For many homeowners, home loans from the Federal Housing Administration (FHA) make homeownership attainable and affordable. This type of home loan has less stringent requirements than conventional loans. But while the requirements are more flexible, FHA mortgages still have requirements home buyers must meet, including paying closing costs.

If youâre considering an FHA loan to purchase a home, you should acquaint yourself with the rules around closing costs. Letâs take a closer look at FHA loan closing costs and everything they include.

When buying a home, closing costs are an unavoidable expense that come on top of your down payment. Both FHA loans and conventional loans require you to pay closing costs, which include origination fees, appraisal fees, title fees, and more.

But are the closing costs actually higher with an FHA loan compared to a conventional loan? Let’s take a closer look

What are Closing Costs?

Closing costs refer to the various fees charged by lenders and third parties to process underwrite and close your mortgage loan. They are paid at closing, along with your down payment.

Closing costs typically range from 2-5% of the total loan amount for both FHA and conventional loans. For example, on a $300,000 mortgage, you may pay $6,000 – $15,000 in closing costs.

Here are some common closing costs for both loan types:

-

Origination fees – Compensates the lender for processing the loan application. Usually 0.5-1% of the loan amount.

-

Appraisal fee – Covers the cost of appraising the home. Typically $500-$1,000.

-

Credit report fee – Charged for pulling your credit report. Around $50 per applicant.

-

Title fees – Paid to the title company for doing a title search and providing title insurance. Usually $1,000-$2,000.

-

Recording fees – Charged by the local government to record the deed transfer. Varies by location but often $100-$300.

-

Prepaids – Upfront payments into escrow for property taxes and homeowners insurance. Varies based on location and policy details.

The specific closing costs you pay can vary by lender, state, and other factors. Your Loan Estimate breaks down all estimated fees.

Upfront Mortgage Insurance Premiums

One key difference between FHA and conventional loans is that FHA borrowers must pay an upfront mortgage insurance premium (UFMIP) at closing.

-

For FHA loans, the UFMIP is set at 1.75% of the loan amount. On a $300,000 loan, that’s $5,250.

-

Conventional loans don’t have an upfront mortgage insurance premium. You may have to pay monthly mortgage insurance premiums, but there’s no upfront fee.

This upfront premium does contribute to FHA closing costs typically being a bit higher overall compared to conventional loans.

Estimated Closing Costs Comparison

To illustrate the typical differences in closing costs, let’s look at two hypothetical loan estimates for a $300,000 purchase price and 20% down payment:

FHA Loan Estimate

- Origination charges: $2,000

- Services you can shop for: $2,500

- Services you can’t shop for: $3,250

- Taxes and other government fees: $750

- Prepaids: $2,000

- Upfront MIP: $5,250

- Total closing costs: $15,750 (5.25% of loan amount)

Conventional Loan Estimate

- Origination charges: $2,500

- Services you can shop for: $2,000

- Services you can’t shop for: $3,500

- Taxes and other government fees: $500

- Prepaids: $2,500

- No upfront MIP

- Total closing costs: $11,000 (3.67% of loan amount)

In this example, the FHA loan closing costs are $4,750 higher than the conventional loan, primarily driven by the UFMIP.

However, actual closing costs will depend on the specifics of your transaction. Some conventional lenders charge higher origination fees, and third-party fees can vary greatly by area.

How to Minimize Closing Costs

While FHA borrowers do need to budget for the UFMIP, there are ways to reduce other closing costs:

-

Shop around: Compare multiple lender quotes and negotiate lender fees.

-

Get seller credits: Sellers can cover up to 6% of closing costs on FHA loans.

-

Pay points: Paying points reduces the interest rate but increases closing costs.

-

Use gift funds: Get financial gifts from family members to help cover costs.

-

Seek down payment assistance: Many nonprofits and state/local programs offer help with closing costs.

-

Roll costs into loan: You can finance closing costs through a higher loan amount.

Carefully weighing the pros and cons of both loan types for your situation can help you make the most cost-effective decision. Speak to a loan officer to get personalized quotes and advice.

While FHA loans do have moderately higher closing costs, they offer more flexible credit and down payment requirements, making them advantageous for many buyers. For borrowers with excellent credit and a 20% down payment, a conventional loan may have lower overall costs.

The Bottom Line

Due to the upfront mortgage insurance premium, closing costs on FHA loans are typically a bit higher compared to conventional loans. However, the exact fees vary by lender and location.

To minimize your closing costs on an FHA loan:

-

Shop around and compare quotes

-

See if the seller can cover some fees

-

Look into down payment assistance programs

-

Consider paying discount points for a lower rate

With some smart planning and shopping around, you can keep your FHA closing costs reasonable. Speak to a lender to weigh up your loan options and get personalized quotes.

