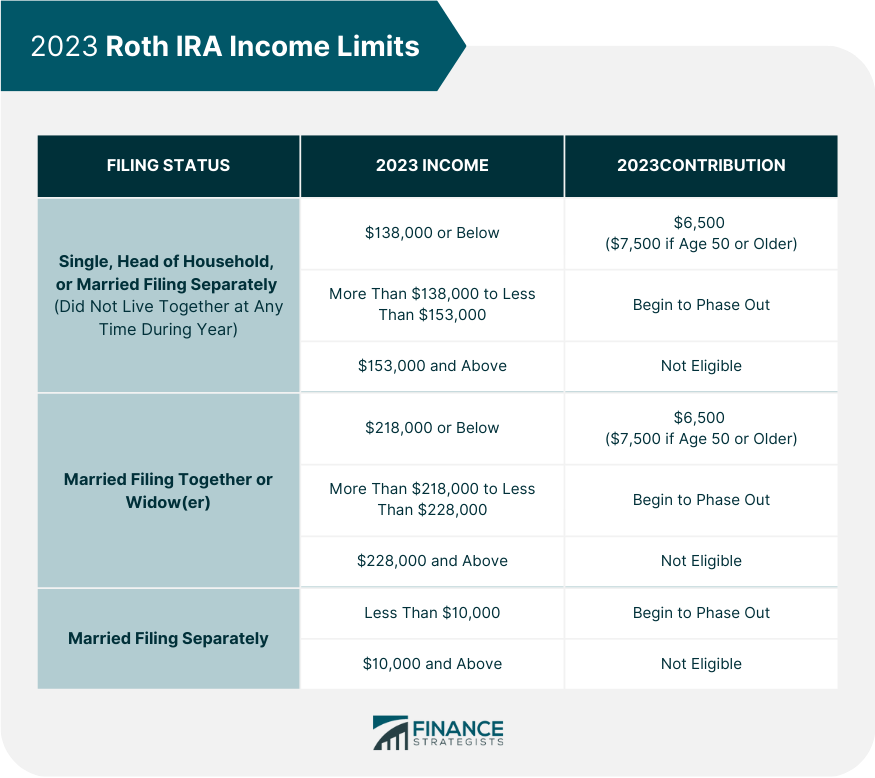

Important Income Limits to Remember

Even if you have some form of earned income, remember that the IRS sets income limits on who can contribute to a Roth IRA. For 2025, if you file as:

- Single or Head of Household: Contributions phase out between $146,000-$161,000

- Married Filing Jointly: Contributions phase out between $230,000-$240,000

The Danger Zone: Penalties for Contributing Without Earned Income

So what happens if you contribute to a Roth IRA without having earned income? I wouldn’t recommend it – the penalties can be steep!

Tax rules say that if you make Roth IRA contributions that aren’t allowed (for example, if you make contributions without earning income), you’ll have to deal with:

-

A 6% Excise Tax Penalty – This applies to the excess contribution amount for each year it remains in your account. For example, a $5,000 ineligible contribution would cost you $300 annually (6% of $5,000) until corrected.

-

Taxes on Earnings – Any investment gains from those ineligible contributions must be withdrawn and reported as taxable income.

-

Potential Early Withdrawal Penalties – If you’re under 59½ when withdrawing these earnings, you might face an additional 10% early withdrawal penalty.

-

Possible IRS Scrutiny – Ongoing noncompliance could trigger audits or detailed financial examinations.

How to Fix an Ineligible Contribution

Made a mistake? Don’t panic! The IRS allows you to fix it by:

- Withdrawing the excess contribution AND any earnings it generated before your tax filing deadline (including extensions)

- Filing the proper forms with your tax return

You’ll have to pay the 6% penalty every year that the extra money stays in your account if you don’t pay by this deadline.

Real-World Example: Sarah’s Situation

Let me share an example from a friend of mine. Sarah was a stay-at-home mom with no personal income. She initially thought she couldn’t save for retirement until she went back to work. However, since her husband Alex had sufficient earned income and they filed jointly, she was able to open a spousal Roth IRA and contribute the full $7,000 for 2025.

This allowed Sarah to build her own retirement savings despite not having a traditional job. When she eventually returned to part-time work years later, her account continued growing without any changes needed.

Why Roth IRAs Are Worth the Effort

Even if you have to get creative with finding qualifying income, Roth IRAs offer incredible benefits:

- Tax-free growth – Your investments grow without capital gains taxes

- Tax-free withdrawals in retirement – Unlike traditional IRAs, qualified Roth withdrawals are completely tax-free

- No required minimum distributions – Unlike traditional IRAs, you’re never forced to withdraw money

- Flexibility for emergencies – You can withdraw your contributions (not earnings) penalty-free at any time

Timing Your Contributions

Remember, you have until the tax filing deadline (typically April 15) to make IRA contributions for the previous tax year. So for 2025 contributions, you’ll have until April 15, 2026. This gives you extra time to figure out if you have qualifying income.

