Hey there, friend! If you’re wondering, “How often does my credit score go up?” you ain’t alone We’ve all been there, staring at that three-digit number like it’s the key to our dreams, hoping for a bump Well, I’m here to break it down for ya in plain English. Spoiler alert there’s no magic clock ticking for score increases, but they do update—usually monthly—and whether they go up depends on your money moves. Stick with me, and I’ll spill all the deets on how this works, what can nudge that score higher, and how to keep tabs on it without losing your mind.

The Basics: When Do Credit Scores Update?

Let’s get straight to the meat of it Your credit score doesn’t just pop up or down on a set day like clockwork It’s tied to your credit reports, which are like a financial report card from the big three bureaus—Equifax, TransUnion, and Experian. These reports get refreshed when lenders and creditors send in new info about your accounts. Most of ‘em report every 30 to 45 days, often around your billing cycle or statement date. So, in a nutshell, your score can update at least once a month, sometimes more if you’ve got multiple lenders dropping updates at different times.

But here’s the kicker an update don’t mean your score will go up. It might stay the same or even dip, depending on what’s reported Things like paying bills on time or cutting down debt can push it higher, while late payments or maxing out cards can tank it We’ll dig into that more in a sec. For now, just know that monthly updates are the norm, but the exact timing? Kinda all over the place since every lender has their own schedule.

Why Ain’t My Score Going Up Every Month?

Alright, let’s tackle the big frustration. You’re checking your score, seeing it update, but it’s stuck or—worse—dropping. What gives? Here’s the real talk: credit scores ain’t a straight line up. They’re more like a rollercoaster, reacting to your financial habits and what’s on those reports. For your score to climb, the info in your report has gotta show positive stuff. Let me break down why it might not be budging:

- Lenders Don’t Always Report Good News Fast: Even if you paid off a chunk of debt, your lender might not tell the bureaus right away. Some only report once a month, others drag their feet. So, your hard work might not show up yet.

- Negative Stuff Lingers: Got a late payment from a while back? That junk sticks on your report for up to seven years. It drags your score down, even if you’re killing it now.

- Credit Mix or Age of Accounts: If you close an old card or pay off a loan, it might mess with the diversity of your credit or the average age of your accounts. Weird, right? But it can lower your score temporary.

- Utilization Still High: Using too much of your available credit—even if you pay on time—can keep your score from rising. Aim to keep it under 30% of your limit.

So, while scores update often, going “up” depends on what’s new in your report. It’s less about frequency and more about your actions stacking up over time.

What Makes a Credit Score Go Up, Anyway?

