You may have sellers remorse in a down market. Or you may be trying to capture some losses without losing a great investment. However it happens, when you sell an investment at a loss, its important to avoid replacing it with a “substantially identical” investment 30 days before or 30 days after the sale date. Its called the wash-sale rule and running afoul of it can lead to an unexpected tax bill.

Have you ever sold a stock at a loss, then bought it back a few weeks later because you thought it was a good deal? If so, you might have accidentally triggered what’s called a “wash sale” – and it could mess with your tax situation more than you realize.

I’ve seen many investors make this mistake especially during market downturns when they’re trying to do some tax-loss harvesting but still want to keep their favorite stocks. Let’s break down everything you need to know about wash sales in simple terms.

The Basics: What Exactly Is a Wash Sale?

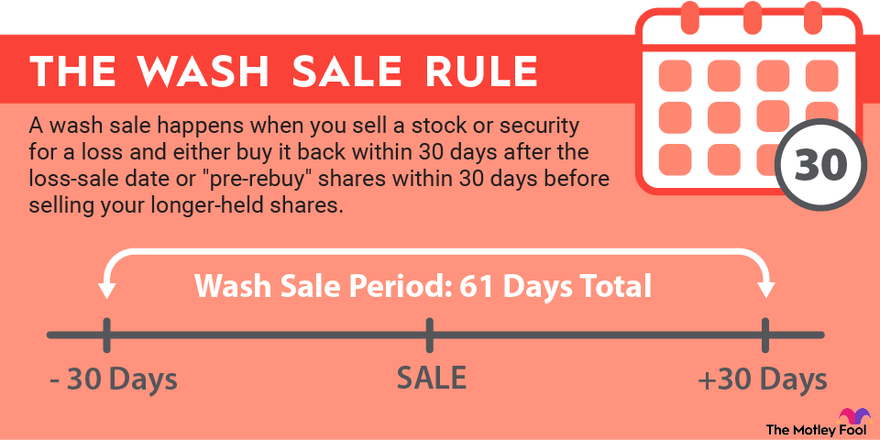

A wash sale happens when you sell a security at a loss and buy a “substantially identical” security within 30 days before or after the sale. The wash-sale rule prevents taxpayers from deducting paper losses without significantly changing their market position.

In simpler terms, the IRS doesn’t want you gaming the system by selling something to claim a tax loss while essentially maintaining your investment position.

How the Wash Sale Rule Works in Real Life

Let me break this down with a practical example

Let’s say you bought 100 shares of XYZ stock for $10 per share, so you spent $1,000 total. A year later, the stock drops to $8 per share, and you decide to sell all your shares, taking a $200 loss.

Three weeks later, you notice XYZ is now trading at $6 per share. “Wow, what a bargain!” you think, and buy 100 shares again for $600 total.

Boom! You’ve just triggered a wash sale because:

- You sold at a loss

- You bought back the same stock

- You did it within the 30-day window

What Happens When You Trigger a Wash Sale?

When you trigger a wash sale, a few things happen:

- You can’t claim that $200 loss on your current year’s tax return

- The amount of the disallowed loss ($200) gets added to the cost basis of your replacement shares

- The holding period of your original shares gets added to the holding period of your replacement shares

So in our example:

- Your new cost basis becomes $800 ($600 purchase price + $200 disallowed loss)

- If you sell those shares later for $1,000, your taxable gain would be $200 instead of $400

- The holding period from your original shares gets tacked on, potentially qualifying you for long-term capital gains treatment sooner

Which Securities Are Covered by the Wash Sale Rule?

The wash sale rule applies to most securities that have a CUSIP number (a unique nine-character identifier), including:

- Individual stocks

- Exchange-traded funds (ETFs)

- Mutual funds

- Options on securities

And here’s something many investors don’t realize: the rule applies across ALL your accounts – even those at different brokerages and your IRAs! Your spouse’s accounts are included too.

Common Wash Sale Misconceptions

Misconception #1: “I can sell in December and buy back in January to avoid the rule”

Nope! The wash sale rule isn’t confined to a calendar year. If you sell on December 15 and buy back on January 4, that’s still within the 30-day window.

Misconception #2: “My broker tracks all my wash sales”

While your broker will track and report wash sales that occur within the same account, they don’t know about your other accounts. It’s up to YOU to keep track of wash sales across different accounts, including IRAs and your spouse’s accounts.

Misconception #3: “I can just buy a similar but different security”

This is actually true! You can sell a security at a loss and immediately buy something similar but not “substantially identical.” The problem is, the IRS hasn’t precisely defined what counts as “substantially identical.”

How to Avoid Triggering the Wash Sale Rule

If you want to harvest tax losses but stay invested in the market, here are some strategies:

- Wait 31 days before buying back the same security

- Buy a similar but not identical security instead

- For example, if you sold an S&P 500 index ETF, you could buy a Russell 1000 Index ETF instead

- Be careful with automated investments like dividend reinvestment plans, which could trigger wash sales without you realizing it

Real-Life Scenarios Where Wash Sales Can Sneak Up on You

Scenario 1: Partial Position Sales

Let’s say you own 1,000 shares of a company and sell 200 shares at a loss for tax-loss harvesting. If you have dividends from the remaining 800 shares automatically reinvested within 30 days, those new shares could trigger a partial wash sale.

Scenario 2: Tax-Loss Harvesting Gone Wrong

Many investors sell losers in December for tax purposes, planning to buy them back in the new year. But if you do this less than 31 days apart, you’ve triggered a wash sale.

