A credit card account can affect your credit for years after you close the account. Its effect on your credit score, however, isn’t always straightforward. Read on to learn when closed accounts are negatively impacting your credit score on your credit report, and how you might address them when necessary.

Your credit report contains a wealth of information about your financial history, including details on both open and closed credit accounts But how long do closed accounts actually stick around on your report after you stop using them?

The answer depends on several factors, which we’ll explore in this article. Read on to learn more about how closed accounts are reported, how long they remain on your credit report, and how they impact your credit scores over time.

An Overview of Closed Accounts on Credit Reports

First, let’s clarify exactly what it means when an account is closed. An account is considered closed when it can no longer be used – for example, when you pay off a loan in full or cancel a credit card. Accounts may be closed by you, the consumer, or by the creditor.

Closed accounts remain on your credit report for a period of time even after they are no longer active. The closed account status is noted on your credit report along with other key details like the date opened, credit limit or loan amount, and your payment history.

Payment history on both open and closed accounts is a major factor that affects your credit scores. On-time payments can continue to benefit your credit long after an account is closed, while late payments can negatively impact your scores.

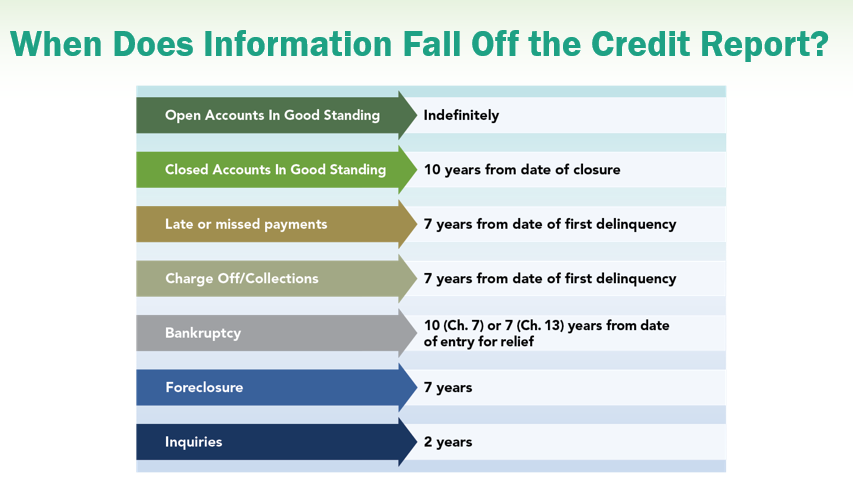

How Long Do Closed Accounts Stay on Your Credit Report?

The length of time a closed account remains on your credit report depends on two key factors:

1. Account Status

- Accounts closed in good standing – Remain for 10 years from date of closure

- Accounts closed with derogatory marks – Remain for 7 years from the date of first delinquency leading to closure

An account in good standing means it does not have any negative marks like late payments, collections or charge-offs. As long as you kept the account current before it was closed it will have a maximum 10 year reporting period.

Derogatory marks like missed payments can reduce the reporting period to 7 years from the date of your first late payment on that account. This is because negative information typically falls off your report after 7 years.

2. Type of Account

- Installment loans – Remain for 10 years from date paid in full

- Revolving credit cards – Remain for 10 years from date of closure

- Collections – Remain for 7 years from date of first delinquency

- Public records – Bankruptcy remains for 10 years, other public records remain for 7 years

Installment loans like mortgages, student loans, and auto loans follow the 10 year rule from the date they are paid in full. Revolving credit cards also remain for up to 10 years after being closed.

Collections and most other public records fall off after 7 years, while Chapter 7 bankruptcies stay on your report for a full decade from filing date.

How Closed Accounts Affect Your Credit Scores

The effect closed accounts have on your credit scores varies depending on the payment history and other factors:

- Accounts closed in good standing – Continue to benefit credit for 10 years

- Accounts closed with late payments – Hurt scores for up to 7 years

- Voluntary closure of unused card – Potential for indirect damage from reduced credit history and higher utilization

As mentioned, on-time payment history is valuable long after an account is closed. But if you missed payments before closure, that negative information persists for 7 years and can drag down your credit scores.