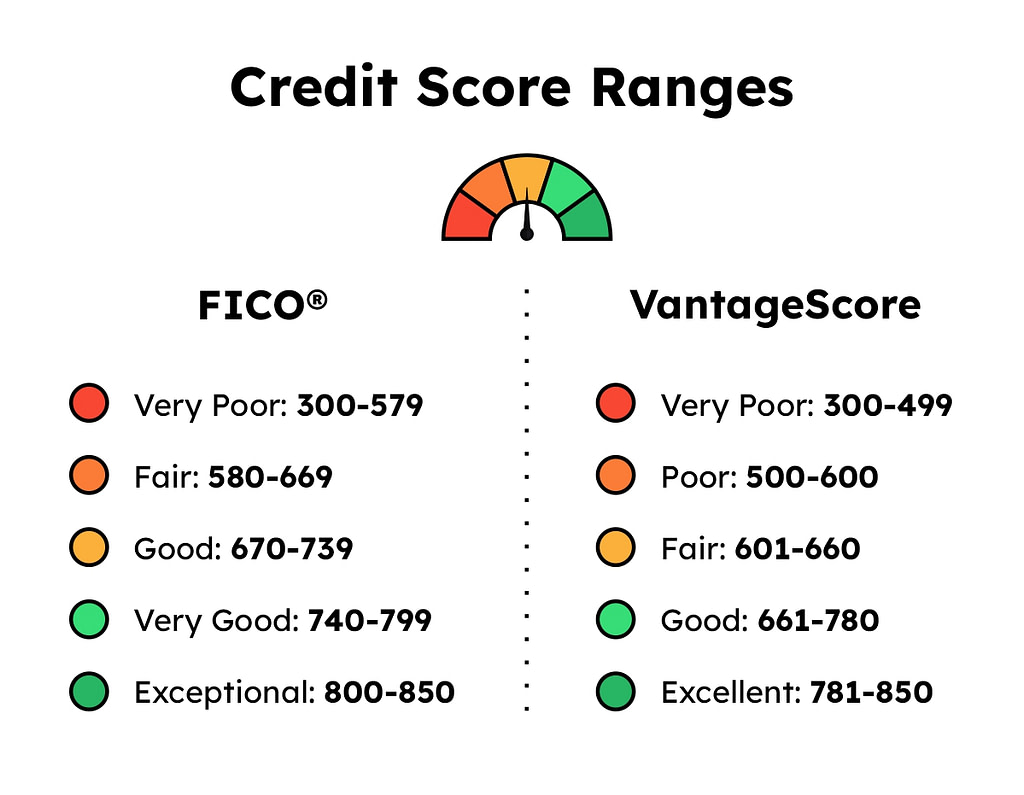

Now that we got the timing down, let’s chat about what actually pushes that number north. Credit scores, whether it’s FICO or VantageScore, are calculated using a few key factors from your reports. I ain’t gonna bore ya with math, but here’s the stuff that matters most:

- Payment History (Biggest Deal): Paying bills on time, every dang time, is the golden ticket. This is like 35% of your score with FICO. Miss a payment by 30 days or more, and it’s a gut punch to your score.

- Credit Utilization (Second Biggest): This is how much of your credit limit you’re using. Keep it low—under 30% is the sweet spot. Got a $1,000 limit? Don’t owe more than $300. This is about 30% of your score.

- Length of Credit History: Older accounts look good. They show you’ve been handling credit for a while. Don’t close your oldest card, even if you don’t use it much.

- Credit Mix: Having different types of credit—like a credit card and a car loan—can help. It shows you can juggle different debts.

- New Credit: Applying for too much new credit at once can spook lenders. Space out applications, maybe every six months or so.

If you’re nailing these, especially payments and utilization, your score can creep up with each report update. But it ain’t instant. It’s a slow grind, fam.

Here’s a quick table to show how these factors weigh in (based on FICO, since it’s super common):

| Factor | Weight in Score | Quick Tip |

|---|---|---|

| Payment History | 35% | Pay on time, no excuses! |

| Credit Utilization | 30% | Keep balances low compared to limits. |

| Length of Credit History | 15% | Hold onto old accounts. |

| Credit Mix | 10% | Mix cards and loans if ya can. |

| New Credit | 10% | Don’t apply for too much too fast. |

How Can I Make My Score Go Up More Often?

Alright, let’s get practical. You want that score to climb, and I’m gonna give ya some straight-up tips to make it happen. These ain’t overnight fixes, but they stack up over months. Here’s what me and my crew at our lil’ financial hangout suggest:

- Pay Bills Like Your Life Depends on It: Set reminders, automate payments, whatever it takes. One late payment can haunt ya for years. Get current fast if you’re behind.

- Slash That Debt: Focus on high-interest cards first. Pay more than the minimum. If you get a bonus or extra cash, throw it at your balance to drop that utilization rate.

- Don’t Max Out Cards: Keep your spending in check. If you’re close to the limit, stop swiping ‘til you pay it down. Simple but effective.

- Check Your Reports for Goofs: Errors happen. Maybe a paid-off debt still shows as open. Dispute that junk with the bureaus. You can get free weekly reports at a certain well-known site—look it up!

- Avoid New Credit Unless Needed: Each application can ding your score a bit with a hard inquiry. Only apply when it’s worth it, like for a mortgage.

- Consider a Credit Builder Trick: If your score is low, look into secured cards or small loans designed to build credit. Use ‘em responsibly, and they can help.

