If buying a home is on your wish list for 2025, it’s important to understand the minimum mortgage requirements for the most common loan programs.

We’ll give you a quick tour of the loan landscape, so you know which loans come with the lowest credit score and down payment requirements, the highest loan limits and more. And if you’re carrying debt? We’ll also cover how much debt you can have and still qualify for each program.

Purchasing a home is an exciting milestone in life. However, qualifying for a mortgage can be challenging, especially for first-time homebuyers. If you’re wondering what is the easiest home loan to qualify for, this guide will walk you through the different types of mortgages and their qualification requirements.

Overview of Mortgage Types

There are several common mortgage options to consider

-

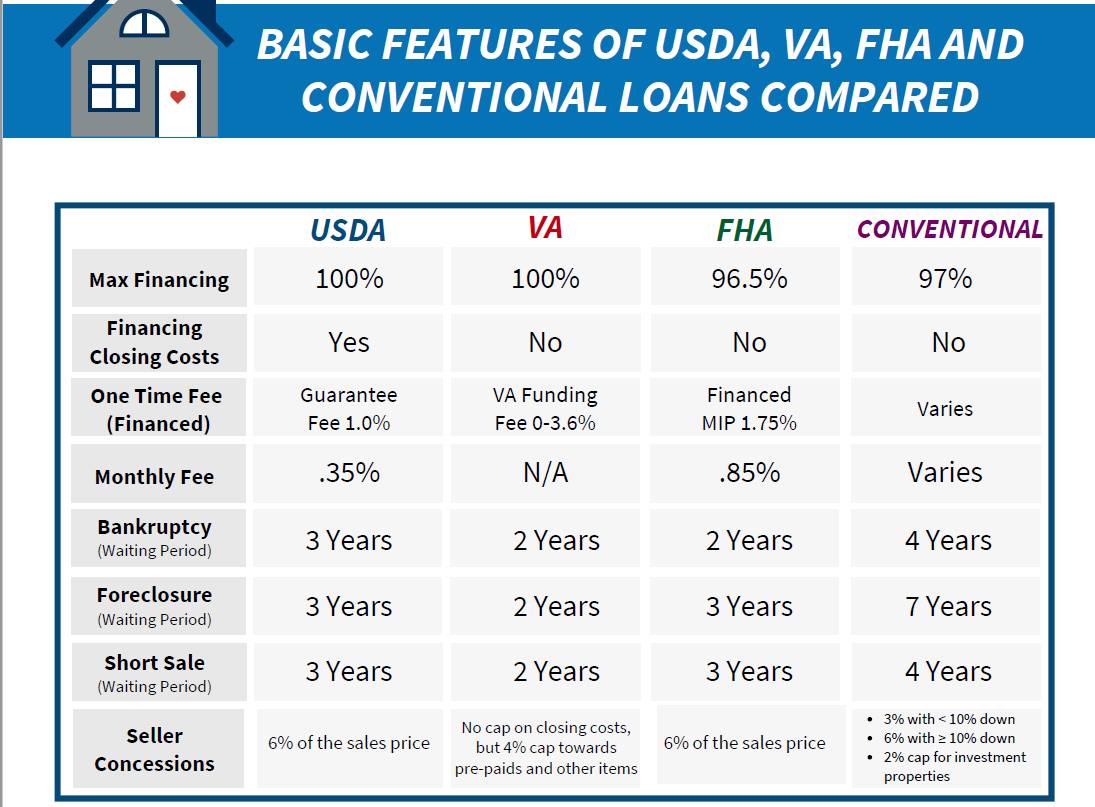

Conventional Loans – Offered by private lenders and not guaranteed by the government. Require a minimum credit score of 620.

-

FHA Loans – Backed by the Federal Housing Administration. Require a minimum credit score of 580 with 3.5% down payment.

-

VA Loans – Offered by private lenders but guaranteed by the VA Require no minimum credit score for veterans

-

USDA Loans – Guaranteed by the U.S. Department of Agriculture for rural properties. Typically require a 640 credit score.

-

Jumbo Loans – For luxury homes above conforming loan limits. Require higher credit and down payments.

-

Non-QM Loans – For those who don’t qualify for conventional loans. Offer alternative qualification methods.

The easiest mortgages to qualify for are generally government-backed loans like FHA VA and USDA loans. They offer more flexibility with credit scores, debt-to-income ratios, and down payments.

