Nearly a quarter (22%) of Americans have a FICO Score of 800 or higher, which the credit scoring company describes as exceptional.

“Exceptional.” Depending on ones frame of mind, the word may conjure up anything from a mint condition rookie card to possibly being asked, again, to stay after class. But in the world of credit, exceptional refers to nearly a quarter of consumers with FICO® ScoresÎ of 800 or higher. Hardly an exclusive club, but a nice place to be nonetheless.

As part of our review of consumer credit and debt among U.S. consumers, Experian looked at trends of those who had exceptional credit scores in 2023. To get to the bottom of what, exactly, exceptional credit looks like in practice, well highlight some of the many characteristics of the consumers behind those scores.

Your credit score is one of the most important numbers in your financial life It determines whether you can get approved for credit cards, loans, mortgages, rental applications, and sometimes even jobs But what is considered a good or bad credit score? And what is the most common credit score among Americans? Let’s take a look.

What is a Credit Score?

A credit score is a three-digit number calculated from the information in your credit report, which details your credit history. The most widely used credit scores are FICO scores, created by the Fair Isaac Corporation, and VantageScores, created by the three major credit bureaus (Experian, Equifax, and TransUnion).

Scores range from 300 to 850, with higher scores indicating a lower risk borrower. Lenders use credit scores to evaluate the likelihood that you will repay borrowed money. If you have a high credit score, you are more likely to be approved for credit and get better terms like lower interest rates.

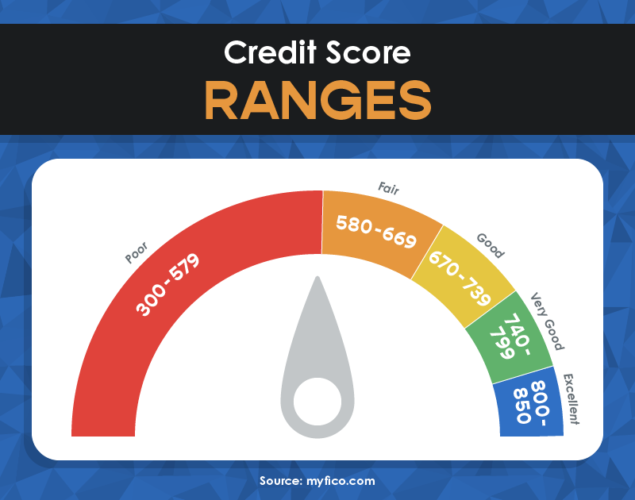

Credit Score Ranges

Although credit scores range from 300-850 most fall between 600 and 750. Here is how the scores are generally grouped

- Poor: 300-579

- Fair: 580-669

- Good: 670-739

- Very Good: 740-799

- Exceptional: 800-850

So what is considered a good or bad credit score? Generally, you need a minimum score of 670 to be approved for most loans and credit cards. However, some lenders have higher cutoffs, so aim for 720+ if you want the best rates and terms.

On the other end, a score below 580 will make it very difficult to get approved for new credit. A poor credit score signals high risk to lenders.

What is the Average Credit Score in America?

According to Experian data from Q3 2022 the average FICO score in America is 716. This has increased from 710 in 2020 and 711 in 2021, showing that Americans’ credit scores continue to improve overall.

The average VantageScore, according to Experian, is slightly lower at 701 as of February 2022. But both scoring models put the average American in the good credit range.

This average, however, varies significantly by location and demographics like age, income, and education level. Let’s break it down further.

Average Credit Score by State

Your location impacts your financial habits and access to credit, so average scores differ quite a bit from state to state.

According to Experian data for 2022, these states have the highest average credit scores:

- Minnesota – 748

- Vermont – 743

- New Hampshire – 742

The states with the lowest average credit scores are:

- Mississippi – 703

- Louisiana – 705

- Nevada – 707

In general, Midwestern and Northeastern states tend to have higher average scores. Southern states lag behind, along with Western states like Nevada and New Mexico.

If you’re curious, you can check the average score for your state in Experian’s report. But remember, these are just averages and your personal score could differ significantly based on your own credit history.

Average Credit Score by Age

Younger Americans tend to have lower credit scores on average, while older generations have higher scores. According to Experian data, the average credit scores by age group are:

- Gen Z (18-25): 680

- Millennials (26-41): 690

- Gen X (42-57): 709

- Baby Boomers (58-76): 745

- Silent Generation (77+): 760

The lowest average belongs to Gen Z. This isn’t surprising since they have had less time to build credit history. Credit scores tend to increase steadily with age as consumers accumulate more credit accounts and history. After retirement, average scores level off and may even decrease slightly.

What is a Good Credit Score?

Now you know that 716 is the average FICO score and 701 is the average VantageScore. But is that a good credit score?

The answer depends on your credit goals. Here are some credit score guidelines to keep in mind:

- Very poor: Below 580 – You will have trouble getting approved for credit.

- Fair: 580-669 – You may get approved but pay higher interest rates.

- Good: 670-739 – Considered a good score by most lenders.

- Very good: 740-799 – Will qualify for the best rates offered.

- Exceptional: 800+ – Top-tier borrowers.

Ideally, you want to reach a minimum of 720 to be approved by most lenders and get the best terms. A higher score opens up your options. Once your score crosses 750, you will qualify for the lowest rates and premium credit card and loan offers.

How to Check Your Credit Score

Checking your own credit score is easy and doesn’t hurt your credit. You can access your credit scores for free through many banks and credit card issuers’ online portals.