I remember when I was tryna boost my score after a rough patch. I had a card with a $500 limit, and I was always at $490. Dumb, right? Once I paid it down to $100 and kept it there, I saw a jump in a couple months. Patience pays off.

Busting Myths: It Ain’t Always Gonna Skyrocket

Let’s clear up some nonsense I hear all the time. People think, “I paid off my debt, why didn’t my score shoot up 100 points?” or “Shouldn’t it go up every week?” Nah, it don’t work like that. Here’s the real deal on some myths:

- Myth 1: Paying Off Debt Always Boosts Your Score: Sometimes, paying off a loan can lower your credit mix or age of accounts. It might dip before it rises. Don’t panic; keep at it.

- Myth 2: Scores Update on the Same Day: There’s no universal “update day.” Depends on when your lenders report. Could be the 5th for one, the 20th for another.

- Myth 3: Checking Your Score Hurts It: Checking your own score is fine—it’s a soft inquiry. Only hard pulls, like for a loan, might nudge it down a tad.

- Myth 4: One Good Move Fixes Everything: A single on-time payment won’t erase years of mess-ups. It’s a long game. Consistency is key.

I’ve had buddies swear they’d see a huge leap after one big payment, only to be bummed out. I tell ‘em, “Keep pluggin’ away; it adds up.”

How to Keep Tabs on Your Score Without Stressin’

Since scores update monthly-ish, you gotta keep an eye on ‘em to spot trends. But don’t obsess—checking every day won’t make it move faster. Here’s how to stay in the loop without losing sleep:

- Sign Up for Free Monitoring Tools: There’s apps and services out there that track your score, some even daily, without dinging it. They often use VantageScore or FICO based on one bureau’s data. Super handy.

- Pull Your Reports Regularly: You can grab free credit reports weekly from the big three. Look for errors or surprises. Dispute anything funky.

- Set Alerts: Some tools notify ya when your score changes or if something weird pops up, like a new account you didn’t open. That’s a lifesaver for catching fraud.

- Use Simulators if Available: Some platforms let ya play with “what if” scenarios—like paying off a card—to see potential score changes. It’s like a crystal ball, sorta.

I’ve been using a free tool for a while now, and it’s dope to see even small jumps. Makes me feel like I’m getting somewhere, ya know?

What If My Score Drops After an Update?

This one stinks, but it happens. You’re expecting a nice lil’ increase, and bam—down it goes. Don’t freak out just yet. Here’s why it might drop and what to do:

- Late Payment Reported: If you missed a bill by 30 days or more, it can slash your score hard. Get current ASAP. The damage lessens over time if you stay on track.

- High Utilization Spike: Did ya rack up a big balance recently? That can hurt. Pay it down quick to recover.

- New Hard Inquiry: Applied for credit? That can lower it a few points, but it’s temporary.

- Something Fishy: Big, unexplained drops might mean identity theft. Check your reports for accounts you don’t recognize and freeze your credit if needed.

I had a drop once ‘cause I forgot a tiny medical bill. Got it sorted, paid up, and my score bounced back in a few months. Mistakes happen; just fix ‘em quick.

The Long Game: Building Credit That Sticks

Look, I ain’t gonna sugarcoat it—building a better score and seeing it go up regular-like takes time. It’s not a sprint; it’s a dang marathon. But every step counts. Focus on the habits I mentioned—paying on time, keeping debt low, and being smart with new credit. Over months and years, those updates will start showing higher numbers more often.

Think of it like planting a garden. You don’t see blooms the next day, but with steady care, you get a killer harvest. Same with credit. I’ve seen folks go from the low 500s to over 700 in a couple years just by sticking to the basics. Heck, I’ve been there myself, clawing my way up after some dumb young-adult decisions.

Special Cases: Can You Speed Up Updates?

