A home equity line of credit (HELOC) could help you fund a home renovation or consolidate debt at a lower interest rate. But theres another benefit you may not be aware of: You may be able to deduct the interest you pay on a HELOC from your federal income taxes.

Heres what you need to know about the rules for deducting HELOC interest and how to do it.

A home equity line of credit (HELOC) allows homeowners to borrow against the equity in their home. It works like a credit card, with a variable interest rate and an open line of credit up to a set limit. Many homeowners take out a HELOC to finance home improvements, consolidate debt, or cover unexpected expenses.

One potential benefit of a HELOC is the ability to deduct the interest paid on your taxes. However, recent tax law changes have made the rules around HELOC interest deductions more complicated. Here’s what you need to know about how much interest you can deduct on a HELOC.

Tax Deductibility of HELOC Interest

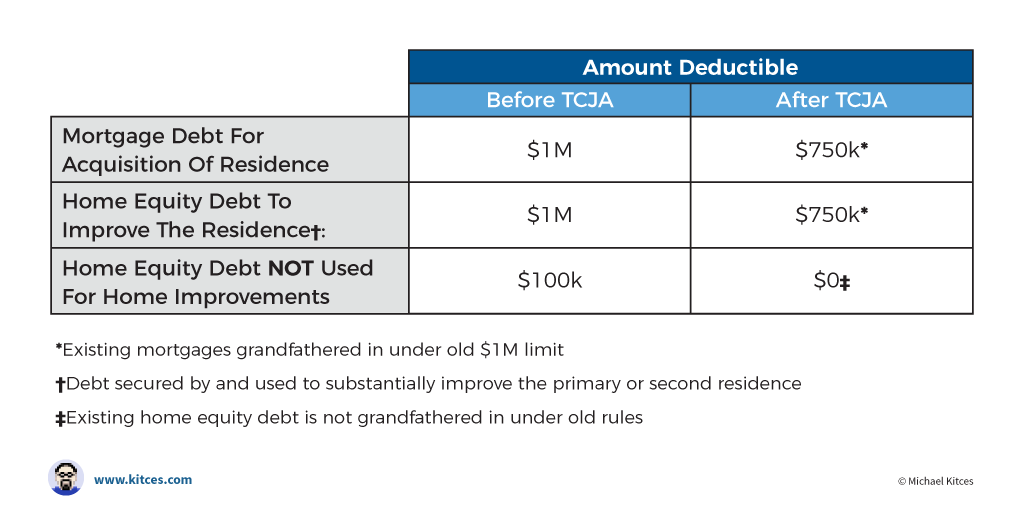

The Tax Cuts and Jobs Act which went into effect in 2018 made major changes to the deductibility of home equity debt interest. Previously, you could deduct interest paid on up to $100,000 of home equity debt, regardless of how you used the funds.

Now HELOC interest is only deductible if you use the proceeds to “buy, build or substantially improve” your home that secures the HELOC. This means renovations and upgrades to your home may qualify but using a HELOC to pay off credit card debt or other expenses will not.

HELOC Interest Deduction Limits

If you use your HELOC funds for qualified home improvements, you can deduct interest paid on up to $750,000 in total mortgage debt. This includes your first mortgage and any home equity loans or lines of credit.

For example:

- You have a $300,000 primary mortgage

- You take out a $50,000 HELOC to remodel your kitchen

- You can deduct interest paid on the entire $350,000

If your total mortgage debt exceeds $750,000, your deduction will be limited. For married couples filing separately, the limit is $375,000 each.

These limits apply to mortgages taken out after December 15, 2017 For older mortgages, the previous limit of $1 million in total mortgage debt ($500,000 if married filing separately) still applies

Calculating Your HELOC Interest Deduction

Figuring out your potential HELOC interest deduction takes a few simple calculations:

1. Determine your total mortgage debt

Add up the following:

- Outstanding balance on your first mortgage

- Outstanding balance on any home equity loans

- Maximum balance on your HELOC (even if you haven’t borrowed that much)

2. Check if you exceed the $750,000 limit

Compare your total mortgage debt to the $750,000 deduction limit ($375,000 if married filing separately).

3. Calculate deductible HELOC interest

If your total is under the limit, you can deduct interest paid on the entire HELOC balance as long as you used the funds for home improvements.

