This article contains general information and is not intended to provide information that is specific to American Express products and services. Similar products and services offered by different companies will have different features and you should always read about product details before acquiring any financial product.

Understand how closed accounts on credit reports may impact your credit score. Find out how to manage and remove a closed account.

No matter how closely you pay attention to your financial history, closed accounts can appear on anyone’s credit report. It may be a credit card you haven’t used in many years, a loan you paid off, or even a mistake by a creditor or the credit bureau. Whatever the reason, a closed account can affect your credit score positively or negatively depending on the specifics of the account. But there are often ways to manage closed accounts – or even remove them from your credit report.

Having a good credit score is important for getting approved for loans and credit cards with the best terms. One question that often comes up is whether paying off closed accounts will help improve your credit score. In this article, we’ll take a detailed look at how paying off closed accounts affects your credit so you can make informed decisions.

What Are Closed Accounts?

First, let’s define what closed accounts are. Closed accounts refer to credit cards or loans that are no longer active This usually happens for a few reasons

-

You close the account – You voluntarily close the credit card or loan This can happen if you want to consolidate accounts or no longer need that line of credit

-

The lender closes the account – The bank or lender closes the account, often due to inactivity or risk of default.

-

The account is charged-off – After several months of non-payment, the lender writes the account off as a loss, closing it.

Does Paying Off Closed Accounts Help Your Credit Score?

In most cases, paying off a closed account does not immediately improve your credit score However, it can help in the long run by removing negative information from your credit history. Here are some key points

-

Paying a charged-off account – If the account has been charged off but not sold to collections, paying it off removes the negative status. But it takes time for your scores to reflect the change.

-

Paying sold debt – If the debt has been sold to collections, pay the collection agency. This will update the status to “paid collection” which is better but still negative.

-

Eliminating debt – Less revolving debt improves your credit utilization ratio, a key factor in credit scores. This helps over time.

-

Won’t change account status – Paying a closed account does not change the fact that the account was closed, which remains negative.

Other Ways Closed Accounts Impact Your Credit

Beyond whether paying off the balance helps, closed accounts can impact your credit in other ways too:

-

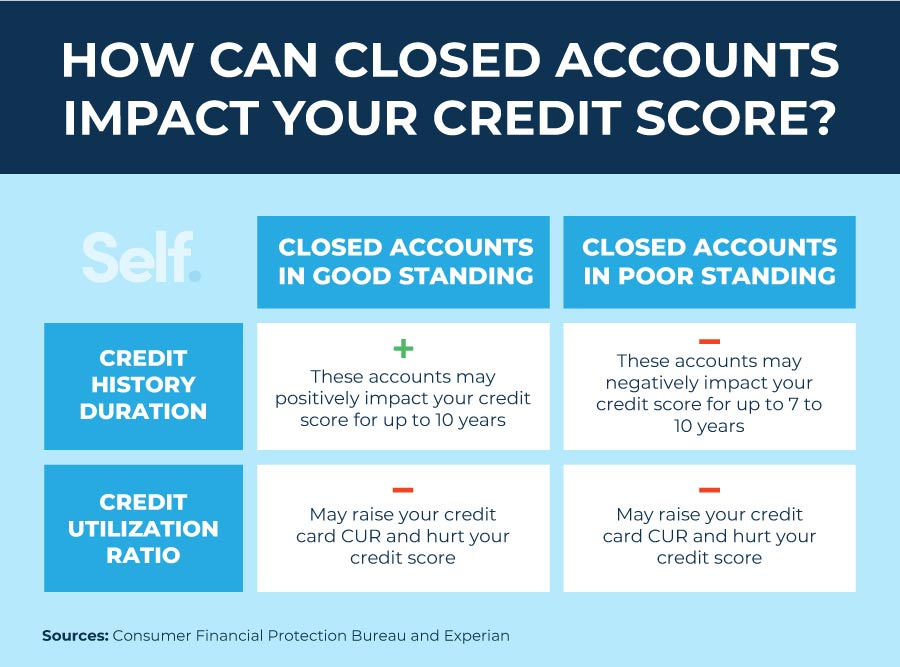

Credit history – Closed accounts remain on your credit reports and contribute to length of credit history for 10 years. This is generally positive.