Scenario 3: Different Account Types

You sell a stock at a loss in your brokerage account and then buy it back in your IRA within 30 days. This triggers a wash sale, and worse – when the loss is disallowed in an IRA scenario, it basically disappears forever rather than being added to your cost basis.

The Silver Lining of Wash Sales

It’s not all bad news! Remember that a wash sale doesn’t eliminate your tax loss forever – it just defers it. The disallowed loss gets added to the cost basis of your replacement shares, which can:

- Reduce your taxable gains when you eventually sell those shares

- Increase the deductible loss if you sell those replacement shares at a loss

- Potentially give you long-term capital gains treatment sooner due to the tacked-on holding period

Tracking Wash Sales: Who’s Responsible?

While brokers are required to track and report wash sales within the same account, they don’t track wash sales:

- Across different accounts at their firm

- Across accounts at different firms

- Between your accounts and your spouse’s accounts

- Between taxable accounts and IRAs

This means YOU are responsible for tracking potential wash sales across all your accounts.

FAQs About Wash Sales

Q: Does the wash sale rule apply to cryptocurrencies?

Currently, the IRS treats crypto as property rather than securities, so technically the wash sale rule doesn’t apply. However, this could change with new regulations.

Q: What if I sell a stock and my spouse buys it within 30 days?

That still triggers a wash sale. The rule applies to purchases by your spouse or even a company you control.

Q: Can I sell a stock in my individual account and buy it in my IRA?

Yes, but this triggers a wash sale, and the loss is essentially lost forever since you can’t adjust the basis in an IRA.

Q: If I sell an ETF at a loss, can I buy individual stocks that the ETF contains?

Generally yes. Most individual stocks wouldn’t be considered “substantially identical” to an ETF that contains them.

When a Wash Sale Might Actually Make Sense

Sometimes, triggering a wash sale can be a reasonable choice:

- When you strongly believe the security will rise significantly during the 30-day waiting period

- When you’re more concerned about missing market gains than getting the immediate tax deduction

- When the tax loss is small compared to your potential investment gains

Practical Tips for Tax-Efficient Investing

- Keep a calendar: Mark the dates when you sell securities at a loss and avoid repurchasing for at least 31 days

- Consider tax-efficient alternatives: Use similar but not identical securities during the 30-day window

- Communicate with your spouse: Make sure you’re coordinating investment decisions to avoid accidental wash sales

- Use tax-loss harvesting strategically: Plan your tax-loss harvesting around your overall investment strategy

- Keep good records: Document all your transactions in case of an audit

Final Thoughts

Understanding the wash sale rule is crucial for anyone who wants to manage their investment portfolio in a tax-efficient way. While the rule might seem like an annoying limitation, it’s really designed to prevent a specific kind of tax avoidance.

We’ve all been tempted to sell a losing investment to claim the tax loss, then quickly buy it back when it drops even further. The wash sale rule simply ensures that when you claim a capital loss, you’ve actually changed your market position in a meaningful way.

By understanding how wash sales work and planning your investment moves accordingly, you can still practice tax-loss harvesting effectively while staying on the right side of IRS rules.

Remember – wash sales aren’t illegal, they just change when you can claim certain tax benefits. With proper planning, you can navigate these rules while still implementing your investment strategy effectively.

Have you ever accidentally triggered a wash sale? I’d love to hear about your experience in the comments!

What is the wash-sale rule?

When you sell an investment that has lost money in a taxable account, you can get a tax benefit. The wash-sale rule keeps investors from selling at a loss, buying the same (or “substantially identical”) investment back within a 61-day window and claiming the tax benefit. It applies to most of the investments you could hold in a typical brokerage account, including stocks, bonds, mutual funds, exchange-traded funds (ETFs), and options.

More specifically, the wash-sale rule states that the tax loss will be disallowed if you buy the same security, a contract or option to buy the security, or a “substantially identical” security, within 30 days before or after the date you sold the loss-generating investment.

Its important to note that you cannot get around the wash-sale rule by selling an investment at a loss in a taxable account and then buying it back in a tax-advantaged account. Also, the IRS has stated it believes a stock sold by one spouse at a loss and purchased within the restricted time period by the other spouse is a wash sale. Check with your tax advisor regarding your personal situation.

How to avoid a wash sale

One way to avoid a wash sale on an individual stock, while still maintaining your exposure to the industry of the stock you sold at a loss, would be to consider substituting a mutual fund or an exchange-traded fund (ETF) that targets the same industry.

Both ETFs and mutual funds can be particularly helpful in avoiding the wash-sale rule when selling a stock at a loss. Unlike some funds that focus on broad-market indexes, like the S&P 500®, others focus on a particular industry, sector, or other narrow group of stocks. These funds can provide a handy way to regain exposure to the industry or sector of a stock you sold, but they generally hold enough securities that they pass the test of being not substantially identical to any individual stock.

Swapping an ETF for another ETF, or a mutual fund for another mutual fund, or even an ETF for a mutual fund, can be a bit more tricky due to the “substantially identical” security rule. There are no clear guidelines on what constitutes a substantially identical security. The IRS determines if your transactions violate the wash-sale rule. If that does happen, you may end up paying more taxes for the year than you anticipated. So when in doubt, consult with a tax professional.

Good to know: Reinvested dividends via dividend reinvestment plans (DRIPs) may trigger a wash sale. If you sold the same security at a loss within 30 days, automatic repurchases through dividend reinvestments count as acquiring substantially identical securities, disallowing the loss under IRS rules.