FHA Loans

FHA loans are a top choice for easy mortgage qualification. Here are the key advantages:

-

Minimum Credit Score: 500 with 10% down payment or 580 with 3.5% down

-

Down Payment: As low as 3.5%

-

Debt-to-Income Ratio: Up to 50% with compensating factors

To qualify for an FHA loan, you’ll need a steady income, employment history, and sufficient cash reserves. FHA loans allow gift funds and sweat equity for your down payment. Overall, FHA loans offer more lenient qualifications for those with less-than-perfect credit.

VA Loans

VA loans have flexible guidelines that make them one of the easiest mortgages to get. Benefits include:

-

Minimum Credit Score: No minimum but 620+ recommended

-

Down Payment: 0% with full entitlement

-

Debt-to-Income Ratio: Up to 41%

To qualify for a VA loan, you must be an eligible veteran, service member, or surviving spouse. VA loans require a VA funding fee instead of private mortgage insurance. Credit, income, and employment history are reviewed but minimums are quite low.

USDA Loans

For borrowers in rural locations, USDA loans offer easy qualification with:

-

Minimum Credit Score: Typically 640

-

Down Payment: 0%

-

Debt-to-Income Ratio: Up to 29% front-end

USDA loans are for low to moderate income borrowers purchasing homes in designated rural areas. You’ll need to meet income eligibility requirements based on the location. USDA loans can be a great option for rural properties.

Non-QM Loans

Non-QM or non-qualifying mortgages help those who don’t qualify for conventional loans. Options include:

-

Alternative income verification for self-employed, contractors, gig workers

-

Higher debt-to-income ratios up to 50%

-

Alternative credit data like rent and utility payment history

While credit scores and down payments may be higher, non-QM loans offer more flexibility on income and debt qualifications.

Tips to Improve Qualification Chances

Here are some tips to boost your chances of qualifying for the easiest home loan:

-

Improve your credit score – Pay bills on time and lower balances

-

Lower your debt-to-income ratio – Pay down debts and limit new credit

-

Make a larger down payment – Save 20% if possible to get the best rates/terms

-

Get pre-approved – Confirm you qualify and get details on requirements

-

Provide all documentation – Have pay stubs, tax returns, and bank statements ready

-

Work with a mortgage broker – They can help you find the right loan programs

-

Apply with multiple lenders – Improves your chances if one lender denies you

The easiest mortgage to qualify for depends on your specific financial situation. With some preparation, you can boost your chances of getting approved. FHA, VA, and USDA loans offer more flexibility but conventional loans have pros too. Discuss options with a lender to find the best home loan to fit your needs.

FHA mortgage requirements

It may be easier to qualify for an FHA loan — which is backed by the Federal Housing Administration (FHA) — than a conventional loan. FHA-approved lenders are protected against losses when you pay your mortgage insurance premiums. This extra insurance allows lenders to make loans to borrowers with lower credit scores and more debt than conventional loans, because the insurance covers their losses if the borrower defaults.

Borrowers struggling to qualify for a mortgage will have more FHA buying leverage in 2025: FHA loan limits increased to $524,225 for most parts of the country. Higher-cost areas get even more bang for the buck, with maximum loan amounts as high as $1,209,750.

