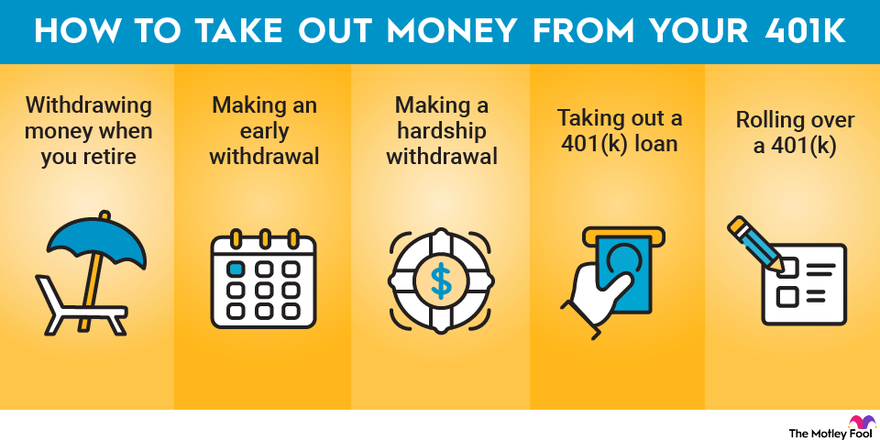

A 401(k) can be a great tool to help you save and invest for retirement. Pre-tax contributions to a traditional 401(k) can help reduce your taxable income today, and you won’t owe taxes until you make withdrawals, usually in retirement. But you might wonder: What if I need some or all of my 401(k) money now? Financial emergencies happen—and in some cases, drawing on your 401(k) may be your only option. Here are the different ways to access your 401(k) money, along with pros and cons to consider.

Have you been eyeing that 401(k) balance and wondering if there’s any way to tap into it without getting slapped with penalties? You’re not alone. Many folks find themselves needing access to their retirement funds before they actually retire and the good news is – yes you can still pull money from your 401(k) without penalty in certain situations!

Let’s dive into the nitty-gritty of how to access your retirement funds penalty-free even before hitting that magical age of 59½.

The Basic Rule: 59½ Is Your Freedom Age

First things first – the standard rule is pretty straightforward. Once you hit age 59½, you can generally withdraw from your 401(k) without facing that nasty 10% early withdrawal penalty. This is the simplest path to penalty-free withdrawals.

But wait! There’s an important distinction to make:

- With traditional 401(k) withdrawals, you’ll still pay ordinary income taxes on the money

- With Roth 401(k) withdrawals, you can potentially take the money tax-free if you’ve met the five-year rule and age requirements

However, many of us need money before we’re pushing 60. So what options do we have?.

Penalty-Free 401(k) Withdrawals Before Age 59½

There are several exceptions to the 10% penalty rule that can help you access your funds earlier Let’s explore the most common ones

1. The Rule of 55

This is a biggie for early retirees or those changing careers later in life.

If you leave your job in or after the year you turn 55, you can withdraw from that specific employer’s 401(k) without the 10% penalty. This applies only to the 401(k) from the employer you just left, not any previous employer plans or IRAs.

Some key points to remember:

- You must have separated from service (quit, been laid off, or fired)

- The money must stay in that employer’s 401(k) plan (don’t roll it to an IRA if you want to use this exception!)

- You’ll still owe regular income taxes on traditional 401(k) withdrawals

2. Substantially Equal Periodic Payments (SEPP/72t)

This option is available at any age but comes with strict rules.

With a 72(t) plan, you commit to taking a series of substantially equal payments for at least five years or until you reach 59½, whichever is longer. The payment amounts follow IRS-approved methods and can’t be modified without penalties.

This is a good option if you need consistent income before traditional retirement age, but it requires careful planning since you’re locked into the payment schedule.

3. Birth or Adoption Expenses

Listen up, new parents! Within a year of a birth or adoption, you can take out up to $5,000 per parent without any fees. This exception was added not long ago, and it’s a good way to deal with those high first-year costs.

You will still have to pay income taxes on traditional 401(k) withdrawals, but you won’t have to pay the 2010 penalty. Some plans even allow you to repay this distribution later.

4. Medical Expenses

If you’re facing large medical bills, you might qualify to withdraw penalty-free to cover unreimbursed medical expenses that exceed 7.5% of your adjusted gross income (AGI).

Say your AGI is $60,000, you could take money out of your account without being charged a fee to pay for medical costs that are more than $4,500 (7). 5% of $60,000).

5. Disability

If you become totally and permanently disabled, you can access your 401(k) funds without penalty. This typically requires documentation from a physician confirming your disability status.

6. Military Service

If you’re a qualified military reservist called to active duty for more than 179 days, you may be eligible for penalty-free withdrawals during your active service period.

7. Emergency Personal Expenses

A newer exception allows each person to withdraw up to $1,000 per year for personal or family emergency expenses without penalty.

8. Domestic Abuse Victim Distribution

Victims of domestic abuse can withdraw up to $10,000 or 50% of their account (whichever is lower) without penalty.

9. Disaster Recovery

If you suffer economic loss due to a federally declared disaster, you may be able to withdraw up to $22,000 penalty-free.