Now, there’s a lil’ somethin’ called “rapid rescoring” I’ve heard about, mostly for mortgages. If you’re tryna buy a house and need a quick score boost—like after paying down a card—you can ask a lender to rush updated info to the bureaus. It ain’t standard, and you can’t do it yourself; gotta go through the lender. Otherwise, you’re stuck with the usual 30-45 day wait for updates. Just a heads-up if you’re in a pinch.

Wrapping It Up: Keep Your Eye on the Prize

So, how often does your credit score go up? Well, updates happen at least monthly for most folks, sometimes more, based on when lenders report to the bureaus. But whether it climbs depends on you—your payments, your debt, your habits. It ain’t always gonna rise with every update, and that’s okay. Focus on the long haul, make smart money moves, and check your progress without stressin’ too much.

We’re all in this financial game together, and I’m rootin’ for ya to see that score soar. Got questions or wanna share your own credit journey? Drop a comment below—I’d love to chat. Keep hustlin’, and remember, every lil’ win adds up to big gains!

How often your credit score updates

Credit scores continually go up and down as information on your credit report gets updated. New balance amounts, bill payments and account openings are only a few factors that appear on your credit report and influence your credit score.

You can generally expect your credit score to update at least once a month, but it can be more frequently if you have multiple financial products. Each time any one of your creditors sends information to any of the three main credit bureaus — Experian, Equifax and TransUnion — your score may refresh.

That means your creditor may send updated information to Experian today, then Equifax next week, and TransUnion the following, which creates variations in your credit score.

Taking a look at my recent credit score updates through *Experian Boost®, my score changed four times in October. The fluctuations were due to a new auto loan being reported on my credit report, as well as changes in my credit card balances.

Your credit score may also fluctuate when you check different credit score services that work with different credit bureaus. As stated above, the credit bureaus may receive information at varying times throughout the month, so if you check your scores with Experian and TransUnion today, they may differ if one has info the other doesnt.

Credit scores are a key piece of your financial history. If you want to track your progress, here’s how long you’ll need to wait for your credit score to update.Updated Thu, Oct 31 2024

If you’re looking to buy a new home or take out an auto loan, you may be checking your credit score every day leading up to your application to see where it stands. But just because you check it often doesn’t mean there will be an update.

Credit scores refresh at different times throughout the month and there may be times where it takes a few days or weeks before your score updates. And even if you check it today and go to apply for a loan or credit card tomorrow, your score may change.

Here’s when you can expect your credit score to update and where to check your credit score for free.

How to RAISE Your Credit Score Quickly (Guaranteed!)

FAQ

How fast will a credit score go up?

| Event | Average credit score recovery time |

|---|---|

| Missed/defaulted payment | 18 months |

| Late mortgage payment (30 to 90 days) | 9 months |

| Closing credit card account | 3 months |

| Maxed credit card account | 3 months |

How rare is a 700 credit score?

Can your credit score go up 50 points in a month?

Unfortunately, no. While some steps can help your score improve faster than others, it can still take time for your efforts to be reported to the credit bureaus. If you need to improve your credit score for a loan or credit card application, it’s recommended that you start taking steps several months in advance.

How often can credit scores increase?

You can generally expect your credit score to update at least once a month, but it can be more frequently if you have multiple financial products. Each time any one of your creditors sends information to any of the three main credit bureaus — Experian, Equifax and TransUnion — your score may refresh.

How often does my credit score update?

Again, your credit score could potentially update on any day of the month, and possibly more than once a month. It depends on how many creditors you have and when they report. In other words: You can’t always time your credit card or loan payments to a specific day of the month for maximum impact.

Do credit scores change over time?

Keep in mind that credit scores change over time. “High” credit scores can drop if you miss payments or maintain high balances on your cards. “Low” credit can get better if you consistently make payments on time. If you’ve never borrowed money before, a credit card can be a smart way to start to develop a good credit rating.

When will my credit score be updated?

Generally speaking, there is no set date each month when you can expect your credit scores to be updated. It all depends on when your lender sends information to the credit bureaus, when those bureaus update their reports and when credit-scoring companies use those reports to update their scores. What is rapid rescoring?