Final Thoughts: Get Creative But Stay Compliant

While the IRS does require earned income for Roth IRA contributions, the definition of “earned income” is broader than many people realize. The key is making sure your contributions are legitimate – the penalties for breaking the rules just aren’t worth it.

If you’re still unsure about your specific situation, I’d recommend consulting with a tax professional. They can evaluate your unique circumstances and help you find legal ways to build your retirement savings.

Remember, retirement planning isn’t just for those with traditional 9-to-5 jobs. With a bit of knowledge and creativity, many people without conventional income can still take advantage of the incredible benefits of a Roth IRA.

Have you found other creative ways to qualify for Roth IRA contributions? I’d love to hear about your experiences in the comments below!

Can a Stay-at-Home Parent Have a Roth IRA?

A stay-at-home parent who has no income of their own can still have a Roth IRA. There is no difference between a spousal IRA and any other Roth IRA. The only difference is that your spouse’s income determines if you can get a Roth IRA based on the maximum income limits.

If you are married and file your taxes jointly in 2025, you can still put in the full amount ($7,000, or $8,000 if you are 50 or older).

The Good News

There’s a good chance you can put money into a Roth IRA even if you’re paying taxes on any kind of work-related income. Wages, salaries, tips, bonuses, commissions, and self-employment income are all examples of “earned income.” However, there are other types of income that you might not immediately think of as “earned.” ”.

Some examples of ways that you might fund a Roth IRA without having a traditional job or steady pay include exercised stock options, scholarships or fellowships, your spouses earned income, and nontaxable combat pay.

Your eligibility to contribute to a Roth IRA also depends on how much you earn. The IRS sets income limits that restrict high earners based on modified adjusted gross income (MAGI) and tax-filing status.

Roth IRA contributions without any income

FAQ

Can you contribute to a Roth IRA if you have no job?

No, you can’t contribute to a Roth IRA unless you have earned income. You can open a regular brokerage account.

Can you put non-earned income into a Roth IRA?

Yes, you need to have earned money to put money into a Roth IRA because the amount you can put in is limited by your taxable income. Earned income includes wages, salaries, tips, bonuses, and net earnings from self-employment.

Can a stay at home mom contribute to Roth IRA?

Yes, a stay-at-home mom can contribute to a Roth IRA through a spousal Roth IRA if her working spouse has sufficient earned income and they file a joint tax return.

What disqualifies you from having a Roth IRA?

Roth IRA exclusions can refer to two concepts: avoiding income limits for contributions and having certain distributions be tax-free and penalty-free. Qualified distributions are generally those made after age 59½, after a five-year period has passed since the first contribution, or in cases of death or disability.

Can you contribute to a Roth IRA if you have no income?

You can contribute to a Roth IRA if you have earned income and meet the income limits. Even if you don’t have a conventional job, you may have income that qualifies as “earned. ” Spouses with no income can also contribute to Roth IRAs using the other spouse’s earned income. Can I contribute to a Roth IRA if I have no income?.

Can I contribute to a Roth IRA if I don’t have a job?

Answer: Yes, you can put money into a Roth IRA even if you don’t have a regular job. Most people think that to contribute to a Roth IRA, you need to have earned income from a job. However, the IRS defines “earned income” as a wider range of income sources.

Can I contribute to a Roth IRA if I don’t get a paycheck?

While the traditional understanding of contributing to a Roth IRA involves having earned income from employment, the IRS definition of “earned income” encompasses a broader range of income sources. This means that even if you don’t receive a regular paycheck, you may still qualify to contribute to a Roth IRA.

Who can contribute to a Roth IRA?

Anyone with both earned income greater than the amount they want to contribute and income that falls within IRS guidelines can contribute to a Roth IRA. To determine if you meet these requirements, you’ll need to know how much income you’ve received, as well as your filing status.

Can a retiree contribute to a Roth IRA?

Retirees can contribute to a Roth IRA even after they’ve left the workforce. However, they must have earned income. While retirement itself doesn’t disqualify someone from making Roth IRA contributions, the earned income requirement applies regardless of age or retirement status.

Can a non working person contribute to a Roth IRA?

Yes, non-working individuals can contribute to a Roth IRA through options like a spousal Roth IRA, where a working spouse contributes on their behalf, as long as they meet certain income and filing status requirements. What are the income requirements for contributing to a Roth IRA without working?