Alternatives to 401(k) Withdrawals

Before you tap into your retirement savings, consider these alternatives that might be less costly in the long run:

401(k) Loans

Many 401(k) plans allow you to borrow from your account. The benefits include:

- No credit checks

- The loan doesn’t appear on your credit report

- Interest is paid back into your own account

- No penalties or taxes if repaid on time

You can typically borrow up to $50,000 or half of your vested balance, whichever is less. The loan usually must be repaid within five years, though longer terms may be available for home purchases.

Warning: If you leave your job before repaying the loan, you’ll typically need to repay it quickly (often within 60-90 days) or it becomes a taxable distribution with penalties.

Hardship Withdrawals

Some 401(k) plans allow hardship withdrawals if you have an “immediate and heavy financial need.” These are still subject to income taxes and usually the 10% penalty, but they provide access to funds when you truly need them.

Qualifying hardships typically include:

- Medical expenses

- Home purchase (primary residence)

- Tuition and education fees

- Preventing eviction or foreclosure

- Funeral expenses

- Certain home repairs

Building a Smart Withdrawal Strategy

The best approach isn’t just about avoiding penalties—it’s about creating a smart withdrawal strategy that considers taxes, growth potential, and your long-term goals.

Here’s a simple framework to follow:

- Build an adequate emergency fund before retirement to reduce the need for early 401(k) withdrawals

- Consider your withdrawal sequence across accounts (taxable accounts first, then tax-deferred accounts, then Roth accounts)

- Model different withdrawal strategies to minimize lifetime taxes

- Time Social Security carefully to maximize guaranteed income later in life

- Consider small Roth conversions in low-income years to reduce future Required Minimum Distributions (RMDs)

Real-World Examples

Let me share a few examples of how real people have handled early 401(k) access:

Case 1: Alicia, Age 56

Alicia left her employer and wanted to travel for a year. She kept her 401(k) with her former employer to use the Rule of 55. She only withdrew what her taxable cash cushion couldn’t cover, avoiding penalties while keeping taxes manageable.

Case 2: Ben and Lila, Ages 60 and 58

This couple had a mix of taxable, pre-tax, and Roth assets. They drew from taxable accounts first and converted small amounts of pre-tax money to Roth annually, staying under Medicare premium thresholds while reducing future RMDs.

Case 3: Priya, Age 51

Wanting more family time, Priya switched to part-time work. Instead of touching retirement accounts, she built a 12-month cash reserve, reduced fixed expenses, and funded healthcare through an HSA and marketplace plan, preserving her retirement investments.

The Cost of Early Withdrawals

Before you pull money from your 401(k), understand the true cost. Let’s look at an example:

Suppose you withdraw $25,000 from your traditional 401(k) at age 45. Here’s what happens:

- Income tax (assuming 22% bracket): $5,500

- Early withdrawal penalty (10%): $2,500

- Total immediate cost: $8,000

But that’s not all! You’re also losing future growth. If that $25,000 had stayed invested for 20 more years growing at 7% annually, it would have grown to over $96,000. That’s the hidden cost of early withdrawals.

When Must You Start Taking Money Out?

On the flip side, the IRS requires you to start taking Required Minimum Distributions (RMDs) from traditional 401(k) accounts once you reach a certain age:

- If you were born between 1951-1959: Age 73

- If you were born in 1960 or later: Age 75

Roth 401(k) accounts are not subject to RMDs if rolled over to a Roth IRA.

Frequently Asked Questions

Q: Can I withdraw from my 401(k) if I’m still working?

A: Generally, current employer plans don’t allow withdrawals while you’re still employed, unless you reach age 59½ or qualify for a hardship withdrawal. Some plans do allow in-service distributions after age 59½.

Q: What if I roll my 401(k) into an IRA – do the same penalty exceptions apply?

A: Not exactly. IRAs have their own set of penalty exceptions. Notably, the Rule of 55 doesn’t apply to IRAs, but they do have additional exceptions for first-time home purchases and higher education expenses.

Q: How do I know which option is best for me?

A: Each situation is unique! I recommend running the numbers through a retirement calculator or working with a financial professional to model different scenarios.

Wrapping It Up

So, can you still pull money from your 401(k) without penalty? Absolutely! From the Rule of 55 to hardship withdrawals to 72(t) distributions, there are plenty of options. The key is understanding which exceptions apply to your situation and weighing the long-term impact on your retirement security.

Remember, just because you CAN access the money doesn’t always mean you SHOULD. Your 401(k) is designed for retirement, and early withdrawals, even penalty-free ones, can significantly impact your financial future.

How to take an early withdrawal from your 401(k)

To make an early withdrawal from your 401(k), you’ll likely need to do the following:

- Reach out to your HR department or 401(k) plan administrator

- Find out if early withdrawals are possible and how the process works.

- You may need to tell your plan administrator why you need the money in order for them to decide if your withdrawal is a hardship or qualified withdrawal.

- If your request is approved, you should get the money within 10 business days, minus any taxes that need to be taken out.

- If you owe extra 2010 taxes on early withdrawals, you will also need to report the early distribution during tax season.

How to get a 401(k) loan

The steps to take out a 401(k) loan are similar to requesting an early withdrawal:

- Get information from HR or your plan administrator about how much you can borrow, how much interest you will pay, and when you have to pay it back.

- Fill out the required paperwork, if necessary

- Receive your funds, usually within 10 business days of approval

Repayment likely begins once you receive the loan, so be sure to account for those payments in your monthly budget.