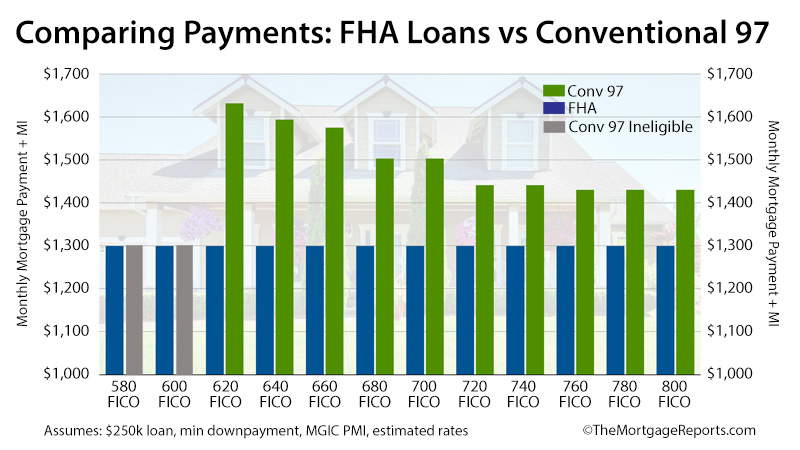

Is it harder to get an FHA loan than a conventional loan?

Because the federal government backs FHA loans, you may think there will be more stringent requirements than there are with conventional mortgages. However, you can qualify for an FHA loan with a lower credit score and a lower down payment than a conventional loan.

Can I roll closing costs into my FHA loan?

Yes, you can roll some or all your closing costs into an FHA mortgage. Itâs sometimes referred to as a no-closing-cost mortgage. Rolling your closing costs into your FHA mortgage will lower your upfront payment but raise your monthly mortgage payment. Youâll also pay interest on the higher monthly amount, making the loan more expensive in the long run.

FHA Loan vs. Conventional Loans (Mortgage): The Pros and Cons Before You Choose | NerdWallet

FAQ

Why are FHA closing costs so high?

Your closing costs are so high because of the property taxes, transfer tax, origination fee, and VA funding fee. I’m guessing you are not a disabled veteran since you’re paying the funding fee?

How much are closing costs for FHA vs conventional?

FHA loan closing costs typically range from 2% to 6% of your total loan amount, meaning on a $300,000 loan, you could pay between $6,000 and $18,000. FHA loan closing costs are similar to those of conventional loans.

How much do I need to make to buy a $300K house with an FHA loan?

To buy a $300K house, you’ll generally need to earn a household income around $80,000 per year, assuming 20% down, a 6.5% interest rate, and moderate existing debts.

Why do sellers not want FHA loans?

Some sellers may be hesitant to accept an FHA offer due to the perception that FHA loans take longer to close or have stricter property requirements; having …

What are FHA closing costs?

They include lender charges, like the origination fee, and fees for third-party services, such as title insurance and the appraisal. In the case of an FHA loan, closing costs involve a fee specific to the FHA loan program: mortgage insurance premiums (MIP). We’ll talk more about those shortly.

Is an FHA loan more expensive than a conventional loan?

However, this doesn’t mean an FHA loan will be less expensive in the long run. Conventional loans might have slightly higher interest rates, but often have lower fees and closing costs than FHA loans — meaning the annual percentage rate (APR) is generally lower.

Can I roll FHA closing costs into my mortgage?

You can roll FHA closing costs into your mortgage, but then you’ll pay interest on these charges. What are FHA closing costs? FHA loan closing costs — like closing costs on a conventional loan — are upfront expenses that homebuyers pay to finalize the home sale.

Are FHA closing costs the same as a down payment?

FHA loan closing costs are not the same as the down payment. The closing costs include charges like the origination fee, mortgage points and third-party services, like the appraisal. The down payment, on the other hand, is the portion of the home’s purchase price you’re paying upfront, rather than financing with the loan.

Is FHA better than conventional?

If your credit score is below 680 or your debt-to-income ratio (DTI) is higher (up to 50%), an FHA loan vs conventional loan might be the better choice. However, if your credit score is higher, a conventional loan vs FHA often offers lower interest rates and monthly mortgage repayments. Can you switch from FHA to conventional?

How much does an FHA loan cost?

Because FHA closing costs include the upfront MIP, an FHA loan can have average closing costs on the higher end of the typical 3% – 6% range. That doesn’t diminish in any way the value of getting an FHA mortgage, with its low down payment, lower interest rates and flexible underwriting. Ready to apply for your FHA or conventional loan?