-

Credit mix – Having different types of credit (credit cards, loans, mortgages, etc.) helps your credit mix. Closing accounts impacts this mix.

-

Lowered credit limits – Since closed accounts no longer count towards your total credit limit, this can negatively impact your utilization ratio.

-

New credit applications – Applying for new credit to replace closed accounts causes hard inquiries, which temporarily lower your scores.

As you can see, closed accounts can positively or negatively influence your credit in direct and indirect ways. The impact depends on your specific credit situation.

Tips for Managing Closed Accounts

If you have closed accounts that you want to pay off, here are some tips:

-

Pay charge-offs directly to the original creditor if possible, or get validation of the debt if sold.

-

Make sure payments are recorded properly by checking your credit reports regularly.

-

Consider asking creditors to “re-age” accounts to erase some negative history once paid off.

-

Don’t close old accounts as these help your length of credit history.

-

If you do close an account, reduce balances on other cards to minimize utilization effects.

-

Be cautious about opening new accounts and inquiries. Space these out over time.

-

Maintain low balances and make all payments on time going forward to offset negative impacts.

With some diligence, you can minimize damage from closed accounts and work toward rebuilding your credit over time. Paying off closed account balances is one small piece of the overall puzzle.

The Bottom Line

How to Get Rid of Closed Accounts on Your Credit Report

There are a few ways to go about getting a closed account off your credit report. If the closed account is an error – or fraudulent – then the credit bureaus and information providers must correct the information in your credit report. If the closed account is verifiable and legitimate – and has negative information like an outstanding balance or a history of late or missed payments – you still have a few options to remove it:

- Pay for delete: In some cases, the lender may agree to remove the negative information from your credit report if you pay the remaining balance, in installments or in full. However, lenders aren’t obligated to do so.

- Goodwill deletion: You request that the information furnisher removes the negative item out of pure goodwill. This option isn’t always successful, but it’s worth pursuing because the furnisher may remove the negative item if you provide them with good enough reason to believe that the negative behavior won’t recur in the future. For instance, if you have an otherwise clean credit history.

- Wait: While not the quickest solution, it’s always successful. But 7-to-10 years can be too long for most people to wait, especially if you need to take steps to help improve your credit, and ideally, relatively quickly. If you do choose to wait, though, the information just goes away.

How Closed Accounts Affect Your Credit Score

How closed accounts affect your credit score can seem a bit contradictory to what you might think. For instance, paying off an auto or home loan is considered a good thing, financially. But it can result in a temporary dip in your score because it reduces the variety of credit types in your mix. Lenders usually prefer borrowers who have learned to handle a good mix of loans and credit lines. If you don’t use a credit card, it may seem logical to close the account. But closing a credit card would lower your overall credit limit, which can raise your credit utilization and that, in turn, could negatively affect your credit score. Closed accounts with remaining balances – like a canceled credit card account with an outstanding balance – can also affect your score negatively. If the account defaulted, it could be transferred to a collection agency. Paying off closed accounts like these should improve your credit score, but you might not see an increase right away.

Paying Collections – Dave Ramsey Rant

FAQ

Will my credit score go up if I pay off a closed account?

Can paid closed accounts be removed from a credit report?

Closed credit card accounts can stay on your credit report for seven to 10 years, depending on certain factors. You can try to remove closed accounts from your credit report by disputing any inaccuracies, sending a “goodwill letter” or simply waiting for the account to fall off automatically.May 22, 2025

Is it good to pay a closed account?

Don’t Forget to Pay Off Your Closed Accounts

Paying off credit card debt — including debt from closed accounts — is one of the fastest ways to improve your credit score. If you aren’t sure if you have any closed accounts on your report, a credit-tracking app can help.

Will paying off and closing a credit card improve my score?