Even closing an old card you don’t use anymore could indirectly hurt your credit if it reduces the average age of your accounts or increases your overall credit utilization. Be cautious before closing unused cards that still have a positive history.

Tips for Removing Closed Accounts from Your Credit Report

If you have a closed account with negative marks that is hurting your credit, you may want to try removing it from your credit reports. Here are some options:

-

Dispute errors – If the information is inaccurate, file disputes with each credit bureau to correct errors. This may lead to removal of incorrect accounts.

-

Goodwill deletion – You can send goodwill letters asking creditors to remove accounts as a courtesy. Success is not guaranteed.

-

Wait for automatic removal – Closed accounts eventually fall off your report automatically after the reporting timelines expire.

Don’t attempt to remove accounts that are closed in good standing, as these are helping your credit. Be patient and continue practicing good credit habits going forward.

How to Improve Your Credit with Closed Accounts

Here are some tips for managing closed accounts and improving your credit scores over time:

- Make all loan and credit card payments on time, every time

- Pay down balances on revolving credit to lower utilization

- Leave old accounts open unless there is a specific need to close them

- Monitor your credit reports and dispute any errors

- Limit new credit applications to only when needed

Staying on top of your payments, even for closed accounts, is critical for credit health. Keeping credit card balances low also helps improve utilization. Leave accounts open unless they have annual fees, for example, to preserve your overall credit history.

Be sure to check credit reports regularly and dispute inaccuracies in order to maximize your scores. Limiting new credit applications also helps. Following these tips can help you manage closed accounts properly and build your scores.

The Bottom Line

Does closing a credit card impact your credit utilization ratio?

Your credit utilization ratio refers to the total percentage of available credit you use at a given moment. High credit utilization ratios can lower your credit score. When you close a credit card account, you reduce your total available credit by that card’s credit limit. That change could increase your credit utilization ratio, especially if you carry a balance on your other credit cards. Before you close an account, it’s helpful to consider the impact.

Does a closed account affect your credit score?

A closed account can affect your credit score for as long as the account appears on your credit report. Your credit score is calculated based on the following factors from your credit report: payment history, amounts owed, length of credit history, credit mix, and new credit. Closing an account may affect your credit score by affecting those factors.

How Long Do Closed Accounts Stay On A Credit Report? – CreditGuide360.com

FAQ

How long do closed credit cards stay on your credit report?

Closed credit card accounts can stay on your credit report for seven to 10 years, depending on certain factors. You can try to remove closed accounts from your credit report by disputing any inaccuracies, sending a “goodwill letter” or simply waiting for the account to fall off automatically.

How long does a bank account stay on your credit report?

“Accounts will age off credit reports after seven or 10 years, depending on the status of the account,” she says. Accounts closed in good standing may stay on your credit report for up to 10 years, which generally helps your credit score. Those with adverse information may remain on your credit report for up to seven years.

How long do closed accounts stay on a credit report?

Items on credit reports, including accounts that have been closed, can remain on a credit report for around seven to 10 years. So if you’re worried about an older closed account with negative information that is potentially lowering your score, know that eventually it will drop off your credit report.

How long does a closed account affect my credit score?

A closed account can affect your credit score for as long as the account appears on your credit report. Your credit score is calculated based on the following factors from your credit report: payment history, amounts owed, length of credit history, credit mix, and new credit.

Are closed accounts on your credit report?

Unless you have a very limited credit history, your credit report is probably full of data about closed accounts, like loans and credit cards you paid off years ago. When your score changes, our app tells you why — and suggests what to do in the future. How long do closed accounts stay on your credit report?

How long does a payment history stay on your credit report?

Generally speaking, if an account’s payment history helps your credit score, it will stay on your credit reports for 10 years after it is closed.