Down payment. The minimum down payment is 3.5% with a minimum 580 credit score, or 10% with a score of 500 to 579.Mortgage insurance. FHA borrowers must pay two types of FHA mortgage insurance. The first is an upfront mortgage insurance premium (UFMIP) worth 1.75% of the loan amount, which is typically financed into the mortgage. The second is the annual mortgage insurance premium (MIP), which ranges from 0.15% to 0.75% of the loan amount, is divided by 12 and added to your monthly payment.Credit score. FHA loan guidelines set the lowest minimum credit score requirements of any standard loan program, allowing scores as low as 500 with a 10% down payment. A 580 score is required for borrowers making the minimum 3.5% down payment. FHA-approved lenders also use the Credit Alert Interactive Verification Reporting System (CAIVRS) to confirm you don’t have any delinquent federal debt, like student loans or unpaid child support.Employment. FHA lenders must look at the borrower’s income stability and employment history for the past two years. Job-hoppers and borrowers with gaps in their job history who apply for an FHA loan may have to provide extra documentation and explanations.Self-employment. You’ll need to document at least two years of self-employment for an FHA loan.Income limits. FHA guidelines don’t set any limits on qualifying income for an FHA loan.Debt-to-income ratio. For FHA loans, your DTI ratio max is 43%. This ratio considers your mortgage PITI payment (principal, interest, taxes and insurance) and all other revolving monthly debt, including car loans, credit card payments and other loans. You may be approved with a higher DTI ratio if you have strong credit scores or extra cash reserves. If you’re buying an energy-efficient home, you may qualify with a DTI ratio as high as 45%.Cash reserves. Cash reserves are liquid funds you may need to show you have “in reserve” to cover mortgage payments if needed. FHA loan qualifications don’t usually require cash reserves unless you’re buying a two- to four-unit home or trying to qualify with a lower credit score.Occupancy. You can only take out an FHA loan to buy a primary residence you intend to live in for at least one year.Property types. An FHA loan can be used to finance one- to four-unit homes, FHA-approved condominiums, cooperative units and manufactured homes affixed permanently to land.Home appraisals. You’ll need an appraisal to buy a home with an FHA loan, regardless of your down payment. FHA appraisal guidelines have stricter safety and habitability requirements, and FHA appraisals are more expensive than conventional home appraisals.

See current FHA loan rates today.

2025 minimum mortgage requirements by loan type

| Requirement | Conventional | FHA | VA | USDA |

|---|---|---|---|---|

| Down payment | 3% | 3.5% | 0% | 0% |

| Credit score | 620 |

|

No minimum, 620 is standard | No minimum, 640 is standard |

| Mortgage insurance or similar fee | PMI 0.14% to 2.33% |

|

1.40% to 3.60% VA funding fee |

|

| DTI ratio | 45% | 43% | 41% | 41% |

| Loan limit for a single-family homes | $766,550 to $1,149,825 | $498,257 to $1,724,725 depending on location | N/A with full VA entitlement | N/A |

The BEST First Time Home Buyer Loans To BUY YOUR FIRST HOME!

FAQ

What is the easiest mortgage to get approved for?

An FHA loan will typically be the easiest mortgage to qualify for. It offers the lowest credit score requirement — far lower than for a conventional loan — and requires only a 3.5% down payment.

What is the easiest loan to get approved for?

What is the minimum salary to get a home loan?

| Eligibility Criteria | Details |

|---|---|

| Nationality | Must be an Indian citizen |

| Age Limit (Salaried) | 23 to 65 years |

| Age Limit (Self-Employed) | 23 to 70 years |

| Minimum Income (Salaried) | ₹25,000/month* |

What is the easiest bank to get a mortgage with?

HSBC: Known for its simple online mortgage process, HSBC offers a range of products and caters to applicants with less than perfect credit scores, making it easier for many to qualify. Barclays: Barclays provides a variety of mortgage options, including deals for first-time buyers and remortgagers.

What is the easiest mortgage to get?

Jumbo loan (usually need 10%+ down payment, 680+ FICO, and asset reserves) FHA loans are the easiest mortgage to get because of the 3.5% down payment and 580 minimum FICO score required. Conforming loans are a close second, despite a lower 3% minimum down payment, due to the higher 620 minimum FICO score required.

What is the best loan to buy a house?

A conventional mortgage may be the best loan to buy a house if you have good credit and savings for a down payment. 2. FHA loans FHA loans are popular among first-time home buyers and those with lower credit scores, thanks to their low down payment requirements and flexible income guidelines.

What is the best mortgage loan for your credit score?

The best mortgage loan for your credit score depends on how high or low it is. FHA loans accept scores as low as 500 (with 10% down) or 580 (with 3.5% down). Conventional loans usually require 620 or higher, while jumbo loans may require 680+. Borrowers with good credit may qualify for better interest rates and lower origination fees.

What is the best home loan for first-time homebuyers?

The best home loan for first-time homebuyers depends on factors like credit score, down payment, and income. FHA loans are popular because they allow low credit scores and require just 3.5% down. Conventional loans with 3% down may be an option if you have a strong credit score. VA and USDA loans offer zero down payment for eligible buyers.

What credit score do you need to get a mortgage?

FHA loans only require a credit score of 500 and Chase is one of the FHA loan providers in the U.S. Standout benefits: Chase’s DreaMaker loan only requires a 3% down payment and income limits have been lifted in many cities. [ Jump to more details ] What do I need to get approved for a mortgage?