If you exceed the limit, you can only deduct interest paid on the portion of the HELOC debt that brings you up to $750,000 total when added to your other mortgage debt.

4. Add other deductible interest

Include mortgage interest paid on your first mortgage and any other home equity loans used for home improvements. The total is your total deductible interest for the year.

Let’s look at two examples to demonstrate:

Example 1:

- Mortgage balance: $200,000

- HELOC balance: $100,000

- Total mortgage debt: $300,000

Since your total mortgage debt is under $750,000, all $100,000 of the HELOC balance qualifies for the interest deduction.

Example 2:

- Mortgage balance: $500,000

- HELOC balance: $300,000

- Total mortgage debt: $800,000

Your total debt exceeds the $750,000 limit by $50,000. So you can only deduct interest on $750,000 – $500,000 (first mortgage balance) = $250,000 of the HELOC balance.

Claiming the Deduction on Your Taxes

To claim your HELOC interest deduction, you’ll need to file Schedule A along with your Form 1040 when you file your taxes. The interest will be reported in the “Home mortgage interest paid” section. Be sure to keep records such as lender statements and receipts for any home improvements.

Since the standard deduction nearly doubled under the new tax law, fewer taxpayers are itemizing deductions now. Run the numbers to see if you’d come out ahead by itemizing and claiming the HELOC interest deduction.

For most homeowners, the HELOC interest deduction is just an added bonus, not the main motivation for getting a home equity line of credit. Focus first on how you plan to use the funds, and consider the deduction a secondary benefit if you qualify. Consult a tax professional to understand how the deduction works for your individual situation.

Key Takeaways

- HELOC interest is deductible up to $750,000 in total mortgage debt if used for home improvements

- Older mortgages still qualify for the $1 million deduction limit

- Calculate your deductible HELOC interest based on usage and total mortgage debt

- Claim the deduction on Schedule A when you file if you itemize

- Consider the deduction just a bonus, not the main reason for getting a HELOC

With careful planning and an understanding of the deduction rules, the HELOC interest deduction can provide some nice tax savings. But make sure you use HELOC funds wisely and compare other borrowing options too. Focus first on your overall financial goals rather than just chasing tax benefits.

How to Deduct HELOC Interest on Taxes

If you qualify to deduct HELOC interest on your annual tax return, follow these steps to proceed:

What You’ll Need to Claim the HELOC Interest Tax Deduction

To claim HELOC interest on your income taxes, its a good idea to collect some supporting documents, including:

- Mortgage interest statement (Form 1098): Your HELOC lender should send you this form or make it available in your online account dashboard. If necessary, contact your lender to get it before you file your income taxes for the year. Youll need it to show exactly how much HELOC interest youve paid during the year.

- Schedule A (Form 1040): Youll need this form to itemize the mortgage interest deduction on your tax return. Use Schedule E to deduct interest on your second home if you use it as a rental property, including improvements you make using HELOC funds.

- Proof of eligible expenses: Collect all receipts and invoices that prove you used HELOC funds to buy, build or improve the home that secured the HELOC. This includes receipts for completed work, materials, labor and permits. Its also wise to save your bank statements that prove how the funds were used.

Tax laws change every year, so consult with a tax professional to make sure you have the most up-to-date information and necessary documents.

Is HELOC Interest Tax Deductible?

FAQ

How much HELOC interest is tax-deductible?

For mortgages or HELOCs taken out after December 15, 2017, the IRS allows you to deduct up to $750,000 ($375,000 if married filing separately) of your interest payments as long as the funds were used to “buy, build, or substantially improve.” It’s important to note these limits apply to the combined home mortgage debt …

What are the disadvantages of a home equity line of credit?

Cons of a HELOC

Variable interest rates: Although HELOCs typically come with lower interest rates, the rates they carry are usually variable, similar to a credit card. This means your interest obligation can swing drastically from month to month, depending on changes to the prime rate.

Does a HELOC increase your taxes?

Funds received from HELOCs are not considered taxable income by the IRS. Therefore, you should not need to pay income taxes on the amount you borrow.Mar 4, 2025

Is interest on a HELOC tax-deductible in 2025?

For tax years before 2018 and after 2025, for home equity loans or lines of credit secured by your main home or second home, interest you pay on the borrowed funds may be deductible, subject to certain dollar limitations, regardless of how you use the loan proceeds.