For example, Discover lets all customers view their FICO score updated monthly, whether or not you have a Discover card. There are also sites like Credit Karma that offer free access to your VantageScores.

You can also purchase your credit reports including scores from Experian, Equifax, and TransUnion. Federal law gives you free access to your report from each bureau once a year at AnnualCreditReport.com.

Checking your own credit is always a soft inquiry that doesn’t affect your score. Only applications for new credit trigger hard inquiries that may cause a small, temporary drop in your score.

How to Improve Your Credit Score

Now that you know where you stand, here are some tips for raising your credit score if needed:

- Make all loan and credit card payments on time each month. This is the most important factor.

- Keep credit utilization low, under 30%.

- Pay down balances rather than moving debt around with balance transfers.

- Limit new credit applications to only when needed.

- Build credit history by becoming an authorized user on someone else’s account.

- Correct any errors on your credit reports that may be dragging your score down.

With time and diligent credit management, you can steadily build your credit. Monitor your scores every few months to check your progress.

The Takeaway

An average FICO score in America is 716 while the average VantageScore is 701. This puts most people in the good credit range, but many should strive for very good scores of 720+ for the best options. Scores vary greatly by state and age too. Everyone’s personal credit situation is different, so check your own score regularly and focus on continuously building healthy credit habits.

Exceptional Credit by Generation

There were some distinct differences that stood out when comparing overall consumer averages against average stats for consumers with exceptional credit scores. Of particular note among the two measures of consumers was the number of delinquencies (late payments). While a typical consumer has one or two delinquencies on their credit report, those with a FICO® Score of 800 or greater have virtually zero delinquencies among them.

| Average ⦠| Average for All Consumers | Average for Consumers With Exceptional (800-850) FICO® Scores |

|---|---|---|

| Number of credit cards | 3.9 | 4.8 |

| Credit card balance | $6,501 | $3,873 |

| Number of retail credit cards | 2.7 | 3.5 |

| Retail credit card balance | $1,188 | $402 |

| Auto loan balance | $23,792 | $21,799 |

| Mortgage balance | $244,498 | $256,946 |

| Non-mortgage balance | $23,964 | $17,484 |

| Credit utilization ratio | 29% | 7% |

| Total tradelines ever delinquent | 1.5 | 0.01 |

Source: Experian data as of Q3 2023

Otherwise, the characteristics of a consumer with exceptional credit mimics that of more seasoned consumers: They have more lines of revolving credit on average, but much lower average revolving balances. A virtuous consequence of low credit card balances is often a lower credit utilization ratio, which is a key credit score factor. Those with an exceptional credit score have average utilization ratios under 10%, versus 29% for the average consumer. Lower utilization ratiosâthose in the single digitsâcan have a positive effect on FICO® Scores.

Borrowers with exceptional credit scores also carry a slightly larger average mortgage balance than the average consumer, as well as a slightly lower balance on any auto loans in their names.

Exceptional Credit More Common in Northern States

Above-average may be selling Minnesotans shortânearly one-third of state residents have an exceptional credit score. The Gopher State, alongside their Badger State neighbors in Wisconsin, lead the nation with the highest percentage of consumers with an 800 or better FICO® Score. State mascots aside, there is a decidedly Northern tilt to where consumers with exceptional credit scores reside.

Why The American Credit System Is So Terrible

FAQ

Is a 900 credit score possible in the USA?

A credit score of 900 is not possible, but older scoring models that are no longer used once went up to 900 or higher. The highest possible credit score you can acheive now is 850.

Has anyone gotten an 850 credit score?

Despite achieving an 850 score, Michell found that it had little impact on his financial life, as interest rates and insurance costs remained unchanged.Jan 4, 2025

How rare is an 800 credit score?

An 800 credit score is relatively rare, with approximately 23% of Americans achieving this “exceptional” FICO score range (800-850), according to The Motley Fool.

How common is a 700 credit score?

What is the average credit score in the United States?

The average credit score in the U.S. across all states is 718. The state with the highest average credit score is Minnesota at 742, it’s also the only state whose average credit score falls into FICO’s Very Good range. The lowest scoring state is Mississippi with an average credit score of 680, though this is still in FICO’s Good range.

What is the average credit score in all 50 states?

Finances look very different across all 50 states, and the average credit score by state looks pretty different, too. While Mississippi has the lowest average credit score at 680, Minnesota has the highest credit score at 742. Here’s the average credit score in each US state and the District of Columbia according to data from Experian:

Which state has the highest credit score?

Minnesota has the highest average credit score at 742, while Mississippi has the lowest average at 680. People with higher credit scores tend to qualify for better interest rates on borrowed money, have access to the best credit cards, and can even pay less for insurance. You’ll also have an easier time applying for an apartment rental.

Who has the highest credit score?

Asian Americans have the highest average credit score of 745, and Black people have the lowest at 677. In between those are non-Hispanic whites at 734, Hispanic whites at 701, and all others at 732.⁴

What is a good credit score?

Despite slowing and stalling averages, all younger generations sport average scores in the good credit score range of 670 to 739. Older generations have, on average, very good scores in the 740 to 799 range. Either range of scores generally qualifies consumers for offers of credit, although those with very good scores may receive better terms.

What is the average FICO credit score?

The average FICO credit score in the US is 717, according to the latest FICO data. The average VantageScore is 701 as of February 2025. Credit scores, which are like a grade for your borrowing history, fall in the range of 300 to 850. The higher your score, the better. The FICO model of credit scoring puts credit scores into six categories: